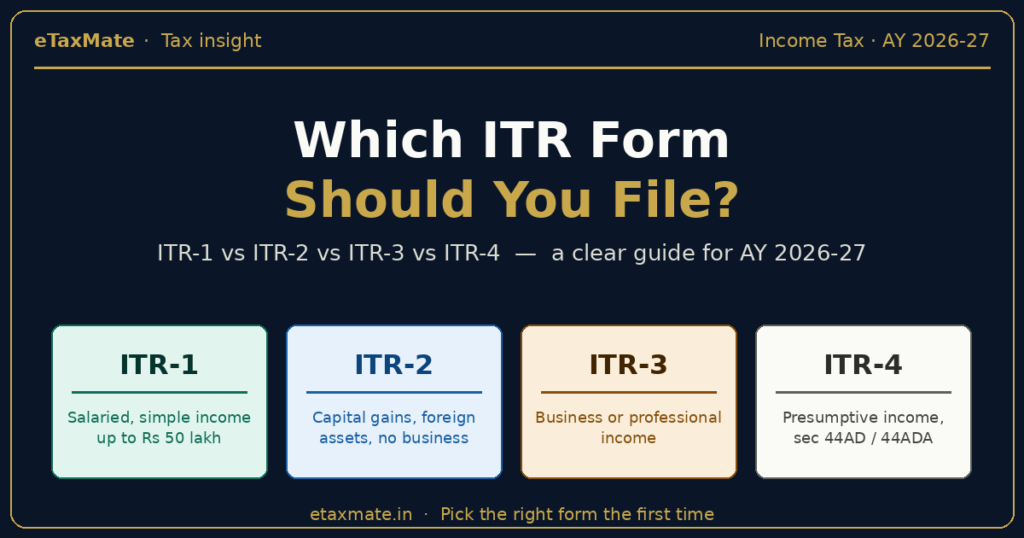

Which ITR Form Should You File?

Which ITR form to file is the single most common question taxpayers ask every June and July. The confusion is understandable. There are seven ITR forms in total, and picking the wrong one is not a harmless mistake — a return filed in the wrong form is treated as a defective return under Section 139(9) of the Income Tax Act 1961, which means the Income Tax Department can ask you to refile or, worse, treat your return as never filed. This post cuts through the noise and tells you exactly which ITR form to file from the four most common options — ITR-1, ITR-2, ITR-3, or ITR-4.

Quick answer

ITR-1 is for salaried residents with simple income up to ₹50 lakh. ITR-2 is for individuals with capital gains, multiple properties, or foreign income but no business. ITR-3 is for anyone with business or professional income. ITR-4 is for presumptive income under Section 44AD, 44ADA, or 44AE.

Before choosing a form, check:

- Do you have any capital gains from shares, mutual funds, or property?

- Do you have business or professional income, even as a side activity?

- Are you a director in a company or holder of unlisted shares?

How the ITR forms are actually split

The four common forms are designed around the source and complexity of your income, not your profession or age. The Income Tax Department updates the applicability rules every assessment year through the ITR notification, so the exact eligibility can shift. For the current filing cycle, the split works like this.

ITR-1 (Sahaj) — for straightforward salaried income

ITR-1 is the simplest form and the one most salaried people should use. You can file ITR-1 if all of the following apply:

- You are a resident individual (not a Hindu Undivided Family or a non-resident).

- Your total income is up to ₹50 lakh.

- Your income is from salary or pension, two house property (not brought forward losses), other sources like interest, and long-term capital gains under Section 112A up to ₹1.25 lakh.

- Your agricultural income is up to ₹5,000.

You cannot file ITR-1 if you are a director in any company, hold unlisted equity shares, have foreign assets or foreign income, have capital gains beyond the ₹1.25 lakh LTCG limit mentioned above, or have brought-forward losses. Many first-time filers tick the ITR-1 box because it is the shortest form, not realising that one mutual fund redemption or a single share sale can push them into ITR-2.

ITR-2 — for individuals with capital gains or other complexity, but no business

ITR-2 is where most salaried professionals with any real investment activity end up. You must file ITR-2 if you are an individual or HUF and any of the following apply:

- You have capital gains from shares, mutual funds, property, or any other asset.

- You own more than two house property.

- You have foreign income or foreign assets, including ESOPs of a foreign parent company.

- You are a non-resident or a resident but not ordinarily resident.

- You are a director in a company or hold unlisted equity shares.

- Your total income exceeds ₹50 lakh.

The critical point: ITR-2 covers everything ITR-1 cannot, as long as you do not have income from business or profession. If you work a salaried job and also invest in the stock market, you are almost certainly an ITR-2 filer.

ITR-3 — for business and professional income

ITR-3 is the form for individuals and HUFs who earn income from a proprietary business or a profession. This includes:

- Freelancers and consultants not using presumptive taxation.

- Doctors, lawyers, architects, and other professionals with actual books of account.

- Traders with income from intraday or futures and options (F&O), which the Income Tax Department treats as business income.

- Partners in a partnership firm (remuneration and interest from the firm).

- Anyone with income from a proprietary business, in addition to salary, capital gains, or house property.

ITR-3 is the most detailed of the four forms because it requires a full profit and loss statement, balance sheet, and disclosures under Section 44AA if you are maintaining books of account. If your business or professional turnover crosses the audit threshold under Section 44AB, a tax audit report must also accompany the return.

A common surprise: salaried professionals who also do some F&O trading on the side often realise too late that F&O losses or profits push them from ITR-2 into ITR-3. This is not optional — it is how the law classifies the income.

ITR-4 (Sugam) — for presumptive income

ITR-4 is a simplified form for small businesses and professionals who opt for presumptive taxation. You can file ITR-4 if you are a resident individual, HUF, or firm (other than LLP) with:

- Business income computed under Section 44AD (6% or 8% of turnover, depending on digital receipts), with turnover up to ₹2 crore (or ₹3 crore if cash receipts are within 5%).

- Professional income computed under Section 44ADA (50% of gross receipts), with gross receipts up to ₹50 lakh (or ₹75 lakh if cash receipts are within 5%).

- Transport income under Section 44AE.

- Total income up to ₹50 lakh.

Presumptive taxation means you declare a fixed percentage of turnover as income and do not maintain detailed books. The trade-off is that once you opt in, you must continue for at least five years if using Section 44AD, or face restrictions re-entering.

Important: The Income Tax Act 2025, which is set to replace the 1961 Act for assessment year 2026-27 onwards, largely carries forward the existing ITR structure and presumptive framework. The section numbers may change in the new Act, but the substance of who files which form is expected to remain the same for this filing cycle. The applicable regime — old or new — is declared inside the form itself and does not change which form you file.

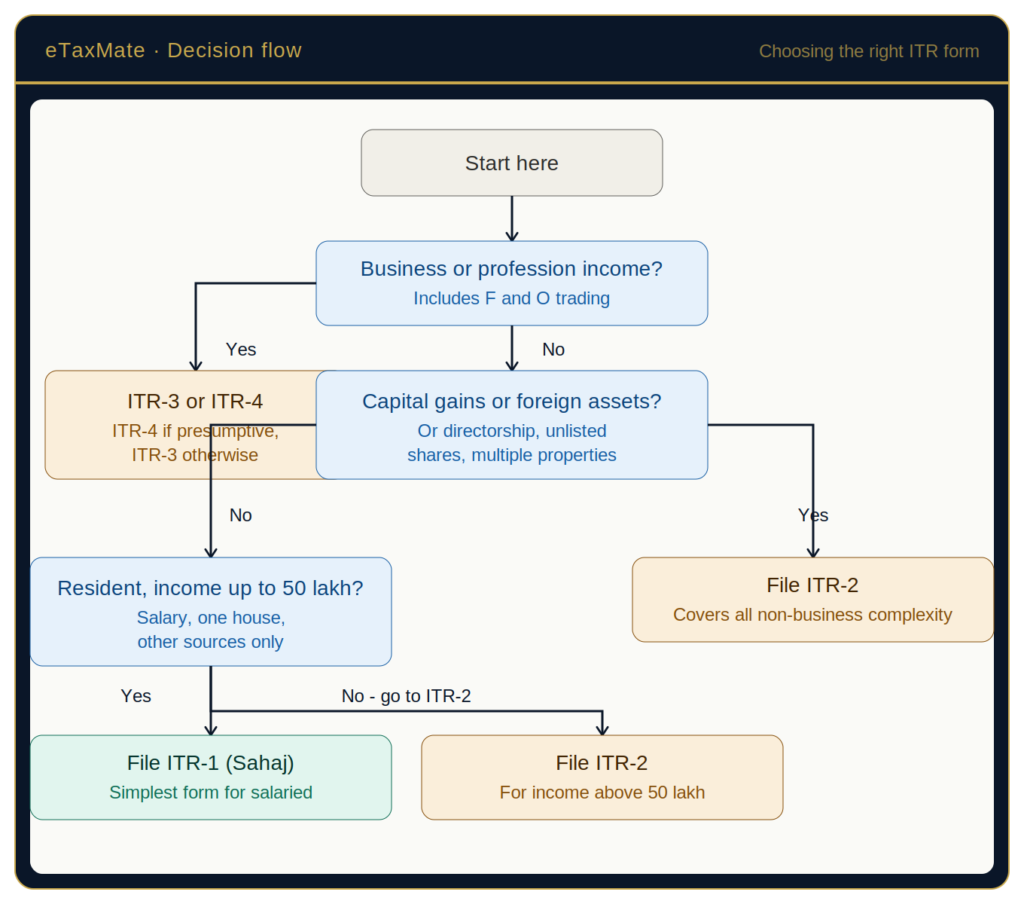

How to decide which ITR form to file

Start with the most restrictive condition and work outwards. The practical sequence is to ask yourself about business income first, then capital gains, then disqualifiers like directorships and foreign assets, and only default to ITR-1 if none of those apply. The flow below captures the decision for a typical individual filer.

Edge cases the flowchart does not cover

- Partners in a firm: File ITR-3, even if your only income from the firm is remuneration and interest.

- NRIs: Cannot file ITR-1 or ITR-4. Default to ITR-2 unless you have business income, in which case ITR-3.

- HUFs: Cannot file ITR-1. Choose between ITR-2, ITR-3, or ITR-4 based on the same income-type logic.

- Companies, LLPs, and trusts: Use ITR-5, ITR-6, or ITR-7 — outside the scope of this post.

When you should not rush to file ITR-1

ITR-1 is tempting because it is short and pre-filled on the Income Tax portal. But filing ITR-1 when you should have filed ITR-2 or ITR-3 causes real problems.

Do not use ITR-1 if:

- You sold any shares, mutual funds, or property during the year, even at a small profit or loss. Capital gains beyond the Section 112A threshold require ITR-2.

- You did any intraday trading or F&O trading. That is business income and forces ITR-3.

- You are a director in a private limited company, even if it is dormant or you draw no salary from it.

- You hold unlisted shares, including ESOPs granted before your company listed, or shares in a startup.

- You have any foreign bank account, foreign investment, or ESOPs in a foreign parent company — these require ITR-2 disclosure under the foreign asset schedule.

- You have brought-forward losses you want to set off this year.

Filing the wrong form is the single most common reason returns are marked defective. The fix involves filing a revised return in the correct form, which eats into your window and adds avoidable stress.

Documents to keep ready before filing

Regardless of which form applies, keep these ready:

- PAN and Aadhaar (linked).

- Form 16 from your employer, if salaried.

- Form 26AS and the Annual Information Statement (AIS) from the Income Tax portal.

- Bank account statements for the full financial year.

- Capital gains statements from your broker and mutual fund platforms.

- Interest certificates from banks and post offices.

- Rent receipts and home loan interest certificate, if claiming HRA or Section 24 deduction.

- Proof of deductions claimed under Chapter VI-A (80C, 80D, and similar).

- Business books, P&L, and balance sheet if filing ITR-3.

Final takeaway

The ITR form is decided by the nature of your income, not your job title or income level alone. Work through the questions in order: business income first, then capital gains and other complexity, then the ITR-1 eligibility test as the final filter. If you tick even one disqualifier for ITR-1, move up the chain. A return filed in the right form the first time saves you from defective return notices, revised filings, and the avoidable stress of correcting a mistake mid-season.

ITR-form confusion or need expert help choosing the right form for your capital gains, business income, or foreign asset situation? eTaxMate can help you review your income profile, pick the correct ITR form, and file accurately before the due date.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.