You filed your ITR, got the acknowledgement, and a few weeks later an email landed in your inbox titled Intimation under Section 143(1) of the Income Tax Act for PAN XXXXX. Maybe the refund you expected shrunk. Maybe a demand appeared out of nowhere. Maybe both. The first instinct is panic — has the department flagged something? Is this a notice? Is scrutiny next? The short answer is no. An intimation under 143(1) is a routine, automated message from the Central Processing Centre at Bengaluru. It is the most common communication a taxpayer receives, and in most cases it is solvable in a matter of minutes if you know what to look for.

Quick answer

An intimation under 143(1) is an automated summary of how the Income Tax Department processed your ITR. It is not a scrutiny notice. It tells you one of three things — no change, refund, or demand — and where it differs from your return, the difference is almost always a fixable mismatch.

Before reacting, check:

- Is the PAN, assessment year, and acknowledgement number on the intimation the same as your filed return?

- Which column differs — the “as filed” or the “as computed” side?

- If a demand has been raised, what is the date of issue (the 30-day response clock starts from there)?

What an intimation under 143(1) actually is

When you file your ITR, the return travels to the Central Processing Centre, known as CPC, at Bengaluru. The CPC runs an automated check that recomputes your total income, deductions, and tax payable using its own records — chiefly Form 26AS, the Annual Information Statement (AIS), and the data uploaded by your employer and your banks. If the two computations match, the return is accepted as filed. If they do not match, the system makes adjustments and sends you an intimation under 143(1) explaining what changed.

A few facts worth knowing upfront:

- The intimation must be issued within nine months from the end of the financial year in which the return was filed. For a return filed in July 2025 for FY 2024-25, the department has until 31 December 2026 to send the intimation. Intimation Under Section 143(1) of Income Tax Act – ITR Intimation Password +3

- If you do not receive any intimation within that window, the law treats your filed ITR as having been accepted in full. The ITR acknowledgement itself becomes the deemed intimation under 143(1). CleartaxKotak Life

- The intimation arrives by email and SMS to the addresses registered on the Income Tax e-filing portal. The PDF is password-protected; the password is your PAN in lowercase followed by your date of birth in DDMMYYYY format. For PAN AAGRK5803P and DOB 2 November 1982, the password is

aagrk5803p02111982. Tax2Win - Under the new Income Tax Act 2025, Section 143(1) of the 1961 Act has been renumbered as Section 270 of the 2025 Act. The substance is the same — what was 143(1) is now 270 — but most taxpayers, the e-filing portal, and tax software still refer to it as 143(1) for the foreseeable future. This post uses 143(1) throughout. Tax2Win

The most important thing to grasp is this: an intimation under 143(1) is a preliminary processing outcome, not an assessment. It is not a scrutiny notice (that would be Section 143(2)), not a reassessment, and not an allegation of concealment. It is a computer-generated comparison sheet.

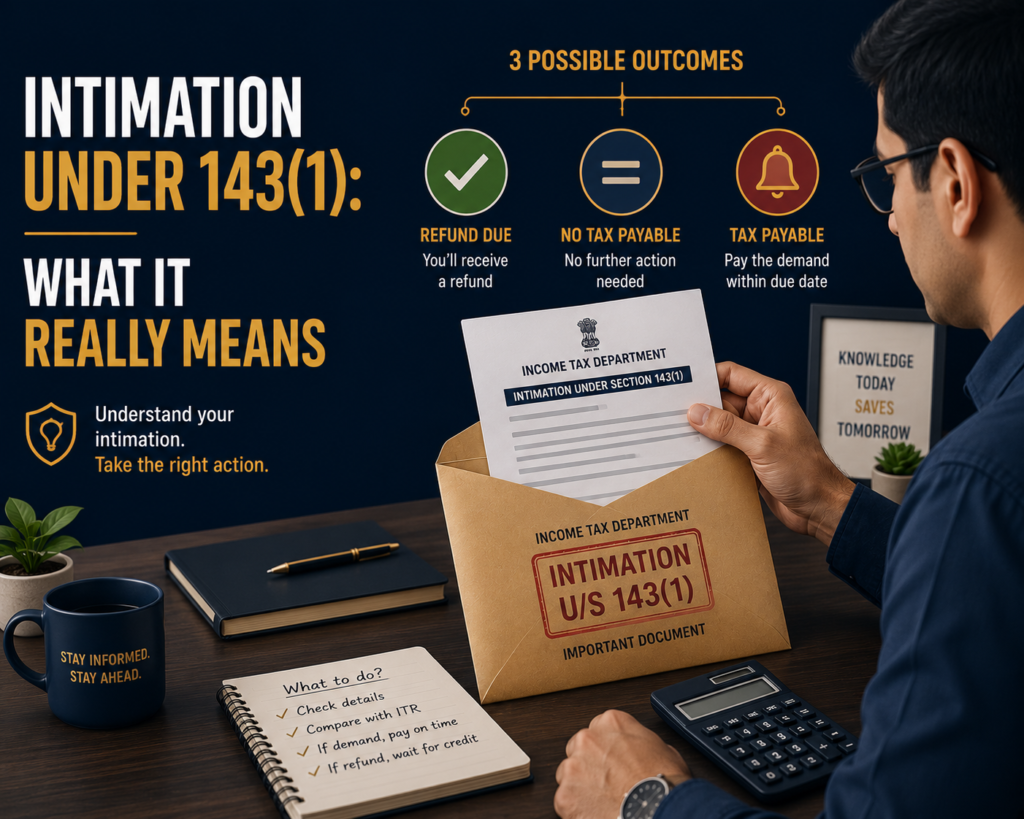

The three things a 143(1) intimation can say

Every intimation falls into one of three buckets. The intimation itself is laid out as two columns — As provided by taxpayer in return of income and As computed under section 143(1) — and the difference between the two determines which bucket you are in.

The three possible outcomes:

- No change. The numbers in the as filed column match the as computed column. Your return is accepted. No further action is required, and the acknowledgement is treated as the final intimation. Bajaj FinservCanara HSBC Life

- Refund determined. Your tax paid (TDS, advance tax, self-assessment tax) is more than the tax liability computed by the department. A refund is issued only if the amount exceeds ₹100, credited to the pre-validated bank account, typically within 20-45 days of e-verification. Intimation Under Section 143(1) of Income Tax Act – ITR Intimation Password +2

- Demand raised. The department’s computation shows you owe more tax than you paid. The intimation includes a challan and a deadline. This is where most readers panic — and where most demands turn out to be fixable mismatches rather than genuine tax shortfalls.

Why refunds get reduced or demands get raised

A 143(1) demand or a reduced refund almost always boils down to one of a small set of recurring mismatches. The CPC can only make limited, objective adjustments under Section 143(1)(a) — it cannot reopen your assessment or question your business judgement. The adjustments it is allowed to make are essentially arithmetical or apparent-from-record:

- TDS not appearing in Form 26AS. This is the single most common cause. Rahul, a software engineer in Pune drawing ₹14 lakh a year, received a demand of ₹22,000. His employer had deducted TDS correctly, but the quarterly TDS return was filed three weeks late. By the time CPC processed Rahul’s ITR, the TDS was not visible against his PAN. Fix: get the employer to file a corrected TDS return, then file a rectification.

- Self-assessment challan not entered. You paid the balance tax through Challan 280 but forgot to enter the BSR code and challan number in Schedule IT of the ITR. CPC sees zero self-assessment tax paid and raises a demand for the same amount.

- AIS or Form 26AS mismatch on income. Bank interest, dividend, or capital gains shown in the AIS but not declared in the return. Priya, a freelance designer, declared ₹6 lakh of professional income but forgot the ₹38,000 of FD interest reflected in her AIS. CPC added it back and raised a demand of around ₹11,800.

- Deductions inconsistent with Form 16. You claimed ₹1.5 lakh under Section 80C in the ITR but your Form 16 shows only ₹70,000 because you did not declare the other investments to your employer in time. Under the new tax regime, you cannot claim most Chapter VI-A deductions at all — claiming Section 80C while filing under the new regime will trigger a 143(1)(a) disallowance.

- Loss carry-forward where the return was filed late. Carry-forward of business or capital losses is allowed only if the return was filed within the original due date under Section 139(1). File late, and the CPC will disallow the loss carry-forward through a 143(1)(a) adjustment.

- Old vs new regime mismatch. Claiming HRA, LTA, or 80C while having opted for the new regime — or vice versa — produces an automated disallowance.

This is why matching your Form 26AS and AIS before filing is the single highest-impact pre-filing step you can take. It is also why correct ITR form selection matters — the wrong form can block legitimate deductions from being processed.

What to do when you get an intimation under 143(1)

Step by step, regardless of which bucket you fall into:

- Open and read the PDF. Use the password format described above (PAN in lowercase + DOB in DDMMYYYY).

- Check the identifiers. PAN, name, assessment year, and e-filing acknowledgement number must all match your filed return. If even one is wrong, the intimation may not belong to you.

- Compare the two columns line by line. Identify exactly which row differs — gross total income, a specific deduction, TDS credit, advance tax, self-assessment tax. The difference is almost always concentrated in one or two rows.

- If the intimation is “no change”: do nothing. Save the PDF for your records.

- If a refund is shown: confirm your bank account is pre-validated on the Income Tax e-filing portal. The refund typically credits within 20-45 days of e-verification.

- If a demand is shown and you agree: pay through Challan 280 on the portal, selecting the correct assessment year and choosing “Self-Assessment Tax.” The demand is settled automatically within 3-5 working days of payment reflecting.

- If a demand is shown and you disagree: file a rectification request under Section 154 through the e-filing portal, attaching the supporting evidence (corrected Form 26AS, challan, original investment proof). You can also file a response under “Pending Actions > e-Proceedings” to disagree with the proposed adjustment. If a notice has been issued under Section 143(1)(a) proposing an adjustment, the response window is 30 days from the date of issue — miss it and the adjustment is made automatically. IT Notice for Proposed Adjustment u/s 143(1)(a) – Learn by Quicko +3

The action against each outcome can be visualised on the e-filing portal under Pending Actions and View Filed Returns. You can also see all past intimations under Services > Income Tax Forms > View Filed Forms on the Income Tax e-filing portal.

When you should not rush to pay the demand

A demand is not always correct, and paying it immediately can be the wrong move. Do not pay before checking:

- The TDS column. If the demand equals the TDS that you can see in your salary slips but is missing from Form 26AS, do not pay. Get the deductor (your employer or bank) to file a corrected TDS return. Once it reflects in 26AS, file a rectification — the demand will be withdrawn.

- The challan column. If you paid self-assessment tax but did not enter the challan details in the ITR, do not pay again. File a rectification with the BSR code and challan number — the demand should drop to zero.

- The interest column. Check whether interest under Section 234A, 234B, or 234C has been computed correctly. CPC sometimes computes interest on a base that ignores TDS credits, inflating the demand.

- Already-issued refund being adjusted. If a refund is being withheld because of a demand from an earlier year, verify that the earlier-year demand is itself correct. An incorrect old demand can drag down a current-year refund.

Paying first and arguing later is harder than getting it right the first time. The rectification route exists precisely so you do not have to pay a wrong demand.

Documents to keep ready before you respond

- The intimation PDF (and its password to reopen later)

- Your filed ITR (PDF and Excel utility, if available)

- Form 16 from each employer

- Form 26AS for the relevant assessment year

- AIS and Taxpayer Information Summary (TIS)

- Self-assessment tax challans (Challan 280 receipts)

- Investment proofs for the deductions claimed

- Bank statement showing TDS-suffered interest credits

- Your registered email and mobile login for the Income Tax e-filing portal

Final takeaway

An intimation under 143(1) sounds intimidating but is almost always a routine processing message. The three possible outcomes — no change, refund, demand — each have a clear path forward. Most demands are fixable through a rectification under Section 154 once the underlying mismatch (a missing TDS entry, an unentered challan, an undeclared interest income) is corrected. The single thing that turns a 143(1) intimation into a real problem is ignoring it. Read it, compare the columns, and respond within the 30-day window where an adjustment notice is involved.

Received an intimation under 143(1) with a reduced refund, an unexpected demand, or a confusing adjustment? eTaxMate can help you read the intimation, identify the mismatch, and file the right response — rectification, revised return, or payment — through the e-filing portal.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. Is an intimation under 143(1) a tax notice?

No. An intimation under 143(1) is an automated processing outcome from the Central Processing Centre, not a scrutiny notice. It compares the income and tax in your ITR with the department’s own records and tells you whether there is a refund, a demand, or no change. A scrutiny notice is issued under Section 143(2) and follows a very different procedure. The two should not be confused.

2. What is the password for the 143(1) intimation PDF?

The PDF is password-protected. The password is your PAN in lowercase followed by your date of birth in DDMMYYYY format, with no spaces or special characters. For example, if your PAN is ABCDE1234E and you were born on 1 January 1990, the password is abcde1234e01011990. The same format works for the intimation copy downloaded later from the e-filing portal.

3. How long does the Income Tax Department have to send a 143(1) intimation?

The department must issue the intimation within nine months from the end of the financial year in which the return was filed. For an ITR filed in July 2025 for FY 2024-25, the deadline is 31 December 2026. If no intimation arrives by that date, the law treats the ITR as accepted in full, and the acknowledgement itself becomes the deemed intimation under 143(1).

4. I got a demand but the TDS is missing from Form 26AS. Should I pay it?

Not yet. If the TDS shown in your salary slip or Form 16 is missing from Form 26AS, the cause is usually that the deductor (employer or bank) filed a late or incorrect TDS return. Get them to file a correction first. Once the TDS reflects in 26AS, file a rectification under Section 154 — the demand will be withdrawn. Paying without checking creates an unnecessary refund-claim cycle later.

5. What is the difference between an intimation under 143(1) and a notice under 143(1)(a)?

An intimation under 143(1) is the final processing outcome — refund, demand, or no change. A notice under 143(1)(a) comes earlier and is a proposal: it informs you of a discrepancy and gives you 30 days to respond before the adjustment is finalised. If you do not respond within 30 days, the proposed adjustment is applied automatically and a final intimation under 143(1) is issued with the resulting demand or reduced refund.

6. Can I revise my return after receiving an intimation under 143(1)?

Yes, provided the time limit for filing a revised return under Section 139(5) has not expired — that is, three months before the end of the relevant assessment year or before the return is processed, whichever is earlier. If the return has already been processed and the assessment year has ended, the route is no longer revised return but rectification under Section 154, which can address apparent errors in the processing.