If you are a freelancer, consultant, or independent professional, the advance tax question hits every quarter. Unlike a salaried employee whose TDS gets deducted automatically, your clients may or may not deduct TDS, and even when they do, it rarely covers your full liability. The Income Tax Department does not wait until July of the following year for the rest. It expects you to pay tax on what you earn, in the year you earn it, in four instalments. Miss the dates and you start clocking interest under Sections 234B and 234C. This post explains who actually needs to pay advance tax, how to estimate it without overcomplicating things, and the one shortcut that lets most professionals collapse the whole calendar into a single 15 March payment.

Quick answer

You must pay advance tax if your total tax liability for the year, after TDS already deducted, exceeds ₹10,000. Freelancers and professionals are the most affected group because their TDS coverage is usually partial. Salaried-only individuals with no other income are usually covered by their employer’s TDS.

Before deciding what to pay, check:

- Is your estimated tax for the year, minus TDS already deducted by clients, above ₹10,000?

- Are you eligible for presumptive taxation under Section 44ADA (gross professional receipts up to ₹75 lakh, or ₹50 lakh if cash receipts exceed 5%)?

- Have you accounted for all income — professional fees, bank interest, FD interest, capital gains, rental income?

When advance tax applies to you

Advance tax is the “pay-as-you-earn” mechanism in Indian income tax. The principle is simple: instead of paying your full tax liability in July of the following year while filing your ITR, you pay it during the year, in instalments, as the income is earned. The legal threshold is the same across taxpayer categories — if your tax liability after adjusting for TDS, TCS, and other prepaid credits is ₹10,000 or more for the financial year, advance tax becomes mandatory.

Three categories of taxpayers see this most often:

- Freelancers and consultants. Clients may deduct TDS at 10% under Section 194J (professional fees), but your applicable slab rate is almost always higher. The shortfall is yours to cover through advance tax.

- Business owners. Income from a proprietorship or partnership flows to you net of any TDS on contract receipts (typically 1-2% under Section 194C), which rarely covers the full liability.

- Salaried individuals with side income. A salaried professional who also earns rental income, capital gains from share sales, or interest on a large FD often crosses the threshold even though salary TDS is fully deducted by the employer.

A common misconception is that advance tax is only for big businesses. Priya, a Bengaluru-based freelance UI designer billing ₹85,000 a month, sees ₹8,500 deducted by her main client each month as TDS under Section 194J. Her total receipts for the year are around ₹10 lakh. Her total tax under the new regime works out to roughly ₹50,000, while TDS deducted by clients is only ₹1 lakh — wait, that exceeds her liability, so she has a refund coming, not advance tax due. Now consider Rahul, a Pune-based freelance software developer with two foreign clients (no TDS) and one domestic client (TDS deducted), earning ₹18 lakh a year. TDS on the domestic portion may be ₹40,000, but his total liability is closer to ₹2.5 lakh. Rahul has to pay the gap — over ₹2 lakh — as advance tax in four instalments. The difference between the two cases is not income size; it is TDS coverage.

Two important exemptions to remember:

- Resident senior citizens (60 years or above) who do not have income from business or profession are exempt from advance tax even if their tax liability exceeds ₹10,000.

- Capital gains shortfall relief. If your shortfall in an instalment is because you could not have estimated a capital gain in advance (you sold shares or property mid-year), no interest applies under Section 234C as long as you pay the tax on that gain in the next instalment or by 31 March.

Note on the new Act: under the Income Tax Act 2025, Section 234B has been renumbered as Section 424 and Section 234C as Section 425, but the rates (1% per month, 1% or 3% for the specified periods) and triggers are identical. Most taxpayers and the e-filing portal continue to refer to them by their old numbers, and this post does the same. Income Tax Department

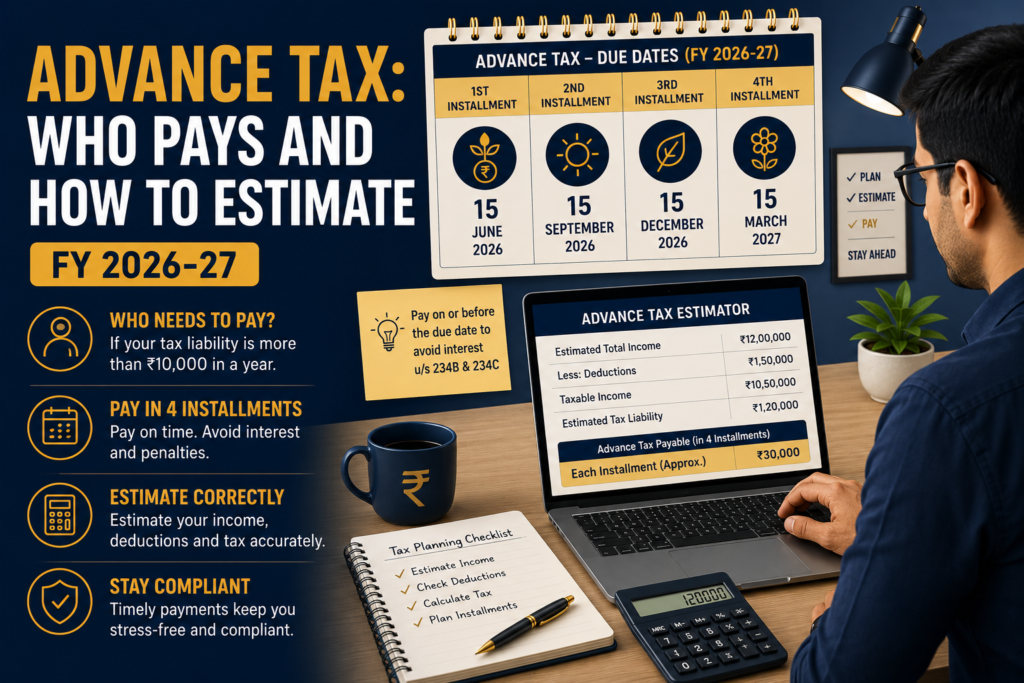

The advance tax due dates and instalment percentages

The four advance tax instalments for FY 2026-27 (AY 2027-28) are:

| Due date | Cumulative advance tax payable |

|---|---|

| 15 June 2026 | 15% of estimated annual tax |

| 15 September 2026 | 45% of estimated annual tax |

| 15 December 2026 | 75% of estimated annual tax |

| 15 March 2027 | 100% of estimated annual tax |

“Cumulative” is the key word. By 15 September, you must have paid 45% in total — not an extra 45% on top of the June instalment. So if your estimated annual tax is ₹1,00,000, the June payment is ₹15,000, and the September payment is ₹30,000 more (taking the total to ₹45,000).

Miss an instalment, or pay less than the required cumulative percentage, and Section 234C kicks in: 1% per month interest on the shortfall for three months for the first three instalments and one month for the March instalment. For the March 15 instalment, even a one-day delay results in a 1% interest charge for that month. Section 234B is the bigger penalty — if your total advance tax paid by 31 March falls short of 90% of your final assessed tax, interest at 1% per month runs from 1 April until you pay the balance, calculated on the entire shortfall. Legal Raasta

A simple way to picture the calendar and the three things that determine whether you owe advance tax:

How to estimate your advance tax: a freelancer walkthrough

Estimation is where most freelancers either freeze or over-engineer. The realistic approach is closer to a back-of-envelope calculation than a forensic forecast. Walk through it like this, using the example of Rahul, a freelance developer, sitting down on 10 June 2026 to estimate his June instalment:

- Estimate gross annual receipts. Rahul looks at his invoicing record from April-May and his pipeline for the rest of the year. He projects ₹18 lakh in gross professional receipts for FY 2026-27.

- Subtract business expenses (if not using presumptive). Office rent, internet, software subscriptions, professional development, asset depreciation. Rahul estimates ₹3 lakh of legitimate expenses. Net professional income: ₹15 lakh.

- Add other income. Bank and FD interest, dividends, capital gains, rental income. Rahul has ₹40,000 of FD interest expected.

- Apply the regime. Under the new regime (FY 2026-27 slabs), tax on ₹15.4 lakh works out to roughly ₹1,30,000 plus 4% cess. Under the old regime with deductions (₹1.5 lakh under 80C, etc.), it could be lower or higher depending on his investments. Pick the regime he expects to use for filing.

- Subtract TDS already deducted. Rahul’s domestic client will deduct roughly ₹40,000 in TDS for the year. The foreign clients deduct nothing.

- The remaining tax is the advance tax base. ₹1,35,000 (with cess) minus ₹40,000 TDS = ₹95,000 of advance tax for the year.

- Multiply by the cumulative percentage for the instalment. For 15 June: 15% of ₹95,000 = ₹14,250.

This is the discipline. You re-do it at every quarter using updated numbers — actual receipts so far, updated expense estimates, and any income that has changed. By 15 March, the cumulative number should be 100% of the corrected annual estimate. Choosing the right regime matters here; if you have not yet decided between old vs new tax regime, run the calculation under both and pay based on the regime you will actually use when filing.

The Section 44ADA shortcut for professionals

If you are a “specified profession” — legal, medical, engineering, architectural, accountancy, technical consultancy, interior decoration, film artist, company secretary, authorised representative, or any other notified profession — and your gross annual receipts are up to ₹75 lakh (or ₹50 lakh if cash receipts exceed 5%), Section 44ADA changes the rules in your favour:

- You declare 50% of gross receipts as deemed income, regardless of actual expenses.

- The remaining 50% is presumed to be business expenses, no documentation required.

- The whole quarterly schedule collapses: you can pay 100% of your advance tax in a single instalment by March 15. No 15 June, 15 September, or 15 December instalments. No Section 234C interest if the full liability is paid by 15 March. AI Accountant

For a freelancer doing technical consultancy at ₹15 lakh a year, this is genuinely useful. Income is deemed at ₹7.5 lakh, tax under the new regime is around ₹26,000, and the whole thing can be paid in one shot before 15 March. The price you pay is that you cannot claim actual expenses above 50% of receipts, even if your real costs are higher. Most pure-services freelancers (developers, designers, writers, consultants) have expenses far below 50%, so 44ADA is usually advantageous.

For the wider rules and trade-offs of opting into the scheme, see our detailed coverage of freelance tax in India and presumptive taxation under Section 44ADA.

How to pay advance tax and avoid 234B and 234C interest

The mechanics are quick:

- Log in to the Income Tax e-filing portal at eportal.incometax.gov.in.

- Navigate to e-Pay Tax > New Payment > Income Tax.

- Select the correct assessment year — for FY 2026-27 income, choose AY 2027-28.

- Choose Advance Tax (100) as the type of payment. This is critical — do not select Self-Assessment Tax, because the credit will appear in the wrong head and you will struggle to claim it later.

- Enter the amount split as appropriate (tax, surcharge if applicable, cess at 4%).

- Pay via net banking, debit card, or UPI. Save the challan PDF — it carries the BSR code and challan serial number you will need at the time of filing your ITR.

The challan reflects in your Form 26AS within 3-5 working days. Once it does, the credit is automatically available against your ITR.

When you should not pay advance tax (or can skip an instalment)

Not every freelancer needs to pay advance tax, and not every quarter requires a payment. Skip or scale back in these cases:

- Your TDS coverage is enough. If clients deduct enough TDS to cover or exceed your total annual liability, advance tax is not required. Refunds get processed at year-end through ITR filing.

- You are a resident senior citizen with no business or professional income. Even if your liability exceeds ₹10,000, the law specifically exempts you.

- Estimated annual tax (after TDS) is below ₹10,000. No advance tax is due. Pay the balance as self-assessment tax before filing your ITR.

- A one-off capital gain arose mid-year. If you could not have anticipated the gain in earlier instalments, the law gives relief — pay the tax on that gain in the next instalment or by 31 March, and no Section 234C interest applies on that portion.

- You are opting for Section 44ADA presumptive. Wait until 15 March and pay 100% in one instalment.

What you should not do is skip an instalment because “the next quarter will cover it.” Section 234C interest is calculated instalment by instalment, not on the year as a whole. Each missed deadline adds a separate interest charge for that period.

Documents and inputs to keep ready

- Bank statements covering the financial year so far

- Invoice register or accounting software export showing professional receipts

- Form 26AS for the current year (shows TDS deducted by clients)

- AIS and TIS for the current year

- FD and savings interest certificates from banks

- Capital gains statements from broker / mutual fund / property sale

- Rental income records, if any

- Last year’s ITR (useful baseline for estimation)

- Login credentials for the Income Tax e-filing portal

- A regime-comparison sheet for old vs new regime tax computation

Final takeaway

Advance tax is a discipline more than a difficulty. The threshold is ₹10,000 of tax liability after TDS, the four dates are 15 June, 15 September, 15 December, and 15 March, and the calculation can be done in under fifteen minutes once your books are in order. Freelancers who treat advance tax as a quarterly habit avoid the double penalty of Section 234B and 234C interest, and those who qualify for Section 44ADA can collapse the whole calendar into a single 15 March payment. The hardest part is the first quarter — once you have done June, the rest is repetition with updated numbers.

Confused about whether advance tax applies to you, struggling with quarterly estimates, or unsure whether Section 44ADA presumptive taxation makes sense for your practice? eTaxMate can help you review your income, compute your liability under the right regime, and pay each instalment correctly.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. When is advance tax compulsory for a freelancer?

Advance tax is compulsory if your total tax liability for the year, after adjusting for TDS deducted by clients, exceeds ₹10,000. Freelancers fall into this category very easily because client TDS under Section 194J is only 10% while your applicable slab rate is usually higher. The threshold is calculated on the net liability, not on gross income.

2. What are the advance tax due dates for FY 2026-27?

The four instalments are due on 15 June 2026, 15 September 2026, 15 December 2026, and 15 March 2027. The cumulative percentages are 15%, 45%, 75%, and 100% of estimated annual tax. Missing a date triggers Section 234C interest at 1% per month on the shortfall, calculated separately for each missed instalment.

3. Can a freelancer under Section 44ADA pay advance tax in one instalment?

Yes. If you opt for presumptive taxation under Section 44ADA (available for specified professionals with gross receipts up to ₹75 lakh, or ₹50 lakh if cash receipts exceed 5%), you can pay the entire advance tax in a single instalment by 15 March. The quarterly schedule of 15 June, 15 September, and 15 December does not apply.

4. What is the difference between Section 234B and Section 234C interest?

Section 234C applies if you miss a quarterly instalment or pay less than the required cumulative percentage — interest at 1% per month on the shortfall for the period of delay. Section 234B applies if your total advance tax paid by 31 March is less than 90% of the final assessed tax — interest at 1% per month from 1 April until you pay the balance, calculated on the whole shortfall.

5. Are salaried individuals also liable to pay advance tax?

Only if they have income beyond salary that is not covered by employer TDS — rental income, bank interest, capital gains from share sales, or freelance side income. The employer deducts TDS on salary itself, so if salary is your only income, advance tax usually does not apply. The ₹10,000 threshold is calculated on the additional liability that TDS does not cover.

6. Do I have to pay advance tax on unexpected capital gains?

You must pay tax on capital gains, but the law gives relief on timing. If a capital gain arises mid-year that you could not reasonably have anticipated in an earlier instalment, no Section 234C interest applies on that shortfall — provided you pay the tax on the gain in the next instalment after the sale or by 31 March, whichever is earlier. This relief is specifically for unforeseen capital gains.