If someone told you that income up to ₹12 lakh is now tax-free, they gave you half the story. The full story is that Section 87A of the Income Tax Act 1961 provides a rebate — and that rebate comes with conditions many taxpayers miss. Some people who expect zero tax end up with a bill. Others who think they are not eligible actually are. This post breaks down exactly who qualifies for the Section 87A rebate for AY 2026-27, who does not, and where the common traps are.

Quick answer

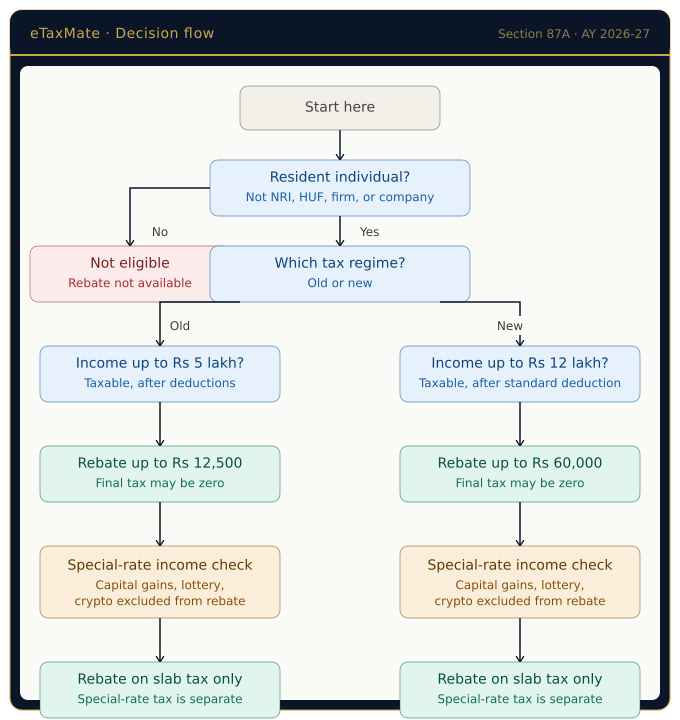

The Section 87A rebate for AY 2026-27 is available only to resident individuals. Under the new tax regime, taxable income up to ₹12 lakh gets a rebate of up to ₹60,000. Under the old tax regime, taxable income up to ₹5 lakh gets a rebate of up to ₹12,500.

Before assuming you qualify, check:

- Are you a resident individual (not NRI, not HUF, not a company)?

- Is your taxable income within the limit for your chosen regime?

- Does your income include capital gains or other specially-taxed items that the rebate does not cover?

What the Section 87A rebate actually is

A rebate is different from a deduction. A deduction reduces your taxable income before tax is calculated. A rebate reduces the tax itself, after it has been calculated. Section 87A gives eligible resident individuals a rebate on their computed tax, which can bring their final tax to zero if the rebate equals or exceeds the tax.

The rebate has existed since 2013. The Union Budget 2025 raised the rebate significantly for taxpayers choosing the new regime, which is why AY 2026-27 is getting so much attention.

Who qualifies for the rebate in AY 2026-27

The conditions are strict. All of them must be met.

Condition 1: You must be a resident individual

The rebate is available only to individuals who are residents of India under Section 6 of the Income Tax Act. This excludes:

- Non-Resident Indians (NRIs)

- Hindu Undivided Families (HUFs)

- Associations of Persons (AOPs) and Bodies of Individuals (BOIs)

- Partnership firms

- Companies

- LLPs

If you are not sure whether you qualify as a resident for the year, residential status depends on the number of days you stayed in India during the financial year and in earlier years. It is a separate test that must be cleared first.

Condition 2: Your taxable income must be within the limit

The income limit depends on which tax regime you choose.

Under the new tax regime (default regime), the limit is ₹12 lakh of taxable income. The maximum rebate is ₹60,000. This is the big change announced in Union Budget 2025. Before AY 2026-27, the new-regime limit was ₹7 lakh with a maximum rebate of ₹25,000.

Under the old tax regime, the limit remains ₹5 lakh of taxable income, with a maximum rebate of ₹12,500. This has not changed in many years.

Taxable income means total income after all allowable deductions and exemptions have been applied. It is not gross salary or gross receipts.

Condition 3: Senior citizens are included, super senior citizens are not

Senior citizens aged 60 to 79 can claim the rebate if they meet the income and residency conditions. Super senior citizens aged 80 and above are generally not considered in this provision because their basic exemption limit under the old regime is already ₹5 lakh, which typically makes them tax-free without needing a rebate. Under the new regime, age-based basic exemption differences do not apply, and super senior citizens who are resident individuals can still be eligible subject to the income limit.

What the rebate does not cover

This is where most confusion happens. The rebate under Section 87A does not apply to every type of income.

Income taxed at special rates is excluded. The rebate applies only to tax computed on income that goes through the regular slab rates. Income taxed at special flat rates is calculated separately and the ₹60,000 rebate does not reduce that tax.

This includes:

- Long-term capital gains under Section 112A (for example, gains on listed shares and equity mutual funds above the exempt limit)

- Short-term capital gains under Section 111A (listed shares and equity mutual funds held for 12 months or less)

- Winnings from lottery, betting, gambling, and online games

- Gains on virtual digital assets such as cryptocurrency and NFTs

If your total income is ₹10 lakh, including ₹2 lakh of long-term capital gains on equity shares, you cannot apply the ₹60,000 rebate to the tax on that ₹2 lakh. The rebate reduces only the tax on the ₹8 lakh of regular-slab income.

Old regime vs new regime — what the rebate actually means in practice

Under the new tax regime

Because the new regime is the default, most taxpayers will be compared against these limits automatically.

- Taxable income up to ₹12 lakh → tax before rebate is up to ₹60,000 → rebate makes it zero → final tax is zero

- For salaried taxpayers, the standard deduction of ₹75,000 applies, so gross salary up to ₹12.75 lakh can effectively result in zero tax

- Most Chapter VI-A deductions (80C, 80D, HRA, etc.) are not available, so “taxable income” under this regime is close to your gross income minus the standard deduction

Under the old tax regime

The old regime is now a conscious opt-in. The rebate limits here have not moved.

- Taxable income up to ₹5 lakh → tax before rebate is up to ₹12,500 → rebate makes it zero

- You can claim 80C, 80D, HRA, home loan interest, and other Chapter VI-A deductions to bring your taxable income down to ₹5 lakh

- This is why two people with the same gross salary may land in very different rebate zones depending on regime choice

The old regime still makes sense for some taxpayers with heavy deductions — home loan borrowers, those maxing out 80C and 80D, people with large HRA claims. For others, the new regime’s ₹12 lakh rebate limit is simply a better deal.

Marginal relief — what happens just above ₹12 lakh

This is the part most blogs skip, but it matters.

Without marginal relief, a taxpayer with taxable income of ₹12,00,001 would lose the entire rebate and face a tax bill of several tens of thousands. To prevent this, the law provides marginal relief: if your income crosses ₹12 lakh slightly, your additional tax payable is capped at the amount by which your income exceeds ₹12 lakh.

For example, if taxable income is ₹12.10 lakh, the extra income above the threshold is ₹10,000. Without relief, tax on ₹12.10 lakh under new-regime slabs would be around ₹61,500. Marginal relief reduces this, so the final tax does not exceed the ₹10,000 of extra income. Relief tapers off as income moves further above ₹12 lakh and stops applying once normal slab tax becomes lower than the extra income amount — roughly around ₹12.75 lakh of taxable income.

Marginal relief applies only under the new regime for AY 2026-27. It is applied automatically by the Income Tax portal when the return is filed correctly.

What this looks like in practice — a decision flowchart

When you should not assume the rebate will save you

The rebate is not a guarantee. You should not plan around it if:

- You are an NRI — you are not eligible, regardless of income level

- Your income includes significant long-term or short-term capital gains on shares or equity mutual funds

- You have income from online gaming, lottery, or virtual digital assets

- You are confused about your residential status for the year — check that first, because an incorrect residency claim can invite scrutiny

- You have income around the ₹12 lakh mark and expect a bonus or additional income — marginal relief helps only in a narrow band, and income clearly beyond ₹12.75 lakh is taxed at regular slab rates

- You are an HUF, firm, or company — the rebate is for individuals only

The 1961 Act vs 2025 Act question

Section 87A as described above sits under the Income Tax Act 1961. The Income Tax Act 2025 has been enacted and is expected to govern future assessment years under the restructured framework. The Union Budget 2025 changes, including the ₹12 lakh rebate and ₹60,000 amount, apply for FY 2025-26 (AY 2026-27) under the 1961 Act. Taxpayers filing returns for AY 2026-27 should apply the provisions as they stand under the 1961 Act. How the rebate is structured under the 2025 Act in its final operational form should be separately reviewed closer to the year it starts applying.

Documents and checks before you assume zero tax

Keep these ready before concluding that your tax will be zero under Section 87A:

- Form 16 or your computed taxable income statement

- A clear calculation of income under each head (salary, house property, business, capital gains, other sources)

- A regime selection confirmation — old or new

- AIS and Form 26AS, to verify all income sources

- A breakup of any capital gains, lottery, or crypto income, separated from regular-slab income

- Proof of residential status for the year, if there is any doubt

Final takeaway

The Section 87A rebate for AY 2026-27 is a genuine benefit for resident individuals — but it is not automatic, not universal, and not all-covering. It applies only to regular-slab tax, only to residents, and only within the income limits of ₹12 lakh under the new regime or ₹5 lakh under the old. Before celebrating zero tax, check your residency, your regime, and whether any part of your income is taxed at special rates. The rebate is powerful, but it rewards taxpayers who understand its edges.

Confused about whether the Section 87A rebate applies to your income, or unsure how capital gains and regime choice affect your final tax for AY 2026-27? eTaxMate can help you review your income composition, confirm your eligibility, and file your ITR correctly.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.