If you are a salaried employee and missed submitting investment proofs to your employer, do not panic. Many people believe that if a deduction was not considered in salary TDS, it is lost forever. That is not always true. The Income Tax portal clearly treats Form 12BB as the form through which an employee gives deduction and exemption details to the employer for salary TDS purposes, while the ITR filing process separately allows the taxpayer to enter and confirm eligible deductions while filing the return.

If you are a salaried employee and missed submitting investment proofs to your employer, do not panic. Many people believe that if a deduction was not considered in salary TDS, it is lost forever. That is not always true. The Income Tax portal clearly treats Form 12BB as the form through which an employee gives deduction and exemption details to the employer for salary TDS purposes, while the ITR filing process separately allows the taxpayer to enter and confirm eligible deductions while filing the return.

Quick answer

Yes, in many genuine cases, a deduction missed in salary can still be claimed in ITR. But before doing that, you must check three things:

- Was the payment or investment actually made?

- Do you have proper proof?

- Is the deduction allowed in your chosen tax regime?

What does “missed investment proofs” mean?

“Missed investment proofs” usually means that the employee did not submit tax-saving documents to the employer in time for salary TDS calculation. This can happen because of late submission, incomplete documents, HR deadline miss, job change during the year, or simple oversight. As a result, the employer may deduct higher TDS from salary.

Typical situations include:

- 80C investment proof not submitted before salary closing

- 80D insurance receipt not uploaded

- HRA documents not given to employer

- home-loan certificate submitted late

- Form 16 not showing the deductions you expected

This is why the topic matters so much for salaried taxpayers in India. The issue is not that the benefit is always lost. The real issue is whether it can still be corrected at return-filing stage.

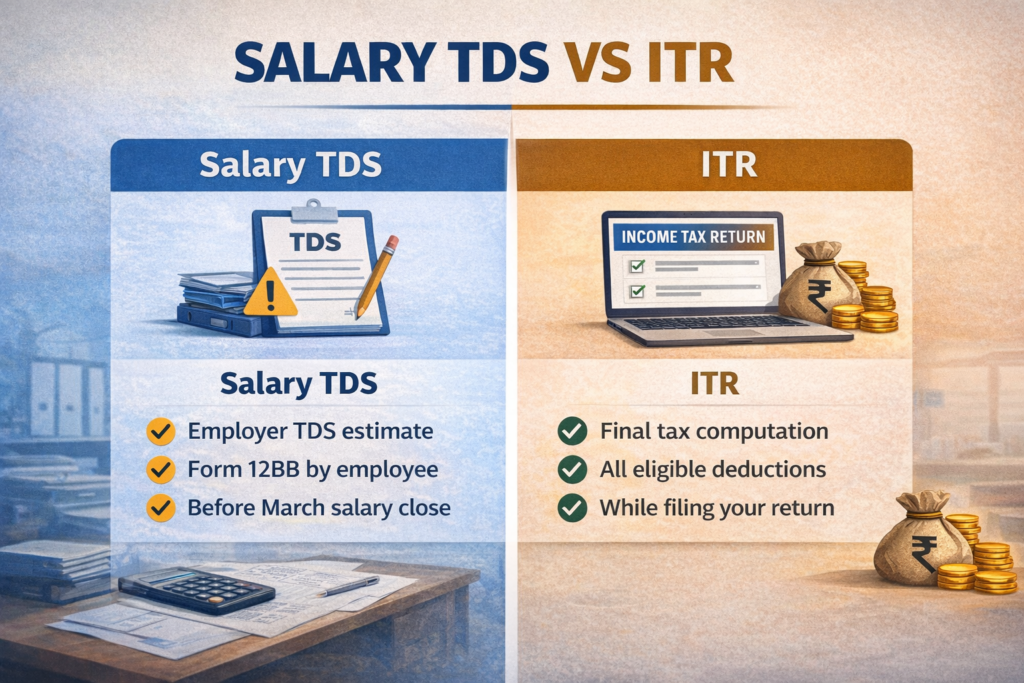

Why salary TDS and ITR filing are not the same

This is the most important concept in the whole article.

At salary stage

At the salary stage, your employer estimates your taxable salary and deducts TDS based on the details available with them. The Income Tax portal specifically lists Form 12BB as the form used by an employee to provide evidence or particulars of HRA, LTC, home-loan interest, and tax-saving claims for the purpose of salary TDS deduction.

At salary stage

At the ITR stage, the taxpayer files the final return and reports total income, taxes paid, and eligible deductions. The official ITR-1 user manual says that under the Total Deductions section, the taxpayer can add, delete, and confirm deductions applicable under Chapter VI-A. The ITR-1 FAQ also says taxpayers must provide all details in the return, including total income, deductions, and taxes paid.

Simple Flowchart

You earn salary

↓

Employer asks for tax proofs / declarations

↓

Employer computes salary TDS

↓

Some deductions may be missed in salary

↓

You file ITR

↓

Final tax liability is computed

↓

Refund or tax payable is determined

What this means

A deduction missed in salary does not automatically mean it is permanently lost. It means the employer did not give that benefit while deducting TDS. The final position may still be corrected in the return, subject to law, proof, and tax regime.

Can you still claim a deduction missed in salary?

The answer is often yes

Many genuine deductions missed in salary can still be claimed in ITR. But this is not automatic. You should only do it when all the following conditions are satisfied.

Condition 1: The deduction must actually be allowed

You cannot claim a deduction merely because you planned to invest or because HR did not consider it. The payment or investment must actually have been made, and the claim must be legally allowable. The ITR filing system allows deduction entry, but not unsupported claims.

Condition 2: You must have proof

If the deduction was missed in salary, documentation becomes even more important. Keep payment receipts, insurance premium receipts, PPF proof, ELSS statement, tuition fee receipts, rent receipts, and home-loan certificates, as applicable. No documents are attached with ITR-1, but that does not reduce the need to keep proper records in case of verification.

Condition 3: Your tax regime must allow the claim

This is where many salaried employees go wrong. The new tax regime is the default regime, and under it, most Chapter VI-A deductions are not allowed except certain specified items. If you want to claim most common salary-related deductions like 80C, 80D, or HRA-linked old-regime benefits, you generally need to be under the old tax regime, subject to conditions.

Old tax regime vs new tax regime — what salaried employees must check

This section is critical because many people think their deduction is missing because of salary processing, when actually the issue is tax regime.

New tax regime

The Income Tax portal’s FAQs say that from AY 2024-25 onward, the new tax regime is the default regime. It also says that most Chapter VI-A deductions are not allowed in the new regime, except specified deductions such as section 80CCD(2), 80CCH, and 80JJAA. It further confirms that HRA exemption is not available in the new regime.

Old tax regime

Under the old regime, various exemptions and deductions can be claimed, subject to conditions. So if your missed claim relates to 80C, 80D, HRA, or home-loan-related old-regime benefit, the regime selection becomes very important.

Standard deduction

The portal FAQ clearly says that standard deduction is available in both old and new tax regimes from AY 2024-25 onward.

Common deductions salaried employees miss before salary closing

1) Section 80C

This may include:

- life insurance premium

- PPF

- ELSS

- tuition fees

- principal repayment of housing loan

- other eligible 80C items depending on facts

These are commonly missed because employees forget to submit the proof before the employer’s salary deadline.

2) Section 80D

Medical insurance premiums for self, spouse, children, or parents may be missed if receipts were not submitted in time. Whether the claim is finally allowed depends on actual payment and legal eligibility.

3) HRA claim

If you paid rent but did not provide rent details or rent receipts to your employer, HRA may not have been considered in salary. But remember, HRA exemption is generally an old-regime benefit and not available in the default new regime.

4) Home-loan related claim

Home-loan interest certificate may not have been submitted to the employer on time. This often creates a mismatch between what the employee expected and what the salary TDS considered. The final claim depends on documents, regime, and legal conditions.

5) Other eligible deductions

Some taxpayers also miss other deductions because they rely only on Form 16. But Form 16 is not the only document you should review before return filing.

What to do if your deduction was not considered in salary

Here is the simplest practical process.

Missed proof submission to employer

↓

Check Form 16

↓

Identify what was not considered in salary

↓

Check if the deduction is legally allowed

↓

Check if your tax regime allows it

↓

Collect proof documents

↓

Cross-check with AIS / 26AS / salary records

↓

Claim correctly in ITR if eligible

↓

Check refund or tax payable

When you should not claim a missed deduction

This is just as important as knowing when you can claim.

You should not claim a deduction if:

- the payment or investment was never actually made,

- you do not have proper proof,

- the deduction is not available in your selected regime,

- the claim is legally not valid,

- you are entering the figure only because it was “supposed” to happen

Documents checklist before claiming deduction in ITR

Before filing, keep these documents ready.

Salary documents

- Form 16

- salary slips

- previous employer salary details, if job changed

Tax data documents

- AIS

- Form 26AS

- bank account details for refund

Proof documents

- life insurance receipts

- PPF proof

- ELSS statement

- tuition fee receipt

- medical insurance receipt

- rent receipts

- home-loan certificate

- any other deduction-related evidence

These documents are essential for review even if they are not uploaded with ITR-1.

Simple decision diagram

Was the deduction missed in salary?

↓

Yes

↓

Was the payment or investment actually made?

↓ Yes ↓ No

Collect proof Do not claim

↓

Is it allowed in your tax regime?

↓ Yes ↓ No

Claim may be possible Do not claim

↓

Cross-check Form 16 / AIS / 26AS

↓

File ITR correctly

Final takeaway for salaried taxpayers

If you missed submitting investment proofs to your employer, do not assume the tax benefit is gone forever. A deduction missed in salary can still be claimed in many genuine cases, but only when the claim is legally valid, supported by proof, and allowed under your tax regime. That is why salaried employees should not file blindly from Form 16 alone. Review Form 16, AIS, Form 26AS, your receipts, and your regime choice before filing.

Missed investment proofs or confused by Form 16, AIS, and tax regime choice? eTaxMate can help you review your salary tax data, identify genuine claims, and file your ITR correctly.