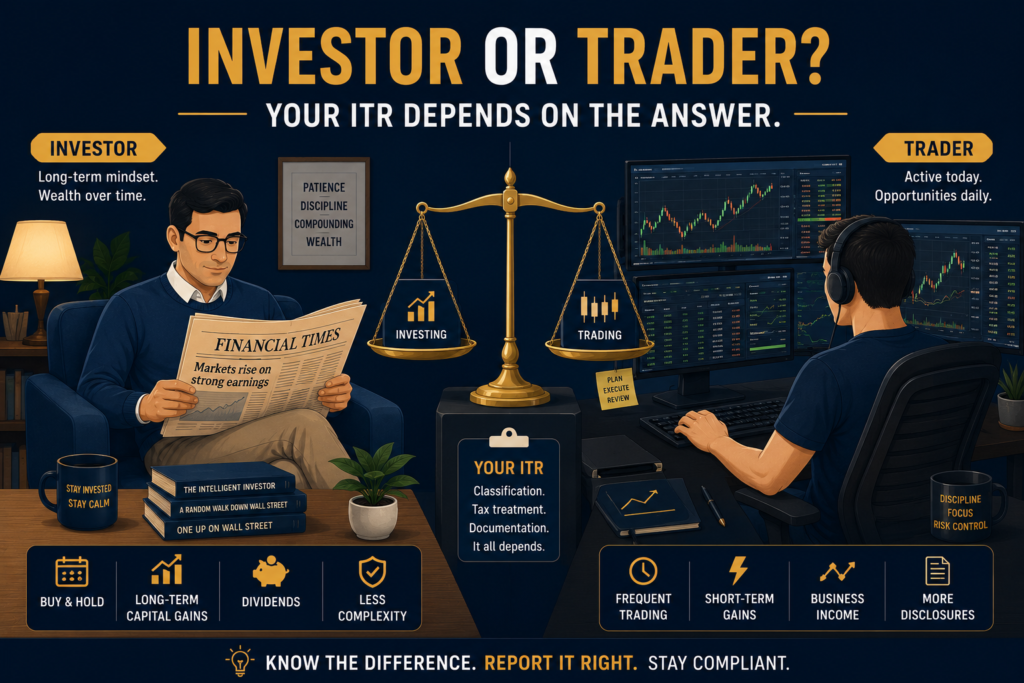

Most people who buy and sell stocks assume their gains are “capital gains” and stop there. That assumption is what attracts notices, defective return flags under Section 139(9), and last-minute panic during scrutiny. The truth is that the same ₹5 lakh profit from the stock market can be taxed completely differently depending on whether the Income Tax Department views you as an investor or a trader. This post explains how the classification works, why it matters for your trading income ITR, and where founders and active market participants commonly get it wrong.

Quick answer

The same stock market profit can be capital gains or business income — the classification depends on your intent, frequency, and trading pattern, not on what you prefer. Intraday equity is always speculative business income. F&O is always non-speculative business income. Delivery-based equity can be either, but once chosen, you must stay consistent year after year.

Before filing, check:

- What type of trades did you do this year — delivery, intraday, F&O, or all three?

- Have you classified delivery-based equity the same way in earlier years?

- Are your books, contract notes, and trading statements in order?

Why this classification matters more than you think

Take two founders, Rahul and Priya. Both earned exactly ₹6 lakh from the stock market in FY 2025-26.

Rahul bought 500 shares of a listed company in April 2024 and sold them in August 2025 after holding for 16 months. His ₹6 lakh gain is long-term capital gain under Section 112A — taxed at 12.5% on the amount above ₹1.25 lakh. His tax on this is roughly ₹59,375 (12.5% of ₹4.75 lakh). He files ITR-2.

Priya did 240 intraday trades and 60 F&O trades during the same year, with a combined net profit of ₹6 lakh. Her entire income is business income — intraday treated as speculative business and F&O as non-speculative business — and taxed at her slab rate. If her other income pushes her into the 30% bracket, her tax on this ₹6 lakh is roughly ₹1.87 lakh including cess. She files ITR-3.

Same profit. Same financial year. Tax outcome differs by more than ₹1.25 lakh. This is why the trading income ITR classification is not a clerical question — it is the question.

What the law actually says about trading income ITR treatment

Three rules form the spine of how stock market income is taxed.

Rule 1 — Intraday equity is always speculative business. Under Section 43(5) of the Income Tax Act 1961, a transaction in which a contract for purchase or sale of stocks is settled otherwise than by actual delivery is a speculative transaction. Buying 100 shares of a company at 10 am and selling them by 3 pm — without taking delivery — falls squarely under this rule. The income or loss is speculative business income, reported under Profits and Gains from Business or Profession (PGBP).

Rule 2 — F&O is always non-speculative business. Section 43(5) carves out an explicit exception for derivatives trading on a recognised stock exchange. Whether you are trading Nifty futures, Bank Nifty options, or commodity futures on a recognised exchange, the gain or loss is non-speculative business income, also reported under PGBP. This treatment is now mirrored in Section 66 of the Income Tax Act 2025, which takes effect for income earned from 1 April 2026 onwards. For FY 2025-26 (AY 2026-27), the 1961 Act still governs.

Rule 3 — Delivery-based equity is a grey zone, governed by CBDT Circular No. 6/2016. This circular gives taxpayers an option for listed shares — either treat all delivery-based equity as capital gains, or treat it all as business income. The catch: once you choose, you must remain consistent year after year. Switching purely to save tax invites scrutiny.

F&O explained: turnover, profit, and what you can actually deduct

F&O trading sits in a place that confuses almost every first-time filer. The contract values run into crores, the P&L looks small, and the broker statement shows half a dozen different numbers. Three things matter for your trading income ITR: turnover, gross profit or loss, and net taxable profit. Each is computed differently, and only the last one is what you pay tax on.

What “turnover” means for F&O — and why it is not the contract value

For F&O, turnover under the Income Tax Act is not the notional contract value. If you bought one lot of Nifty futures at ₹24,500 with a lot size of 25, the contract value is ₹6,12,500 — but that is not your turnover. The ICAI Guidance Note on Tax Audit (8th edition, revised September 2023) clarifies that F&O turnover is the absolute sum of profit and loss across all squared-off trades.

The position is the same for both buyers (holders) and sellers (writers) of futures and options, and the same for both call and put options. What matters is the realised P&L on each trade, not which side of the trade you took.

Futures (holder or writer, long or short): Turnover = sum of absolute profit and absolute loss on each squared-off contract.

Options (holder or writer, call or put): Turnover = sum of absolute profit and absolute loss on each squared-off contract. Under the 2023 ICAI guidance, premium received on sale of options is not separately added if it has already been factored into the net P&L computation — which is how all major brokers (Zerodha, Groww, Upstox, ICICI Direct, Kotak) now report it. This is an important change: earlier (7th edition), sale premium had to be added separately, which inflated turnover significantly for option writers. Most current broker tax P&L statements already follow the simpler 8th edition method.

A quick worked example. Across FY 2025-26, a trader has these results:

- Nifty futures trade 1: profit of ₹15,000

- Nifty futures trade 2: loss of ₹22,000

- Bank Nifty call option (bought): profit of ₹8,000

- Bank Nifty put option (sold/written): loss of ₹40,000

- Reliance futures trade: profit of ₹12,000

Gross P&L = 15,000 − 22,000 + 8,000 − 40,000 + 12,000 = loss of ₹27,000 Turnover = 15,000 + 22,000 + 8,000 + 40,000 + 12,000 = ₹97,000

Notice that the trader has a net loss of ₹27,000, but his turnover is ₹97,000. This is the source of most confusion — turnover is large even when net P&L is small or negative. Turnover is what determines whether tax audit applies; net P&L is what gets taxed.

What expenses can be claimed against F&O income

Because F&O is non-speculative business income, all genuine business expenses incurred to earn that income are deductible under the normal PGBP provisions. The commonly allowable expenses are:

- Brokerage and exchange charges — brokerage, exchange transaction charges, SEBI turnover fees, clearing member charges, stamp duty on contract notes.

- GST on brokerage — fully deductible.

- Securities Transaction Tax (STT) — STT paid on F&O is allowed as a business expense under the proviso to Section 36 of the Income Tax Act 1961. (For capital gains traders, STT is not separately deductible — it is built into the special rate. For F&O traders, the position is different.)

- Internet and telephone bills — proportional, based on use for trading. A reasonable allocation (say 50% if you also use the connection personally) is the standard practice.

- Subscription costs — TradingView, advisory services, market data feeds, financial newspapers and journals, courses directly related to your trading.

- Depreciation on equipment — laptop, desktop, monitors, mobile phone used for trading, at the rates prescribed in the Income Tax Rules.

- Rent — if you use a dedicated room or office space for trading, a proportional share is deductible.

- Salary — if you employ an assistant or analyst for trading-related work.

- Professional fees — fees paid to a Chartered Accountant for tax return filing, advisory, or audit relating to the trading business.

What is not deductible: margin money kept with the broker (it is a deposit, not an expense), losses on unrelated activities, and personal expenses dressed up as business.

Net taxable profit — the only number that matters for tax

The number you pay tax on is:

Net taxable profit = Gross P&L from F&O − Allowable expenses

Continuing the earlier example, suppose the same trader had ₹35,000 of legitimate expenses (brokerage, STT, GST, partial internet bill, depreciation on a laptop, advisory subscription):

- Gross P&L = −₹27,000 (loss)

- Less: Allowable expenses = ₹35,000

- Net taxable income from F&O = −₹62,000 (business loss)

This ₹62,000 is a non-speculative business loss. It can be set off against any other business income, capital gains, house property income, or other sources (but not against salary) in the same year. Any unabsorbed loss can be carried forward for 8 assessment years, provided the ITR is filed within the due date under Section 139(1).

Conversely, if the gross P&L had been a profit of ₹3,00,000, then net taxable F&O income would be ₹3,00,000 − ₹35,000 = ₹2,65,000, taxed at the trader’s applicable slab rate along with the rest of their income.

How this looks in ITR-3

Inside ITR-3, F&O income is reported under Profit & Gains from Business or Profession (PGBP), separately from any speculative (intraday) business. The standard approach used by most active traders:

- Trading Account — Sales side: report F&O turnover (the absolute P&L sum) as “other operating revenue.”

- Trading Account — Purchases/Direct Expenses side: brokerage, STT, exchange charges, GST.

- P&L Account — Indirect Expenses: internet, telephone, depreciation, advisory subscriptions, professional fees.

- Business code: 09028 (retail sale of other products) is commonly used for F&O. There is no F&O-specific code in the ITR utility.

If the trader is not maintaining full books of account, F&O can be reported under the “No Account Case” portion of ITR-3, which only asks for gross receipts (turnover), gross profit, expenses, and net profit. This is acceptable only if turnover is below the audit threshold and the trader is not opting for presumptive taxation.

Investor vs trader: how the Assessing Officer decides

For delivery-based equity, there is no single test. The Assessing Officer looks at the totality of facts. The factors that consistently appear in CBDT guidance and tribunal rulings are:

- Intent at the time of purchase — were the shares bought to earn dividends and hold long-term, or to flip on a short-term price movement?

- Frequency and volume of transactions — a person doing 5 trades a year looks like an investor. A person doing 300 trades a year looks like a trader.

- Holding period — long average holding periods point to investor classification. Days or weeks point to trading.

- Source of funds — own funds suggest investment; borrowed funds or margin funding suggest business.

- Treatment in books and balance sheet — shares shown as “investments” in books support capital gains treatment. Shown as “stock-in-trade” supports business income.

- Whether trading is the main source of income — a salaried professional doing occasional trades is typically an investor. A full-time market participant is typically a trader.

No single factor is decisive. A salaried employee who does 80 short-term trades a year using borrowed funds can be classified as a trader despite their day job. A retired person who does 20 delivery trades using own funds is almost always an investor.

The four buckets of stock market income

Before filing your trading income ITR, slot every trade into one of these four buckets. The infographic below shows how each bucket maps to its tax head, rate, ITR form, and key rule.

How to report trading income ITR-wise: form selection

The form follows the bucket. If you had income from only buckets 1 and 2 (capital gains), ITR-2 is sufficient. The moment you add any intraday or F&O activity, even a single trade, ITR-3 becomes mandatory because intraday and F&O are business income.

A common founder profile — salary plus some delivery investing plus occasional F&O — requires ITR-3. ITR-2 would be a defective return under Section 139(9). Filing the wrong form is one of the top triggers for a defect notice from the Centralised Processing Centre.

For the regime question: capital gains under Sections 111A and 112A are taxed at the special rates regardless of whether you opt for the old or new regime. The choice between old and new regimes affects only your slab-taxed income, including business income from intraday and F&O. Under the new regime, Chapter VI-A deductions like 80C and 80D cannot be claimed. Founders with business income who want to opt out of the default new regime must file Form 10-IEA before the due date.

For internal step-by-step guidance on picking the correct form across all scenarios, see our detailed ITR form selection walkthrough.

When you should not switch your classification

The most expensive mistake is switching from capital gains to business income — or the other way — because the numbers look better one year. CBDT Circular No. 6/2016 gives flexibility, but the operative word is consistent. Switch only when your actual trading pattern has genuinely changed.

Do not switch in these cases:

- You showed delivery gains as STCG for three years, and this year STCG of ₹4 lakh would attract more tax than business slab. A switch purely to save tax is exactly what the department flags during scrutiny.

- You started doing F&O this year and want to absorb F&O losses against earlier years’ capital gains. Speculative and non-speculative business losses follow their own set-off rules. They cannot retrospectively change capital gains classification.

- You want to claim Section 44AD presumptive taxation on F&O. Presumptive taxation is not available for speculative business, and even for non-speculative F&O the treatment is contested. Better to compute actual profit and file ITR-3.

- You did one or two short-term trades and want to bury them as business income to avoid the 20% STCG rate. Two trades do not make a business. The classification will not stand.

For a deeper look at when Section 44AD presumptive taxation genuinely fits a small business, that post covers the eligibility tests in detail.

Documents and records to keep ready

Whether you are filing ITR-2 or ITR-3, gather these before starting:

- Annual profit and loss statement and tax P&L from your broker (Zerodha, Groww, Upstox, ICICI Direct etc.)

- Contract notes for every trade, kept for at least 6 years

- Trading statement segregated by segment (delivery, intraday, F&O)

- Bank statement covering all market-related transactions

- Form 26AS and AIS to reconcile reported STT and STCG/LTCG figures

- For business income filers: ledger of expenses (brokerage, internet, advisory fees, depreciation on equipment used for trading)

- Form 10-IEA acknowledgement if you have opted out of the new regime

- Prior year ITRs to confirm consistency of classification

Final takeaway

Your trading income ITR is not decided by what you call yourself — it is decided by what you actually did during the year. Intraday and F&O are business income, no exceptions. Delivery-based equity gives you a choice, but that choice is binding once made. Mixing buckets is fine in real life; mixing classifications carelessly is what creates trouble. The cleanest filings come from clear separation: one portfolio for long-term investment, another for active trading, both consistently treated year after year. Decide where you belong before you file. The form, the rate, and the audit risk all flow from that one decision.

Trading income ITR confusion or need expert help with classifying delivery, intraday, and F&O correctly? eTaxMate can help you review your trading activity, choose the right ITR form, and file it consistently with your past returns.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. Can I treat my stock market profits as capital gains or business income, whichever saves more tax?

Not freely. CBDT Circular No. 6/2016 gives flexibility only for delivery-based listed equity, and even there the choice must be consistent year after year. Intraday is always speculative business income and F&O is always non-speculative business income — no choice exists for these. Switching classification only to reduce tax is exactly what triggers scrutiny by the Assessing Officer.

2. Which ITR form should I use if I have salary plus some F&O trades?

ITR-3. The moment you have any business income — including a single F&O trade or intraday trade — ITR-2 becomes a defective return. ITR-3 is the correct form for salaried taxpayers with business income alongside, even if the F&O activity is small. Filing ITR-2 in this situation typically results in a defect notice under Section 139(9) from the Centralised Processing Centre.

3. Is intraday trading taxed differently from F&O trading?

Yes. Both are business income but the sub-category differs. Intraday equity is speculative business under Section 43(5) and its losses can only be set off against speculative business gains. F&O is non-speculative business and its losses can be set off against any business income except speculative. The slab rate applies to both, but the loss set-off rules diverge.

4. What is the tax rate on STCG from shares in FY 2025-26?

Short-term capital gains on listed equity shares and equity-oriented mutual funds with STT paid are taxed at 20% under Section 111A for FY 2025-26 (AY 2026-27). This rate was raised from 15% by the Finance Act 2024, effective 23 July 2024. No Chapter VI-A deduction is allowed against this gain and the Section 87A rebate is not available against STCG taxed at this special rate.

5. Is tax audit required for F&O traders?

Tax audit under Section 44AB may apply depending on F&O turnover and profit percentage. Since F&O is business income, the audit triggers under the Act apply. The exact threshold has changed several times — most recently the limit was raised to ₹10 crore where 95% or more transactions are digital. F&O turnover is computed on the absolute sum of profit and loss for each trade, not on the contract value.

6. Can I claim Section 87A rebate against my F&O profits?

Yes, F&O profits are taxed at slab rates and the Section 87A rebate is available against slab-taxed income if total income is within the rebate threshold. However, the rebate is not available against STCG under Section 111A or LTCG under Section 112A, which are taxed at special rates. This is an important distinction for taxpayers with mixed market income — capital gains do not get the rebate, business income does.