If you are a salaried employee at a startup or a listed company and your employer has handed you a stock option grant letter, the first question is almost never about wealth. It is about cash. When does the tax bill arrive, and how do you pay it without selling shares you may not even be able to sell yet? ESOP tax in India trips up otherwise careful taxpayers because it is taxed twice, at two different stages, under two different heads of income. This post explains exactly when each tax is triggered, how it is calculated, and the one provision that can defer the first bill if you work at the right kind of startup.

Quick answer

ESOPs in India are taxed at two stages: as a salary perquisite when you exercise the options, and as capital gains when you sell the shares. There is no tax at grant or vesting. The perquisite is the difference between the fair market value (FMV) on the exercise date and the price you paid. Your employer deducts TDS on this amount at exercise. The capital gains stage applies later, when you sell.

Before exercising your options, check:

- Whether your employer is a DPIIT-recognised startup with Section 80-IAC certification — if yes, the perquisite tax can be deferred.

- Whether the shares are listed or unlisted — this changes the holding period and the capital gains rate.

- Whether you have the cash to pay TDS at exercise without selling shares.

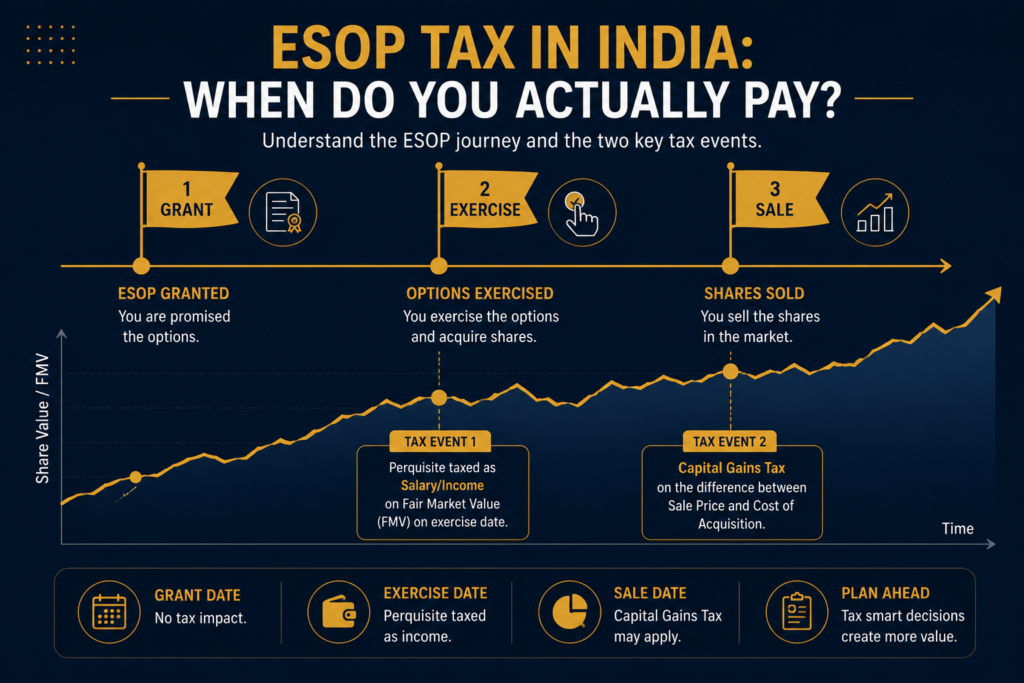

How ESOP tax in India actually works

An Employee Stock Option Plan, or ESOP, gives an employee the right to buy company shares at a fixed price (the exercise price) after a vesting period. The grant itself is just a promise — no money changes hands, no shares are issued, and no tax is payable. Tax kicks in only at two later points: when the employee exercises the option and actually buys the shares, and when the employee later sells those shares.

This two-stage structure is set out in Section 17(2)(vi) of the Income Tax Act 1961, which classifies ESOPs as a perquisite — a non-cash benefit from the employer, taxed as part of salary. The same framework continues under the Income Tax Act 2025, which takes effect from 1 April 2026 with renumbered sections but no change in the substantive ESOP rules. Returns for FY 2025-26 are still filed under the 1961 Act.

A simple example shows how the two stages connect. Rahul, a software engineer at a Bengaluru-based startup, is granted 3,000 options at an exercise price of ₹50. Three years later, he exercises all of them when the FMV is ₹250. He pays his employer ₹50 × 3,000 = ₹1,50,000 and receives the shares. He sells them eighteen months later at ₹400 per share.

The tax events look like this:

- At grant and vesting: No tax.

- At exercise: Perquisite = (₹250 − ₹50) × 3,000 = ₹6,00,000. Added to salary, taxed at slab rate.

- At sale: Capital gain = (₹400 − ₹250) × 3,000 = ₹4,50,000. Taxed under capital gains.

Notice that the FMV at exercise (₹250) becomes the cost of acquisition for the capital gains calculation. The original exercise price of ₹50 is not used again. This avoids double taxation of the same gain.

Stage 1: Perquisite tax at exercise

When an employee exercises ESOPs, the gap between the FMV on that date and the exercise price is a perquisite under Section 17(2)(vi). This amount is added to salary for the year, taxed at the applicable slab rate, and the employer deducts TDS under Section 192 before the shares are allotted.

The FMV is determined under Rule 3(8) of the Income Tax Rules:

- For listed shares: the average of the opening and closing price on the recognised stock exchange on the exercise date.

- For unlisted shares: a valuation report from a SEBI-registered Category I Merchant Banker, valid for 180 days before the exercise date.

This perquisite is fully taxable under both the old and the new tax regime. No deduction or exemption is available against it under either regime.

The cash-flow problem is the real pain point. In the example above, Rahul owes tax on ₹6,00,000 of perquisite income even though he has not sold a single share. At the 30% slab he owes roughly ₹1.8 lakh on paper income. If the company is unlisted and there is no buyer for his shares, that cash has to come from somewhere else. This is exactly the problem the startup deferral was created to solve.

Stage 2: Capital gains tax at sale

When the employee eventually sells the shares, the capital gain is the difference between the sale price and the FMV on the exercise date (not the original exercise price). The rate depends on whether the shares are listed and how long they have been held from the date of allotment.

For sales on or after 23 July 2024:

Listed shares (sold on a recognised exchange with STT paid):

- Holding period for long-term: more than 12 months.

- STCG under Section 111A: 20% (up from 15% earlier).

- LTCG under Section 112A: 12.5% on gains above ₹1.25 lakh per financial year.

Unlisted shares (typical for private startup ESOPs):

- Holding period for long-term: more than 24 months.

- STCG: taxed at the employee’s slab rate.

- LTCG under Section 112: 12.5% without indexation.

If Rahul’s company is listed and he sold after 18 months, his ₹4,50,000 gain is LTCG; after the ₹1.25 lakh exemption, ₹3,25,000 is taxed at 12.5% — about ₹40,625. If the same shares were unlisted, the holding period of 18 months is short-term, and the entire ₹4,50,000 is taxed at his slab — potentially up to 30%. The listed-versus-unlisted distinction can change the bill by several lakhs.

The startup deferral that changes the math

Section 80-IAC of the Income Tax Act, read with Section 192(1C), lets certain startups defer the perquisite TDS — postponing the cash outflow that crushes most ESOP holders. The deferral is not an exemption. The tax is still due, just later.

The deferral applies only if the employer satisfies two conditions:

- The startup is recognised by the Department for Promotion of Industry and Internal Trade (DPIIT).

- The startup has been certified under Section 80-IAC by the Inter-Ministerial Board (IMB) for tax holiday benefits.

Both are needed. DPIIT recognition alone is not enough. As of early 2026, only around 3,700 startups out of nearly two lakh DPIIT-recognised entities hold the Section 80-IAC certificate. The first practical step for any ESOP holder at a startup is to ask HR or finance whether the company has the IMB certificate, not just DPIIT registration.

If the employer qualifies, the perquisite tax is deferred until the earliest of three trigger events:

- Sale of the shares by the employee.

- Cessation of employment with the startup.

- Forty-eight months from the end of the assessment year in which the shares were allotted.

Whichever happens first triggers the tax. The employer must deduct and deposit the TDS within 14 days of the trigger, at the tax rate in force for the year of allotment — not the year of the trigger.

Take Priya, who exercised ESOPs in a Section 80-IAC certified startup. The shares were allotted in March 2026 (FY 2025-26, AY 2026-27). Her perquisite tax is deferred until the earliest of: the day she sells the shares, the day she resigns, or 31 March 2031. She has years of breathing room to wait for a liquidity event.

For ESOP holders at non-qualifying startups or listed companies, no deferral is available — perquisite TDS is deducted on the exercise date, and the cash has to come from somewhere.

Here is how the two tax stages connect across the ESOP lifecycle:

How to report ESOP tax in India in your ITR

The two ESOP tax events go in two different schedules of the income tax return, and getting this wrong is one of the most common triggers for a notice. ESOP holders cannot file ITR-1 (Sahaj) because of the capital gains. Most will file using ITR-2 or ITR-3, depending on whether they have any business income.

Where each amount goes:

- Perquisite value at exercise → Schedule S (Income from Salary), under the perquisites sub-section. This figure is also reflected in Form 16 Part B and Form 12BA.

- Capital gain at sale → Schedule CG (Capital Gains). Report sale date, sale value, cost of acquisition (FMV at exercise), and classify as STCG or LTCG.

- For shares of a foreign parent company → Schedule FA (Foreign Assets) must also be filed if you hold the shares on 31 December of the calendar year ending in the assessment year.

- Eligible startup deferral cases → The perquisite is still disclosed in Schedule S for the year of allotment, with the deferred tax position recorded separately.

Before filing, cross-check your Form 16 perquisite figure against the Annual Information Statement (AIS) on the e-filing portal. Mismatches between Form 16 and AIS are routinely flagged by the department.

When you should pause before exercising

ESOPs feel like a one-way bet — exercise, hold, sell, profit — but the perquisite tax at exercise can turn into a real loss if the share price falls or there is no exit. Step back before exercising if:

- You would need to borrow to pay the perquisite TDS, and the company is unlisted with no clear exit path.

- You are about to leave the company at a non-qualifying startup. Many plans force exercise within 90 days of resignation, triggering tax at the worst possible moment.

- The company’s valuation has dropped but the FMV is still high enough to trigger meaningful tax. Some employees end up paying tax on a paper gain that disappears before sale.

- The shares are under a lock-in or transfer restriction that prevents sale for years. Tax is due now; cash to pay it has to come from elsewhere.

- You are an NRI or about to become one. ESOP perquisite for services rendered in India remains taxable in India even if you exercise from abroad, and the cross-border treatment gets complex quickly.

Exercising ESOPs is rarely a pure tax decision, but it should never be made without a tax calculation done first.

Documents to keep ready

- ESOP grant letter and the company’s ESOP scheme/policy document.

- Exercise notice confirming exercise date and number of shares.

- FMV valuation report from a SEBI-registered Merchant Banker (for unlisted shares).

- Form 16 Part B and Form 12BA from your employer, showing the perquisite value.

- Share allotment certificate or demat statement confirming the allotment date.

- Sale contract notes or broker statements at the time of sale.

- AIS and Form 26AS downloaded from the e-filing portal for cross-verification.

- For startup deferral cases: written confirmation from the employer that the company holds Section 80-IAC certification.

Final takeaway

ESOP tax in India is not one event but two — a salary perquisite at exercise and a capital gain at sale — and the FMV on the exercise date is the hinge that connects them. Most of the pain comes from the first stage, where tax is due on a paper gain before any cash has been realised. Eligible startup employees can defer that pain under Section 80-IAC; everyone else has to plan for it. Whatever your situation, the calculations should happen before the exercise, not after the TDS lands in Form 16.

ESOP-related confusion, or need expert help with exercise planning, perquisite calculation, or ITR reporting? eTaxMate can help you review your grant terms, work out the tax across both stages, and file correctly so the department does not come calling.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. When are ESOPs taxed in India?

ESOPs are taxed at two stages. First, when you exercise the options and shares are allotted to you, the difference between the fair market value and the exercise price is taxed as a salary perquisite under Section 17(2)(vi). Second, when you eventually sell the shares, the gain over the FMV at exercise is taxed as capital gain. There is no tax at the time of grant or vesting.

2. Do I pay tax on ESOPs even if I have not sold the shares?

Yes. The perquisite tax at exercise applies whether or not you sell the shares. You are taxed on the paper gain — the gap between the FMV on the exercise date and the price you paid. The only exception is for employees of startups that are DPIIT-recognised and certified under Section 80-IAC, who can defer the perquisite tax until sale, resignation, or 48 months from the end of the allotment year.

3. How is the fair market value of unlisted ESOP shares calculated?

For unlisted shares, the FMV must be determined under Rule 3(8) of the Income Tax Rules through a valuation report from a SEBI-registered Category I Merchant Banker. The valuation report is valid for 180 days before the exercise date. For listed shares, the FMV is simply the average of the opening and closing price on the recognised stock exchange on the date of exercise.

4. Which ITR form should I use if I have ESOP income?

You cannot use ITR-1 (Sahaj) if you have ESOP capital gains. Most salaried employees with ESOP income file ITR-2. If you also have business or professional income, ITR-3 applies. The perquisite value is reported in Schedule S (salary), the capital gain in Schedule CG, and shares of a foreign parent company may also need disclosure in Schedule FA.

5. What is the difference between DPIIT recognition and Section 80-IAC certification?

DPIIT recognition is the first step — the company registers as a startup with the Department for Promotion of Industry and Internal Trade. Section 80-IAC certification is a separate, much narrower approval granted by the Inter-Ministerial Board, mainly for income tax holiday benefits. ESOP perquisite tax deferral requires both. As of early 2026, only around 3,700 of nearly two lakh DPIIT-recognised startups hold the Section 80-IAC certificate.

6. How are ESOPs of a foreign parent company taxed for Indian employees?

The exercise-stage perquisite is taxable in India under Section 17(2)(vi) because the benefit relates to services rendered in India. The capital gain on sale is also taxable in India for residents. Additionally, if you hold the foreign shares on 31 December of the relevant calendar year, you must report them in Schedule FA of your ITR. Non-disclosure of foreign shares attracts penalties under the Black Money Act.