Many homeowners assume that reporting rental income in ITR means writing down the rent they received and moving on. That is the single most common mistake in this part of the return. Rental income is never one number — it is a small calculation with at least three moving parts, and getting any of them wrong either inflates your tax or invites a notice. Whether you own one flat you rent out or a house you live in with a home loan, this post explains exactly what goes into your rental income ITR reporting and what you are allowed to deduct.

Quick answer

Rental income in your ITR is not the rent you receive — it is the net figure after a 30% standard deduction and home loan interest, reported under “Income from House Property.” What you can claim depends on whether the property is self-occupied or let out, and on which tax regime you choose.

Before acting, check:

- Is the property self-occupied, let out, or deemed let out?

- Are you filing under the old or the new tax regime?

- Do you have a home loan, and is the interest within the limit that applies to you?

Why rental income in ITR is never a single number

Rental income is taxed under a head called “Income from House Property” in the Income Tax Act 1961. The return you file in 2026 covers FY 2025-26 (AY 2026-27), and even though the new Income Tax Act 2025 took effect on 1 April 2026, this return is still governed entirely by the old Act. So the rules below are the rules that apply to the return in front of you.

The reason rent is never a single line is that the law lets you reduce the rent before it is taxed. You start with the rent, subtract a couple of allowed amounts, and the smaller figure that remains is what actually gets added to your income. Skip those subtractions and you overpay. Claim ones you are not entitled to and you risk a correction.

How income from hosue property is built up, step by step

Think of it as a short ladder, each rung subtracting something from the one above.

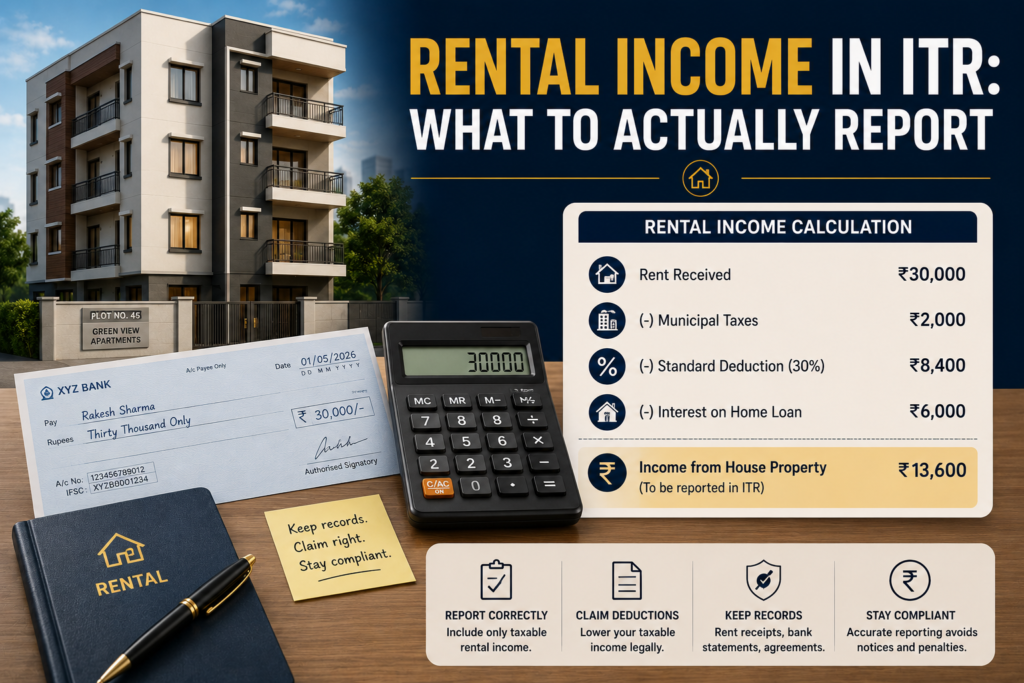

1. Gross Annual Value (GAV). This is essentially the rent the property can reasonably fetch in a year. For a normally let-out property, it is the actual rent received or receivable.

2. Less: municipal taxes paid. Property tax, sewerage tax and similar municipal charges are deductible — but only the portion you actually paid during the year, and only if you (not the tenant) paid them. What remains after this subtraction is the Net Annual Value (NAV).

3. Less: 30% standard deduction under Section 24(a). This is a flat 30% of the Net Annual Value, allowed automatically to cover repairs, maintenance, and upkeep. You do not need bills or proof — it is given regardless of what you actually spent. This single deduction is the one most homeowners forget to claim.

4. Less: home loan interest under Section 24(b). If you took a loan to buy, build, or repair the property, the interest is deductible. For a let-out property, the entire interest is allowed with no ceiling. For a self-occupied property, the deduction is capped at ₹2 lakh in a year, and only under the old regime.

Take Rahul, who rents out a flat for ₹25,000 a month — ₹3 lakh a year. He paid ₹15,000 in municipal taxes, so his NAV is ₹2.85 lakh. The 30% standard deduction is ₹85,500. If he also paid ₹1.2 lakh in home loan interest, his taxable house property income is ₹2.85 lakh minus ₹85,500 minus ₹1.2 lakh — about ₹79,500, not the ₹3 lakh he received. The difference is entirely legitimate.

Self-occupied, let-out, or deemed let-out

The category of the property changes everything, so settle this first.

Self-occupied. A house you live in has a Gross Annual Value of zero — you are not earning rent from it. You cannot claim the 30% standard deduction (there is no NAV to apply it to), but you can claim home loan interest up to ₹2 lakh under the old regime. You may treat up to two houses as self-occupied.

Let out. A property you rent earns rent, so it carries a GAV, the 30% deduction, and unlimited interest deduction.

Deemed let out. If you own more than two houses and none are rented, the law treats the extra ones as if they were let out, and you must report a notional rent on them even though no money changed hands. This catches many people who own an inherited second flat lying empty.

If you own more than two house property, you cannot use the simplest form, ITR-1 — you will need ITR-2. Confirming which ITR form you must file before you start saves a re-filing later.

Old regime vs new regime for rental income

This is where the two regimes diverge sharply, so read carefully.

Under the old regime, a self-occupied home gives you home loan interest up to ₹2 lakh. For a let-out property, you claim the full interest, and if that interest exceeds the rent (creating a loss under house property), you can set off that loss against other income such as salary, up to ₹2 lakh in a year.

Under the new regime, which is the default for AY 2026-27, the position is tighter. You get no interest deduction at all on a self-occupied house. For a let-out property, you can still deduct the full interest against the rental income from that property — but if that produces a loss, you cannot set it off against your salary or other income. The loss simply cannot be used.

The practical effect: a homeowner with a large home loan on a let-out flat often finds the old regime more valuable, because the loss set-off against salary can be worth real money. Run both before deciding. The home loan interest deduction in detail is worth understanding fully before you commit to a regime.

How to report your rental income correctly

Work through it in this order rather than typing rent straight into the form.

First, decide the category of each property — self-occupied, let out, or deemed let out. Second, for let-out property, total the actual rent received for the year as your Gross Annual Value. Third, subtract the municipal taxes you actually paid to arrive at Net Annual Value. Fourth, apply the 30% standard deduction. Fifth, subtract eligible home loan interest within the limit for your category and regime. Sixth, check your AIS — high-value rent and TDS on rent (where the tenant deducts it) now appear there, so your reported figure should reconcile with it.

When you should not report rent the easy way

Some situations need more care than simply entering a rent figure:

- You own more than two houses. The extra ones may be deemed let out, and you must report notional rent even if they are empty. Ignoring this is a common omission that the department can question.

- Your tenant deducted TDS on rent. Rent above the monthly threshold attracts TDS by the tenant. That TDS appears in your Form 26AS and AIS, so your reported rent must match it.

- You received rent in cash or part-year. Report the rent for the actual period let out, and do not assume cash rent is invisible — AIS and high-value transaction reporting increasingly capture it.

- You co-own the property. Rent and deductions must be split in the ownership ratio. Each co-owner reports only their share, not the whole.

When the property is anything other than a single, clearly let-out flat, slow down and confirm the category before you file.

Quick checklist before you file

📋 Keep these ready for your house property entries:

- Rent agreement and a record of actual rent received during FY 2025-26

- Municipal tax receipts for taxes you paid during the year

- Home loan interest certificate from your lender

- TDS details if your tenant deducted tax on rent (check Form 26AS)

- Co-ownership ratio, if the property is jointly owned

- Your AIS, to reconcile reported rent and TDS — part of your complete ITR filing checklist

Final takeaway

Rental income in your ITR is a calculation, not a figure you copy off a rent receipt. Start with the rent, subtract municipal taxes to reach Net Annual Value, take the 30% standard deduction, then apply home loan interest within the limit for your property type and regime. Settle the property category first, choose your regime knowing how the loss set-off differs, and reconcile everything against your AIS. Do that, and the most error-prone part of a homeowner’s return becomes one of the simplest.

Rental income confusion, or unsure how to report a let-out, self-occupied, or jointly owned property correctly? eTaxMate can help you classify your property, calculate the right deductions, and file your return accurately for AY 2026-27.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. How is rental income calculated for ITR?

You start with the rent received as Gross Annual Value, subtract the municipal taxes you paid to get Net Annual Value, then take a flat 30% standard deduction under Section 24(a), and finally subtract home loan interest under Section 24(b). The figure that remains is your taxable income from house property — usually much lower than the rent itself.

2. What is the 30% standard deduction on rental income?

Under Section 24(a), you can deduct a flat 30% of the Net Annual Value of a let-out property to cover repairs and maintenance. It is allowed automatically, regardless of what you actually spent, so you need no bills or proof. It does not apply to a self-occupied house, which has no Net Annual Value.

3. Can I claim home loan interest on rental income under the new regime?

Yes, for a let-out property you can deduct the full home loan interest against its rental income under the new regime. But if the interest creates a loss, you cannot set that loss off against your salary or other income, unlike under the old regime. A self-occupied house gets no interest deduction at all under the new regime.

4. Do I have to report rent on a house I am not renting out?

Possibly. You can treat up to two houses as self-occupied with zero rent. If you own more than two and the extra ones are empty, the law deems them let out and you must report a notional rent on them. This commonly catches owners of an inherited or unused second property.

5. Which ITR form should I use for rental income?

If you own only one house property, ITR-1 may be enough. If you own more than one house property, you must use ITR-2. Choosing the wrong form leads to a defective return and re-filing, so confirm your form before you start based on how many properties you own and your other income.

6. How is rental income reported when a property is jointly owned?

Each co-owner reports only their share of the rent and the related deductions, in the same ratio as their ownership. You do not report the entire rent on one owner’s return. Splitting it incorrectly can cause mismatches with the AIS, so agree the ownership ratio and report consistently across both returns.