Most salaried taxpayers report their salary carefully and then forget the one thing that quietly trips up thousands of returns every year — interest income. The interest your savings account earns, the maturity on a fixed deposit, the small amount on a recurring deposit: all of it is taxable, and all of it is now visible to the department through your AIS. Fixed deposit interest is the single most commonly missed item, because banks deduct TDS on it and people assume that settles the matter. It does not. This post explains exactly where interest income goes in your ITR and how to report it without inviting a mismatch.

Quick answer

Interest income in your ITR is fully taxable and goes under the head “Income from Other Sources” — including savings, FD, and RD interest — even if the bank already deducted TDS on it. You can claim a small deduction on savings interest under Section 80TTA, but only under the old regime.

Before acting, check:

- Have you added up interest from every bank, FD, and post office account?

- Does your reported interest match the figure in your AIS?

- Are you in the old regime (where 80TTA applies) or the new regime (where it does not)?

Why interest income is the most commonly missed item

The problem is a simple misunderstanding. When a bank pays FD interest, it often deducts TDS — tax deducted at source — and many people assume that the bank has therefore “handled the tax.” That is wrong on two counts. First, TDS is usually deducted at 10%, which may be less than your actual slab rate, so more tax can be due. Second, even where TDS covers the full amount, you must still report the interest in your return.

The return you file in 2026 is for FY 2025-26 (AY 2026-27) and is governed by the Income Tax Act 1961, even though the new Income Tax Act 2025 came into force on 1 April 2026. So the rules below are the ones that apply to this return.

What has changed the stakes is the AIS — the Annual Information Statement. Banks now report your interest directly to the department, and it pre-fills into your return. If you leave out FD interest that your bank has already reported, the gap surfaces immediately. The era of quietly omitting interest is over.

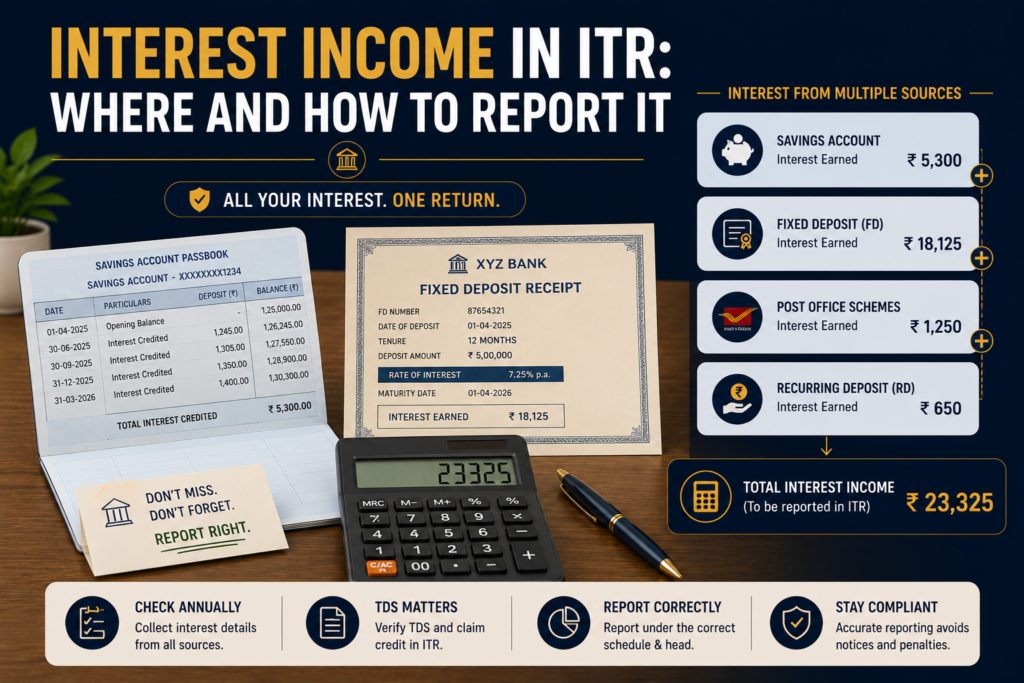

The kinds of interest you must report

All of the following are taxable and must be added up:

1. Savings account interest. The interest your savings balance earns through the year. Banks do not deduct TDS on this, which is exactly why people forget it — there is no deduction to remind them.

2. Fixed deposit (FD) interest. Taxable on accrual each year, not only at maturity. Even if you have not withdrawn it, the interest credited during the year is income for that year. This is the most commonly missed item.

3. Recurring deposit (RD) interest. Treated the same as FD interest — fully taxable.

4. Post office and small savings interest. Interest on post office deposits and similar schemes is taxable too, with limited exceptions.

5. Interest on income tax refunds and bonds. If you received interest on a tax refund, that is also taxable.

Take Priya, a salaried professional with ₹6,000 of savings interest, ₹40,000 of FD interest, and ₹4,000 of RD interest. Her total interest income is ₹50,000 — every rupee of which must be reported, regardless of whether any TDS was deducted. She cannot report only the FD on which TDS appeared and skip the rest.

Where interest income goes in your ITR

Interest income is reported under the head “Income from Other Sources.” It is not salary and it is not capital gains — it has its own slot in the return, and it is added to your total income and taxed at your normal slab rate.

If your only income is salary and interest, and the interest is from ordinary bank or post office accounts, ITR-1 is usually sufficient. More complex interest situations may push you to ITR-2, so it is worth confirming which ITR form applies to you before you begin.

Section 80TTA and 80TTB: the deduction that depends on your regime

This is where the regime choice matters, so read carefully.

Section 80TTA allows a deduction of up to ₹10,000 on savings account interest (not FD or RD interest) for individuals below 60. So if your savings interest is ₹6,000, the whole ₹6,000 is deductible; if it is ₹15,000, only ₹10,000 is.

Section 80TTB is for resident senior citizens (60 and above) and is more generous — a deduction of up to ₹50,000 covering both savings and deposit interest, including FDs. A senior citizen claims 80TTB instead of 80TTA, not both.

The catch: both deductions are available only under the old tax regime. Under the new regime, which is the default for AY 2026-27, neither 80TTA nor 80TTB can be claimed, and all your interest income is taxable in full. This is one more line item to weigh when you compare the two regimes. If your interest income is significant, understanding the difference between the old and new regime in full can change which one is better for you.

TDS on interest is not the same as tax paid

This distinction causes more confusion than almost anything else in interest reporting.

When interest crosses a threshold, the bank deducts TDS under Section 194A. For FY 2025-26, that threshold on bank interest is ₹50,000 for non-senior citizens and ₹1,00,000 for senior citizens. Below the threshold, no TDS is deducted — but the interest is still fully taxable and must still be reported. People often read “no TDS” as “no tax,” which is a costly error.

Equally, TDS deducted is not your final tax. It is an advance against your liability. If your slab rate is higher than the 10% usually deducted, you owe the difference. If your slab is lower or your income is below the taxable limit, the excess TDS comes back to you as a refund — but only if you file and claim it. The TDS shows up in your Form 26AS, and you claim credit for it in the return.

How to report your interest income correctly

Work through this in order.

First, gather an interest certificate or statement from every bank, and note the interest on each FD and RD. Second, total all of it — savings, FD, RD, post office, refund interest — into one figure. Third, download your AIS and check that your total matches what the banks reported; learning how to read your AIS before filing is the step that catches most omissions. Fourth, enter the total under “Income from Other Sources.” Fifth, if you are on the old regime, claim 80TTA (or 80TTB if you are a senior citizen). Sixth, check Form 26AS for any TDS on interest and claim credit for it so you are not taxed twice.

When you should not assume interest is tax-free

A few situations regularly catch salaried filers out:

- No TDS was deducted. Below the ₹50,000 threshold no TDS applies, but the interest is still fully taxable. Treat “no TDS” as a reporting duty, not a free pass.

- You only checked your FD interest. Savings interest carries no TDS and so leaves no trail in Form 26AS — but it is in your AIS and still taxable. Add it.

- Your FD spans multiple years. Interest is taxable on accrual each year, not all at once on maturity. Reporting it only at maturity bunches several years’ income into one and can push you into a higher slab.

- You are on the new regime expecting 80TTA. It is not available there. Do not enter the deduction; it will be disallowed.

- Interest belongs to a minor or spouse. Clubbing rules may apply, and the interest may need to be reported on your return rather than theirs.

If your interest comes from several sources or older deposits, slow down and total everything before you file.

Quick checklist before you file

📋 Keep these ready for your interest income entries:

- Interest certificates from every bank and post office for FY 2025-26

- FD and RD interest figures, on accrual basis, for each deposit

- Savings account interest for the year (often not on any certificate — check the statement)

- Form 26AS, to claim credit for any TDS deducted on interest

- Your AIS, to reconcile total reported interest before submitting

- Your age and residential status, to know whether 80TTA or 80TTB applies

Final takeaway

Interest income is small in amount but large in trouble if missed. Every rupee of savings, FD, RD, and post office interest is taxable and goes under “Income from Other Sources,” whether or not the bank deducted TDS. Add up everything, reconcile it against your AIS, claim 80TTA or 80TTB only if you are on the old regime, and take credit for any TDS in Form 26AS. Do that, and the most commonly overlooked item in a salaried return stops being a source of notices.

Unsure how to report FD or savings interest, or whether you can claim Section 80TTA in your regime? eTaxMate can help you total your interest income correctly, reconcile it with your AIS, and file your return accurately for AY 2026-27.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. Is FD interest taxable even if TDS was deducted?

Yes. FD interest is fully taxable regardless of whether the bank deducted TDS. TDS is usually only 10%, which may be less than your slab rate, so more tax can be due. And even when TDS covers the full amount, you must still report the interest in your return. TDS is an advance against your tax, not the final tax.

2. Where do I report interest income in my ITR?

Interest income is reported under the head “Income from Other Sources.” This includes savings account interest, fixed deposit and recurring deposit interest, post office interest, and interest on tax refunds. It is added to your total income and taxed at your normal slab rate, separately from salary or capital gains.

3. Can I claim Section 80TTA under the new tax regime?

No. Section 80TTA, which allows up to ₹10,000 of savings account interest as a deduction, is available only under the old regime. The same applies to Section 80TTB for senior citizens. Under the new regime, which is the default for AY 2026-27, your full interest income is taxable with no such deduction.

4. Is savings account interest taxable if no TDS was deducted?

Yes. Banks do not deduct TDS on savings account interest, but that does not make it tax-free. It is fully taxable under “Income from Other Sources” and appears in your AIS. Under the old regime you can claim up to ₹10,000 against it through Section 80TTA, but the interest itself must still be reported.

5. What is the difference between Section 80TTA and 80TTB?

Section 80TTA gives individuals below 60 a deduction of up to ₹10,000 on savings account interest only. Section 80TTB is for resident senior citizens and is broader — up to ₹50,000 covering savings, FD, and RD interest. You can claim one or the other, not both, and only under the old regime.

6. When is FD interest taxed — every year or at maturity?

FD interest is taxed on accrual, meaning each year as it is credited, not only when the deposit matures. Reporting it all at maturity bunches several years of income into one and can push you into a higher slab. Report the interest credited during FY 2025-26 in this year’s return, even if you have not withdrawn it.