If you changed jobs and withdrew your provident fund instead of transferring it, you may have a tax bill you did not expect. Many salaried employees believe EPF money is always tax-free because it came from their own salary. That is true only after a point. Before that point, an EPF withdrawal can be fully taxable, the EPFO can deduct TDS on it, and you must report it in your return. The single fact that decides the EPF withdrawal tax is how long you stayed in continuous service. This post explains when withdrawal becomes taxable, how it is taxed, and how to report it correctly.

Quick answer

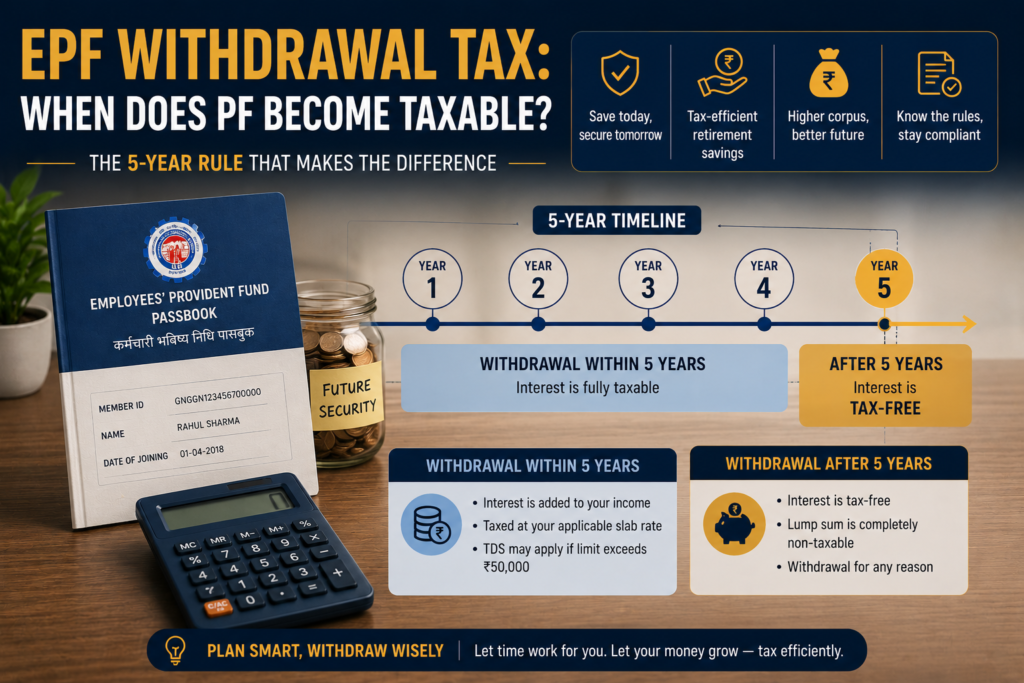

An EPF withdrawal is tax-free if you have completed five years of continuous service. Withdraw before five years and the amount is generally taxable, with TDS under Section 192A if it exceeds ₹50,000. Whether it is taxable turns almost entirely on the length of your service, not the size of the corpus.

Before acting, check:

- Have you completed five years of continuous service, counting all employers if you transferred your PF?

- Is your withdrawal above or below ₹50,000?

- Did the EPFO deduct TDS, and does it show in your Form 26AS?

The five-year rule that decides everything

The whole question of EPF withdrawal tax comes down to one threshold: five years of continuous service. Complete five years and your withdrawal is exempt from tax under Section 10(12) of the Income Tax Act 1961. Withdraw before five years and the amount is generally taxable.

Two points matter here. First, “continuous service” counts your time across all employers if you transferred your PF balance from one to the next. If you worked three years at one company, transferred your PF, and then worked two more years at the next, you have completed five years — even though no single job lasted that long. Second, if you withdrew the PF when changing jobs instead of transferring it, the clock resets.

The return you file in 2026 is for FY 2025-26 (AY 2026-27) and follows the Income Tax Act 1961, even though the new Income Tax Act 2025 took effect on 1 April 2026. So the five-year rule as described here is what applies to this return.

When EPF withdrawal becomes taxable

Putting the conditions together, your EPF withdrawal is taxable when all of these are true:

- You withdrew before completing five years of continuous service, and

- The withdrawal was not for a reason the law treats as beyond your control.

The law spares certain situations even before five years. If your service ended because of ill health, because your employer’s business closed, or for another reason genuinely beyond your control, the withdrawal is not taxed. But withdrawing simply because you switched jobs, or to fund a purchase, does not qualify — those remain taxable if you are under five years.

Take Rahul, who worked for three years, did not transfer his PF when he changed jobs, and withdrew ₹2 lakh to fund a personal expense. Because he had under five years of service and the reason was not one the law exempts, his withdrawal is taxable. Contrast Priya, who worked four years and withdrew her PF only because her employer shut down the business — her withdrawal is not taxed, because the exit was beyond her control.

How a taxable withdrawal is actually taxed

This is the part most people get wrong. A taxable EPF withdrawal is not one lump taxed in one way. The corpus has parts, and they are taxed differently:

- Your own contribution — not taxed again as income (it was already taxed salary), but if you claimed Section 80C deductions on it in earlier years, those deductions are effectively reversed and added back.

- Interest on your own contribution — taxable as “Income from Other Sources.” If you have other interest income, you would report it under Income from Other Sources alongside it.

- Employer’s contribution — taxable under the head “Salary.”

- Interest on the employer’s contribution — also taxable as salary.

So a withdrawal can affect both your salary income and your other-sources income in the year you receive it, and can claw back deductions you took years earlier. The exact split should come from your EPF statement. The practical takeaway: a taxable withdrawal usually costs more than the 10% TDS suggests, because it is taxed at your slab rate across more than one head.

TDS under Section 192A is not the full story

When you withdraw before five years and the amount exceeds ₹50,000, the EPFO deducts TDS under Section 192A — usually at 10% if you have furnished your PAN. If you have not furnished a valid PAN, the rate is far higher, so always provide your PAN.

But two things are widely misunderstood. First, if your withdrawal is ₹50,000 or less, no TDS is deducted — yet the amount can still be taxable if you are under five years. No TDS does not mean no tax. Second, TDS is only an advance against your final tax. At 10%, it may be less than your slab rate, so more may be due; or if your total income is low, the excess comes back as a refund — but only if you file and claim it. The TDS appears in your Form 26AS.

If your total income for the year is below the taxable limit, you can submit Form 15G (or Form 15H if you are a senior citizen) to the EPFO to avoid TDS in the first place — but only when your income genuinely falls below that limit.

How to report a taxable EPF withdrawal in your ITR

Work through it in order.

First, confirm whether you crossed five years of continuous service, counting transfers — if you did, the withdrawal is exempt and there is nothing to tax.

Second, if you are under five years and no exemption applies, get the component breakup from your EPF passbook.

Third, report the employer’s contribution and its interest under “Salary,” and the interest on your own contribution under Income from Other Sources.

Fourth, add back any Section 80C deductions you had claimed on your own contribution.

Fifth, claim credit for the TDS using your Form 26AS so you are not taxed twice on the same amount. The form you use will be ITR-1 or ITR-2 depending on the rest of your income, so confirm which ITR form applies to your situation.

When you should not rush to withdraw

The tax cost of an early withdrawal is often avoidable, so step back in these situations:

- You are close to the five-year mark. Waiting a few months to cross five years can turn a fully taxable withdrawal into a fully exempt one. The corpus does not change; the tax treatment does.

- You are only changing jobs. Transferring your PF to the new employer keeps the clock running and avoids both tax and TDS. Withdrawing resets it.

- Your PAN is not linked to Aadhaar. An inoperative PAN is treated as no PAN, and TDS is then deducted at a much higher rate. Fix the linkage before withdrawing.

- You assume a small withdrawal is invisible. Even a ₹50,000-or-less withdrawal with no TDS can be taxable if you are under five years. Report it.

Withdrawing PF before five years should be a last resort, not a default when you switch employers.

Quick checklist before you file

📋 Keep these ready if you withdrew EPF during FY 2025-26:

- Your EPF passbook showing the component breakup (own and employer contribution, plus interest on each)

- Total period of continuous service, including transfers across employers

- Form 26AS, to confirm any Section 192A TDS deducted

- Your AIS, to reconcile the withdrawal reported by the EPFO

- Records of any Section 80C deduction claimed on your own EPF contribution in earlier years

- The reason for exit, if you are claiming an exemption for an exit beyond your control

Final takeaway

EPF withdrawal tax hinges on one fact: did you complete five years of continuous service, counting transfers? Cross that line and the withdrawal is exempt. Fall short and it is generally taxable — across both salary and other-sources income, with earlier 80C deductions clawed back, and TDS under Section 192A if it exceeds ₹50,000. TDS is not the final word; report the withdrawal, claim the TDS credit, and pay or recover the balance through your return. When in doubt, transferring beats withdrawing.

EPF withdrawal confusion, or unsure whether your PF is taxable and how to report it across salary and other sources? eTaxMate can help you check your service period, work out the taxable portion, and file your return correctly for AY 2026-27.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. Is EPF withdrawal taxable before 5 years?

Yes, generally. If you withdraw your EPF before completing five years of continuous service, the amount is taxable unless your exit was for a reason beyond your control, such as ill health or your employer’s business closing. After five years of continuous service, the withdrawal is fully exempt under Section 10(12) of the Income Tax Act.

2. Does service with different employers count towards 5 years?

Yes, if you transferred your PF balance from one employer to the next. Three years at one job plus two years at another counts as five years of continuous service, provided the PF was transferred rather than withdrawn. If you withdrew the PF when changing jobs, the five-year clock resets from your new employment.

3. How much TDS is deducted on early EPF withdrawal?

Under Section 192A, if you withdraw before five years and the amount exceeds ₹50,000, the EPFO deducts TDS at 10% when you have furnished your PAN. If you have not furnished a valid PAN, the rate is much higher. If your withdrawal is ₹50,000 or less, no TDS is deducted, but the amount may still be taxable.

4. Do I have to report EPF withdrawal in my ITR if TDS was already deducted?

Yes. TDS under Section 192A is only an advance against your final tax, not the full liability. You must still report the taxable withdrawal in your return. At 10%, the TDS may be less than your slab rate, so more tax can be due — or if your income is low, the excess comes back as a refund only when you file and claim it.

5. How is a taxable EPF withdrawal taxed?

It is taxed in parts. The employer’s contribution and the interest on it are taxed under “Salary.” The interest on your own contribution is taxed under “Income from Other Sources.” Your own contribution is not taxed again, but any Section 80C deduction you claimed on it in earlier years is added back. So it is taxed at your slab rate across more than one head.

6. Can I avoid tax on EPF withdrawal when changing jobs?

Yes. Instead of withdrawing your PF when you switch jobs, transfer the balance to your new employer’s EPF account. This keeps your continuous service running, so once you cross five years in total, any later withdrawal is fully exempt. Withdrawing instead resets the clock and can make an early withdrawal taxable.