“Income up to ₹12 lakh is tax-free now.” You have seen that line shared a hundred times, and it is mostly true — but the part everyone leaves out is what makes it true and where it quietly stops applying. The rebate under section 87A is the single provision doing all that work, and it comes with conditions that catch people out every filing season: it depends on your regime, it excludes certain kinds of income entirely, and it works very differently for someone earning a salary versus someone sitting on capital gains. This post separates what the rebate actually does from the myths people keep forwarding.

Quick answer

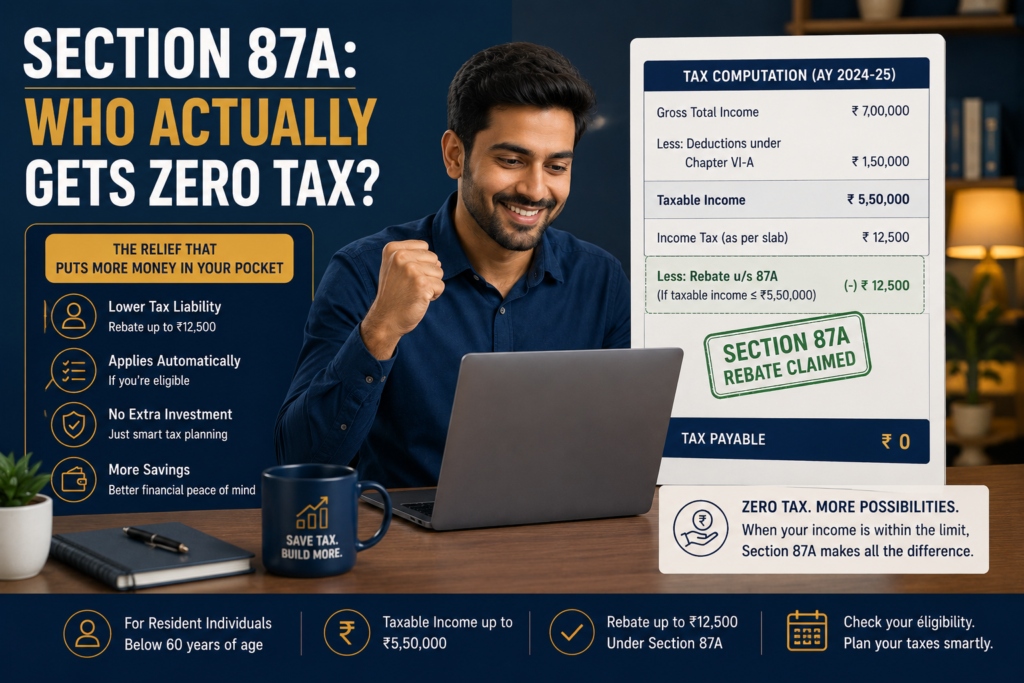

The rebate under 87A is a direct cut to your tax bill — not your income — that can bring your tax to zero if you stay within the limits. For AY 2026-27, it is up to ₹60,000 under the new regime for taxable income up to ₹12 lakh, and up to ₹12,500 under the old regime for income up to ₹5 lakh.

Before you assume you owe nothing, check:

- Are you a resident individual? (NRIs cannot claim it.)

- Is your income ordinary salary/interest, or does it include capital gains taxed at special rates?

- Is your taxable income just over the threshold, where marginal relief matters?

What the rebate under section 87A actually is

A rebate is not a deduction, and the difference is the whole point. A deduction like Section 80C reduces your taxable income before tax is calculated. A rebate reduces the tax itself, after it has been calculated. The rebate under 87A is applied at the very end: you work out your tax on slab rates, and then 87A knocks money straight off that figure.

Section 87A provides a tax rebate, not a deduction, that directly reduces your tax liability to zero if your income is within the threshold. This is why “zero tax up to ₹12 lakh” works — the slab tax is calculated, and then the rebate wipes it out. It sits under the Income Tax Act 1961, which still governs AY 2026-27, since the Income Tax Act 2025 only takes effect for income earned from 1 April 2026 onwards. Taxgarden

The limits under each regime for AY 2026-27

This is where the two regimes split sharply, so know which one you are in. For a clear breakdown of which suits you, see our explainer on the [old versus new tax regime].

Under the new tax regime (the default), the rebate is up to ₹60,000, making taxable income up to ₹12 lakh effectively tax-free. Under the old tax regime, the rebate is ₹12,500, making taxable income up to ₹5 lakh tax-free. The old-regime figure has not moved; only the new-regime limit jumped in Budget 2025. Cleartax

For a salaried person, there is a bonus layer. The standard deduction is subtracted from salary before the rebate is even tested. Because salaried employees get a ₹75,000 standard deduction under the new regime, salary income up to ₹12,75,000 becomes effectively tax-free. Take Rahul, a salaried professional earning ₹12.7 lakh: his [standard deduction] of ₹75,000 brings his taxable income under ₹12 lakh, the rebate then zeroes out his tax, and he pays nothing. Taxgarden

Who can claim it, and who cannot

The rebate under 87A is narrow by design. It is only for resident individuals. Non-residents are not eligible, and HUFs, firms, and companies cannot claim it either — it is strictly an individual-resident benefit. Senior and super-senior citizens who are residents do qualify, on the same income conditions as everyone else. Cleartax

So an NRI earning ₹6 lakh of taxable income in India does not get the rebate that a resident on the same income would. This single condition is behind a large share of the confusion in forwarded messages, which almost never mention residency.

The income that the rebate does not cover

Here is the trap that catches investors. The rebate does not apply to income taxed at special rates. It is not allowed against income such as capital gains taxed under Section 111A and Section 112A. Cleartax

Suppose Priya has ₹6 lakh of salary and ₹3 lakh of long-term [capital gains] from equity. Her total may look like it sits comfortably under the limit, but the rebate cannot be used against the capital-gains portion — that part is taxed at its own special rate regardless. People routinely forward “income up to ₹12 lakh is tax-free” without realising it means ordinary income, not capital gains, lottery winnings, or online gaming income. The tax department’s processing system has in the past computed tax incorrectly on 87A claims involving special-rate income, which has made this one of the more disputed areas for AY 2026-27. Kcshah

There is also marginal relief for income just over the new-regime threshold. If your income slightly exceeds ₹12 lakh, marginal relief ensures the extra tax payable is not more than the income exceeding ₹12 lakh. So someone at ₹12.1 lakh does not suddenly owe full slab tax on the whole amount — their tax is capped at roughly the ₹10,000 by which they crossed the line. This relief applies up to approximately ₹12.75 lakh and is calculated automatically by the portal, but it is worth verifying if you compute tax manually. CleartaxKcshah

How to check if you qualify for the rebate under 87A

A two-minute self-check saves a lot of forwarded-message anxiety. The infographic below maps the conditions in order.

The 87A myths people keep sharing

Most of the confusion around the rebate under 87A comes from half-true forwards. Here is where to stop trusting them.

“Everyone earning under ₹12 lakh pays zero tax.” Not quite — it is resident individuals, on ordinary income, under the new regime. An NRI does not get it. “My capital gains are covered too.” They are not; special-rate income is excluded. “I crossed ₹12 lakh by ₹20,000, so I owe full tax now.” No — marginal relief caps your extra tax near the amount you crossed by. “It applies the same in both regimes.” It does not; the old-regime limit is ₹5 lakh, not ₹12 lakh. Treat any forwarded tax tip as a starting point to verify, never a conclusion.

Documents and checks before you rely on it

📋 Keep these in view before assuming the rebate applies:

- Your residential status for the year (resident versus NRI)

- Your total taxable income after deductions, computed correctly

- A separate figure for any capital gains or special-rate income

- Your Form 16 and the standard deduction already applied to salary

- The regime you are filing under, since the limit differs

- The tax computation shown on the income tax portal before you submit

Final takeaway

The rebate under 87A is real and powerful, but it is not the blanket “no tax up to ₹12 lakh” that gets forwarded around. It is for resident individuals, on ordinary income, with sharply different limits under the two regimes, and it simply does not touch capital gains and other special-rate income. If your income is ordinary salary and interest and you are within the limit, you genuinely pay nothing. If it is not, check carefully before assuming the same — that gap between the headline and the rule is exactly where filing mistakes happen.

Section 87A confusion, or unsure whether the rebate applies once you factor in capital gains or your residential status? eTaxMate can help you review your income, work out whether the rebate applies to you, and handle your filing correctly.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. Can NRIs claim the rebate under 87A?

No. The Section 87A rebate is available only to resident individuals. Non-residents cannot claim it, regardless of how low their Indian taxable income is. This is one of the most commonly missed conditions, because forwarded messages about “zero tax up to ₹12 lakh” almost never mention that residency is a strict requirement for the rebate.

2. How much is the 87A rebate for AY 2026-27?

It depends on your regime. Under the new tax regime, the rebate is up to ₹60,000, making taxable income up to ₹12 lakh effectively tax-free. Under the old tax regime, it remains ₹12,500, covering taxable income up to ₹5 lakh. The two limits are very different, so knowing which regime you are in matters.

3. Does the 87A rebate apply to capital gains?

No. The rebate does not apply to income taxed at special rates, which includes capital gains under Sections 111A and 112A, as well as lottery and online gaming winnings. So if your income mixes ordinary salary with capital gains, the gains are taxed at their own rate and the rebate cannot wipe them out, even if your total looks within the limit.

4. What happens if my income is just over ₹12 lakh?

Marginal relief protects you. If your taxable income slightly exceeds ₹12 lakh under the new regime, your extra tax is capped at roughly the amount by which you crossed the threshold, rather than full slab tax on the whole income. This relief applies up to around ₹12.75 lakh and is usually calculated automatically by the income tax portal.

5. Is salary up to ₹12.75 lakh really tax-free?

For a salaried person under the new regime, yes — but through two steps, not one. The ₹75,000 standard deduction first reduces salary, bringing taxable income to ₹12 lakh or below, and the 87A rebate then removes the remaining tax. So the ₹12.75 lakh figure works specifically for salary income, combining the standard deduction with the rebate.

6. Do senior citizens get the rebate under 87A?

Yes, provided they are resident individuals and within the income limits. Resident senior citizens and super-senior citizens qualify on the same conditions as other residents. The rebate is tied to being a resident individual within the threshold, not to age, so seniors are neither given a special higher rebate nor excluded from the normal one.