Your savings account earns interest every year. That interest is taxable — but the Income Tax Act 1961 gives you a deduction against it, depending on how old you are. Section 80TTA vs 80TTB both reduce your taxable interest income, but they cover different people, different deposit types, and different limits. Many taxpayers claim the wrong one, or miss the deduction entirely. This post settles which section applies to you and what you can actually deduct.

Quick answer

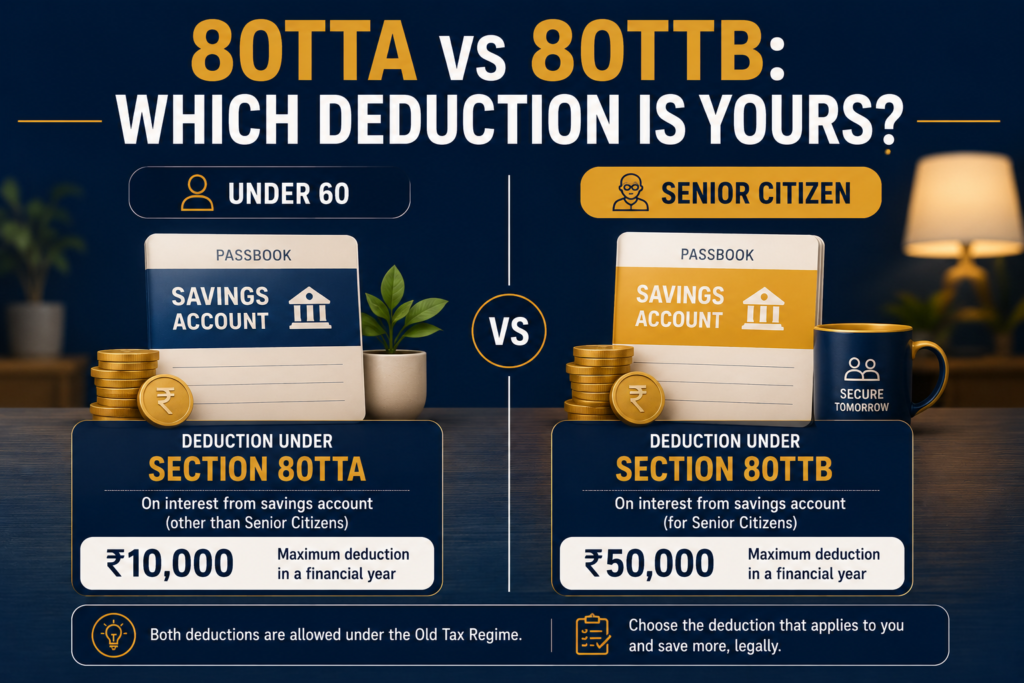

If you are below 60, Section 80TTA gives you a deduction of up to ₹10,000 on interest earned from savings accounts only. If you are 60 or above (a senior citizen), Section 80TTB gives you a deduction of up to ₹50,000 on interest from savings accounts, fixed deposits, and recurring deposits. The two sections are mutually exclusive — you claim one or the other, never both. Neither deduction is available if you opt for the new tax regime.

Before acting, check:

- Are you below 60, between 60 and 80, or 80 and above? Your age bucket determines which section applies.

- Is your interest income from a savings account, or also from fixed deposits and recurring deposits? The answer affects which section gives you relief.

- Are you filing under the old tax regime? Both deductions are unavailable under the new regime.

What Section 80TTA and 80TTB actually do

Both sections reduce your taxable income by the amount of interest you earn from bank deposits — up to a ceiling. They do not give you a tax credit; they reduce the base on which tax is computed. If you are in the 20% bracket and claim ₹10,000 under 80TTA, your tax saving is ₹2,000 (plus cess). The deduction sits in Chapter VI-A of the Income Tax Act 1961.

Section 80TTB was introduced in the Finance Act 2018, recognising that senior citizens depend on FD interest as a primary post-retirement income. Section 80TTA had existed since AY 2013-14 for everyone else.

The one rule that decides which section applies to you

Your age on the last day of the financial year — that is, 31 March — determines which section you use.

If you turn 60 on or before 31 March of the relevant financial year, you are a senior citizen for that year and you must use Section 80TTB. You cannot use Section 80TTA, even if you were below 60 for most of the year.

If you are below 60 on 31 March, you use Section 80TTA — and only savings account interest qualifies.

One point that surprises people: there is no further distinction between a senior citizen (60–79) and a super senior citizen (80 and above) for this deduction. Both use 80TTB with the same ₹50,000 ceiling. The 80-year age threshold matters for other provisions — such as the basic exemption limit — but not here.

What the 80TTA deduction covers — and what it does not

Section 80TTA applies to individuals and Hindu Undivided Families (HUFs) who are below 60. The deduction ceiling is ₹10,000 per year, and it applies only to interest from savings accounts — held with scheduled commercial banks, cooperative banks, or post offices.

Fixed deposits, recurring deposits, and other term deposits are explicitly excluded. If you earn ₹8,000 from your savings account and ₹40,000 from an FD, only the ₹8,000 qualifies — and since it is below ₹10,000, the full ₹8,000 is deductible. The ₹40,000 FD interest is taxable in full.

This is where many salaried taxpayers go wrong. The ₹10,000 ceiling does not cover all bank interest. FD interest for those below 60 is fully taxable, and the bank deducts TDS at 10% once interest crosses ₹40,000 in a year.

What the 80TTB deduction covers — and why it is broader

Section 80TTB applies to resident senior citizens — individuals aged 60 or above. The deduction ceiling is ₹50,000 per year, and it covers interest from savings accounts, fixed deposits, and recurring deposits — held with banks, cooperative banks, or post offices.

The practical impact: a retired individual with ₹20 lakh in a bank FD at 7% earns ₹1,40,000 in annual interest. Under 80TTB, ₹50,000 is deductible, bringing taxable interest down to ₹90,000. Without 80TTB, the full ₹1,40,000 is taxable.

One restriction that trips up non-residents: Section 80TTB applies only to resident individuals. An NRI aged 60 or above cannot claim this deduction.

Old regime vs new regime: does either deduction survive?

Neither Section 80TTA nor Section 80TTB is available under the new tax regime under Section 115BAC of the Income Tax Act 1961.

If you have opted for the new regime — which is now the default for individuals unless you actively opt out — your savings account interest and FD interest are fully taxable. You cannot claim either deduction.

This matters most for senior citizens. One earning ₹50,000 or more in FD interest annually gives up a meaningful deduction by staying in the new regime. Whether the new regime’s lower slab rates compensate depends on total income and other deductions. This deduction is available only if you opt for the old tax regime — if you are unsure which regime suits you, our comparison of the old tax regime and new tax regime walks through the full trade-off.

A quick comparison: 80TTA vs 80TTB side by side

Here is a visual summary of the two sections side by side — the fastest way to locate where you stand.

A few things worth noting from the comparison above. Senior citizens get five times the deduction ceiling not because the law treats FD interest differently in principle, but because Section 80TTB is explicitly broader in scope. Both deductions sit in Chapter VI-A of the Income Tax Act 1961, which means one rule governs both: unavailable if you choose the new regime.

Interest income from all sources must be reported under Schedule OS in your ITR — our post on filing ITR when you have income from other sources explains exactly how this flows through the return.

When you should not assume either deduction applies

There are several situations where taxpayers assume they qualify but do not.

You have chosen the new tax regime. This is the most common error. With the new regime now the default, many salaried taxpayers are in it without realising. Neither 80TTA nor 80TTB applies. Check your Form 16 or previous year’s ITR acknowledgement — if the regime is shown as 115BAC, you are in the new regime.

You are an NRI claiming 80TTB. Section 80TTB is restricted to resident senior citizens. If you are an NRI aged 60 or above, this deduction is not available. Your bank interest income may be subject to a flat TDS rate, and the Chapter VI-A mechanism works differently for non-residents.

You are claiming 80TTA on fixed deposit interest. A taxpayer below 60 cannot use 80TTA against FD interest. The section is explicit — only savings account interest qualifies. If your bank statement shows interest from both a savings account and a term deposit, only the savings account portion is eligible.

You are an HUF claiming 80TTB. Section 80TTB applies only to individuals, not to Hindu Undivided Families. An HUF can claim 80TTA on savings account interest, but 80TTB is unavailable regardless of the karta’s age.

You assume TDS means you are done. TDS deducted by the bank at 10% is an advance payment of tax, not a final settlement. You must still report the full interest income in your ITR and claim the deduction separately.

Documents to keep ready

- Annual interest statement from each bank (savings account, FD, and RD as applicable)

- Form 16A issued by the bank (the TDS certificate for interest income)

- Bank passbook or statement for the full financial year

- PAN linked to the bank account (mandatory — otherwise TDS is deducted at 20%)

- Form 26AS or Annual Information Statement (AIS) from the income tax e-filing portal — cross-check the interest figure against your bank statement before filing

Salaried readers who have already moved to the new tax regime will want to check which deductions still survive — our guide to salary deductions under the new regime covers this in detail.

Final takeaway

The 80TTA vs 80TTB question reduces to one fact: your age on 31 March of the financial year. Below 60, you get ₹10,000 off savings account interest under 80TTA. At 60 and above, you get ₹50,000 off all bank interest — savings, FD, and RD — under 80TTB. Both require the old tax regime. Neither applies to NRIs claiming 80TTB, and neither covers FD interest for those below 60. The deduction is modest, but the rule is clear — the only mistake is not claiming it at all.

Confused about which deduction applies to your interest income, or unsure whether your regime choice is costing you an 80TTA or 80TTB claim? eTaxMate can review your income, confirm the right deduction, and file your return correctly.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on this post.

Frequently Asked Questions

1. What is the difference between Section 80TTA and 80TTB?

Section 80TTA gives individuals below 60 a deduction of up to Rs 10,000 on savings account interest only. Section 80TTB gives senior citizens aged 60 and above a deduction of up to Rs 50,000 on interest from savings accounts, fixed deposits, and recurring deposits. The two sections are mutually exclusive — you use whichever applies to your age group, not both.

2. Can a senior citizen claim Section 80TTA instead of 80TTB?

No. Once you turn 60 on or before 31 March of a financial year, Section 80TTB replaces 80TTA for you. You cannot choose between the two. Since 80TTB has a higher ceiling of Rs 50,000 and covers FD interest as well, it is almost always the more beneficial section anyway.

3. Is FD interest covered under Section 80TTA?

No. Section 80TTA applies only to savings account interest — fixed deposits and recurring deposits are explicitly excluded. If you are below 60, FD interest is fully taxable with no deduction available. Only senior citizens (60 and above) can deduct FD interest, and they must use Section 80TTB, not 80TTA.

4. Are 80TTA and 80TTB available under the new tax regime?

Neither deduction is available if you opt for the new tax regime under Section 115BAC. Both sections sit in Chapter VI-A of the Income Tax Act 1961, which is entirely surrendered when you choose the new regime. If you have moved to the new regime, your bank interest income — savings, FD, or RD — is taxable in full.

5. Can an NRI claim Section 80TTB on fixed deposit interest?

No. Section 80TTB is available only to resident senior citizens. NRIs aged 60 or above cannot claim this deduction. NRI interest income is subject to a separate TDS regime, and Chapter VI-A deductions including 80TTB do not apply to it.

6. What happens if the bank deducts TDS on my interest — do I still need to claim the deduction in my ITR?

Yes. TDS deducted by the bank is an advance tax payment, not a final tax settlement. You must report the full interest income in your ITR under Schedule OS (Other Sources) and claim the 80TTA or 80TTB deduction separately in the deductions section. The TDS credit adjusts against your final tax liability — it does not replace the need to file and claim the deduction.