GST Input tax credit — ITC — is one of the most valuable features of GST. In theory, every rupee of GST your business pays on purchases can be offset against GST you owe on sales, so you pay tax only on the value you add. In practice, ITC is not automatic. Section 16 of the CGST Act 2017 sets out conditions that must all be satisfied before any credit can be claimed. Fail even one of them and the ITC is disallowed — and depending on when the failure is discovered, you may also owe interest on the incorrectly claimed amount.

Quick answer

Under Section 16(2) of the CGST Act, a registered business can claim ITC only if it holds a valid tax invoice, has received the goods or services, the ITC appears in its GSTR-2B, the buyer has filed its GSTR-3B, and the supplier has been paid within 180 days. ITC for FY 2025-26 must be claimed by 20 October 2026 — the due date of September 2026 GSTR-3B — or by the date of filing GSTR-9, whichever is earlier. After that, the credit is permanently lost.

Before reading further:

- Are you reconciling your purchase register against GSTR-2B every month before filing GSTR-3B?

- Have you checked whether any regular purchases fall under Section 17(5) blocked credits?

- Are any supplier invoices unpaid beyond 180 days? If so, ITC must be reversed.

How ITC works — and why it is not automatic

When a GST-registered business purchases goods or services for its business, the supplier charges GST. That paid GST is the potential ITC. Instead of remitting GST on the full sale price, the seller offsets the GST it collected on sales against the GST it paid on purchases.

Example: A software startup buys cloud services for ₹1 lakh plus ₹18,000 GST (18%). It charges a client ₹5 lakh plus ₹90,000 GST (18%). Without ITC, it remits ₹90,000. With ITC, it remits ₹90,000 minus ₹18,000 = ₹72,000. The ₹18,000 paid on cloud service is the ITC.

This makes GST a tax on value addition. But the credit is available only when all Section 16 conditions are met. The GSTR-2B statement is the primary gate: ITC not appearing in GSTR-2B cannot be claimed, regardless of how genuine the purchase is.

ITC is available only to GST-registered businesses — our post on the GST registration threshold explains when registration is mandatory and how to apply.

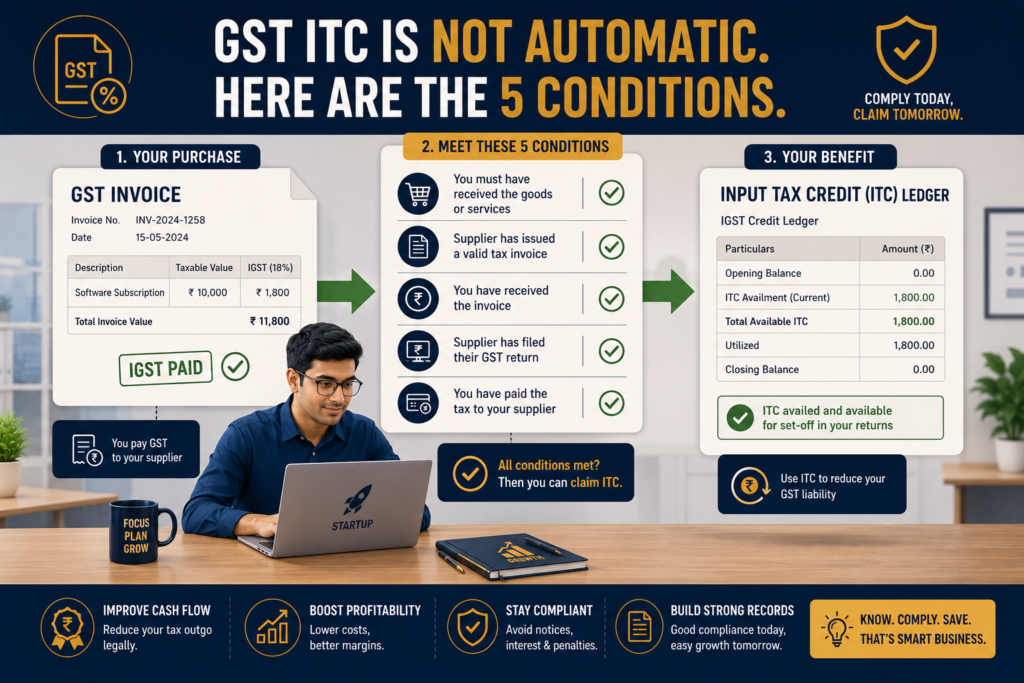

The five conditions under Section 16(2): all must be met

Section 16(2) of the CGST Act sets out conditions cumulatively — every condition must be satisfied for every invoice. One unsatisfied condition disallows the entire ITC on that invoice.

The five conditions: (1) hold a valid tax invoice or debit note; (2) goods or services received; (3) ITC appears in GSTR-2B; (4) buyer has filed GSTR-3B; (5) supplier paid within 180 days.

Condition 1: You must hold a valid tax invoice

ITC can only be claimed against a valid GST tax invoice, debit note, bill of entry (for imports), or ISD invoice. A receipt, payment confirmation, or pro forma invoice does not qualify.

The invoice must contain all mandatory fields: supplier’s GSTIN, invoice number and date, buyer’s name and GSTIN, HSN/SAC code, quantity, value, GST rate, and tax amount. An invoice missing any mandatory field is technically invalid for ITC purposes.

Common mistake: paying for a software subscription and receiving only a bank debit notification — not a GST tax invoice. For ITC purposes, only the invoice counts. Ensure every GST-registered vendor issues a proper tax invoice for every payment.

Condition 2: Goods or services must have been received

ITC arises only on purchases actually received — not on advance payments. For goods received in multiple lots, ITC on the full invoice can be claimed only after the last lot is received. For services, receipt is generally deemed to occur when the service is performed.

One nuance for bill-to-ship-to transactions: if Company A orders from a supplier but directs delivery to Company B’s premises, Company A can claim ITC as the buyer — provided the invoice is in Company A’s name — even though physical delivery went to Company B.

Condition 3: The ITC must appear in your GSTR-2B

Since the 2022 GST amendment, ITC is available only to the extent it appears in the buyer’s GSTR-2B — the auto-populated statement generated from the supplier’s GSTR-1 filing.

If the supplier has not filed their GSTR-1, the invoice does not appear in GSTR-2B and the ITC cannot be claimed — regardless of how genuine the purchase is. If the supplier files GSTR-1 but has not paid the tax, Rule 37A applies: ITC initially credited is automatically reversed in the next return period.

Every month, before filing GSTR-3B, reconcile your purchase register against GSTR-2B. Invoices in your register that do not appear in GSTR-2B are invoices for which ITC cannot yet be claimed. Follow up with the supplier to file their GSTR-1. Never claim ITC that has not appeared in GSTR-2B — it invites a demand with interest.

Exporters on the LUT route accumulate ITC on input purchases but cannot offset it against zero-rated output tax — our post on LUT under GST covers the cash refund process via Form RFD-01.

Condition 4: You must have filed your GSTR-3B

ITC for a period cannot be claimed unless the buyer has filed their own GSTR-3B for that period. Filing GSTR-3B late does not permanently lose the credit — but consistent late filing disrupts the ITC reconciliation cycle and may invite scrutiny.

Condition 5: Payment to the supplier within 180 days

Under Section 16(2)(b), if the buyer has not paid the supplier within 180 days from the invoice date, the ITC must be reversed — along with interest at 18% per annum from the date of original claim.

Once payment is made (even after 180 days), the reversed ITC can be re-claimed in the return period of actual payment. The reversal is temporary; the interest is real.

For startups with extended payment cycles — those paying vendors after 6 months or longer — track invoice dates and payment dates for all significant purchases to avoid unexpected ITC reversals.

The ITC time limit: the cutoff that makes unclaimed credit disappear

Under Section 16(4), ITC on any invoice of a financial year must be claimed by the earlier of:

- The due date of GSTR-3B for September of the following financial year, or

- The date of filing GSTR-9 for that financial year

For FY 2025-26: ITC on any invoice dated between 1 April 2025 and 31 March 2026 must be claimed by 20 October 2026 (September 2026 GSTR-3B due date) or by the date of GSTR-9 filing, whichever is earlier.

After that date, the ITC is permanently lost. No late claims, no extensions, no GSTR-9 amendments can restore it.

The risk: a startup that receives Q4 FY 2025-26 invoices (January–March 2026) and does not reconcile GSTR-2B until October 2026 may find that supplier non-compliance from those months has not been corrected — and the window has just closed.

Section 17(5): the blocked credits that never qualify

Even if all five Section 16(2) conditions are satisfied, certain purchases are permanently blocked under Section 17(5). These cannot be claimed regardless of invoice validity or GSTR-2B appearance.

Commonly blocked in most startups:

- Motor vehicles with seating up to 13 persons — cars, SUVs, two-wheelers — unless used for transporting goods or passengers as a business, or as a driving school vehicle.

- Food and beverages, outdoor catering — office lunches, team dinners, cafeteria supplies — unless the business itself is in the food supply business.

- Membership of clubs and fitness centres — corporate gym or club fees.

- Works contract services for immovable property — GST on civil construction, office renovation, or interior fit-out for own-use property. If the startup is a works contractor itself supplying WCS, eligible.

- Rent-a-cab — employee cab services are blocked unless the employer is legally obligated to provide transport.

- Life and health insurance — group health and life cover premiums are blocked unless the employer is an insurance company.

What is eligible (often confused with blocked):

- Office rent for a commercial premises — eligible.

- Laptops and computers for business use — eligible (not motor vehicles).

- Cloud software, SaaS subscriptions — eligible if for business use.

- Business travel — airline tickets, hotel bookings on official duty — eligible.

What Priya’s startup case shows you

Priya runs a SaaS startup in Hyderabad with a monthly GST output liability of ₹1.2 lakh. Monthly purchases: cloud infrastructure (₹40,000 GST), office rent (₹10,800 GST), software licences (₹9,000 GST), corporate cab arrangement for the team (₹4,500 GST), and a sprint-end team dinner (₹2,700 GST).

Running the conditions:

- Cloud infrastructure: Section 16(2) conditions met. ITC = ₹40,000. Eligible.

- Office rent: Section 16(2) met. ITC = ₹10,800. Eligible — commercial rent is not blocked.

- Software licences: Section 16(2) met. ITC = ₹9,000. Eligible.

- Corporate cab: Section 16(2) may be met, but Section 17(5) blocks rent-a-cab unless Priya is legally obligated to provide transport. Blocked. ITC = ₹0.

- Team dinner: Section 17(5) blocks food and beverages. Blocked. ITC = ₹0.

Net eligible ITC: ₹59,800. GSTR-3B cash outgo: ₹1,20,000 − ₹59,800 = ₹60,200.

Had Priya incorrectly claimed the cab and catering ITC, she would have claimed ₹7,200 of blocked credit — generating a demand plus interest when the department identified the reversal.

Freelancers who pay RCM on imported services — such as Adobe, Zoom, or Upwork fees — can claim that RCM payment back as ITC in the same return period; our post on GST for freelancers explains how the RCM-ITC cycle works.

ITC conditions at a glance

Here is a quick-reference infographic covering the five Section 16(2) conditions and the key blocked categories.

When ITC must be reversed

Supplier non-payment (Rule 37A): If a supplier files GSTR-3B but does not pay the tax, the buyer’s ITC is automatically reversed in the following month’s GSTR-3B. The buyer must recover the amount from the supplier or pay it as cash.

Non-payment within 180 days (Section 16(2)(b)): As discussed — ITC reversed, re-claimable on actual payment, 18% interest on the reversal period.

Mixed use (Rule 42/43): If goods or services are used partly for taxable and partly for exempt supplies, ITC must be proportionately reversed. A startup with some exempt and some taxable revenue must track the proportion of inputs used for each.

Capital goods and depreciation: ITC claimed on a capital good (e.g., a server with ₹36,000 GST) cannot be combined with income tax depreciation on the GST component. One or the other — not both.

Final takeaway

GST input tax credit is only as clean as the conditions that support it. All five Section 16(2) conditions must be satisfied simultaneously — and even then, Section 17(5) may block the credit permanently. The GSTR-2B gate catches most startups off guard: a genuine purchase from a genuine supplier is still ineligible for ITC if the supplier has not filed their GSTR-1. Monthly reconciliation of the purchase register against GSTR-2B, followed by supplier follow-up for missing entries, is the core of ITC hygiene. And 20 October 2026 is absolute: ITC not claimed by then for FY 2025-26 invoices is gone permanently.

Not sure which purchases qualify for ITC, or want to confirm your GSTR-2B reconciliation is catching every eligible credit? eTaxMate can review your ITC position, identify blocked credits being incorrectly claimed, and handle your monthly GSTR-3B filing.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. What are the conditions to claim GST input tax credit under Section 16?

Under Section 16(2) of the CGST Act, five conditions must all be satisfied simultaneously: (1) you hold a valid tax invoice or debit note, (2) goods or services have been actually received, (3) the ITC appears in your GSTR-2B (meaning your supplier has filed their GSTR-1), (4) you have filed your own GSTR-3B for that period, and (5) the supplier has been paid within 180 days of the invoice date. Failing any one of these disallows the ITC on that invoice.

2. What is the last date to claim ITC for FY 2025-26?

ITC for FY 2025-26 must be claimed by 20 October 2026 — the due date of the GSTR-3B return for September 2026 — or by the date of filing the annual return (GSTR-9) for FY 2025-26, whichever is earlier. After this deadline, ITC on any invoice dated between 1 April 2025 and 31 March 2026 is permanently lost. There is no extension or correction mechanism after the cutoff.

3. Can I claim ITC if the entry is not in my GSTR-2B?

No. Since the GST amendment effective from 2022, ITC is available only to the extent it appears in your GSTR-2B — the auto-populated statement generated from your supplier’s GSTR-1 filing. If your supplier has not filed their GSTR-1, the invoice will not appear in your GSTR-2B and you cannot claim the credit, regardless of how genuine the purchase is. You must follow up with the supplier to file their GSTR-1 before the ITC time limit expires.

4. Which purchases are blocked under Section 17(5) and cannot qualify for ITC?

Section 17(5) permanently blocks ITC on: motor vehicles with seating capacity up to 13 persons (unless used for goods transport or passenger transport as a business), food and beverages or outdoor catering, membership of clubs and fitness centres, construction of immovable property for own use, rent-a-cab services for employees (unless legally obligated), and employee health or life insurance premiums. These are blocked regardless of how genuine the purchase is or whether Section 16 conditions are met.

5. What happens if I claim ITC but do not pay the supplier within 180 days?

Under Section 16(2)(b), if you fail to pay the supplier within 180 days from the invoice date, the ITC you claimed must be reversed in your GSTR-3B, along with interest at 18% per annum from the date of original claim. Once you actually pay the supplier — even after 180 days — the reversed ITC can be re-claimed in the return period of payment. The reversal is temporary but the interest is a real cost.

6. Is office rent eligible for ITC under GST?

Yes. GST paid on commercial office rent is eligible for input tax credit — it is not blocked under Section 17(5). Office rent for a startup’s leased workspace, coworking space, or registered office is a legitimate business expense that qualifies for ITC, provided all Section 16(2) conditions are satisfied. This is a common misconception — rent is often confused with construction or immovable property, which is blocked.