If you have missed the ITR due date, the first question is not whether you will be penalised — it is how much the delay will actually cost you. Most people think the late filing fee 234F is the whole story. It is not. Section 234F is the flat fee the department charges for filing after the due date, but it rides alongside three interest provisions — 234A, 234B, and 234C — that can quietly inflate the total well past the flat fee. This post explains each one with worked numbers so you can see exactly where the money goes.

Quick answer

The late filing fee 234F is ₹5,000 if you file your ITR after the due date but before 31 December of the assessment year. It drops to ₹1,000 if your total income is up to ₹5 lakh. On top of this flat fee, interest under Sections 234A, 234B, and 234C may also apply if you have unpaid tax.

Before acting, check:

- Is your total income above or below the ₹5 lakh threshold?

- Do you actually have any tax still payable, or has TDS already covered it?

- Did you pay your advance tax instalments on time during the year?

What Section 234F actually charges

Section 234F of the Income Tax Act 1961 was introduced to push taxpayers towards filing within the due date. It applies to any person required to file a return under Section 139(1) who does so after the deadline.

The fee structure is straightforward:

- ₹5,000 if the return is filed after the due date.

- ₹1,000 if total income does not exceed ₹5 lakh.

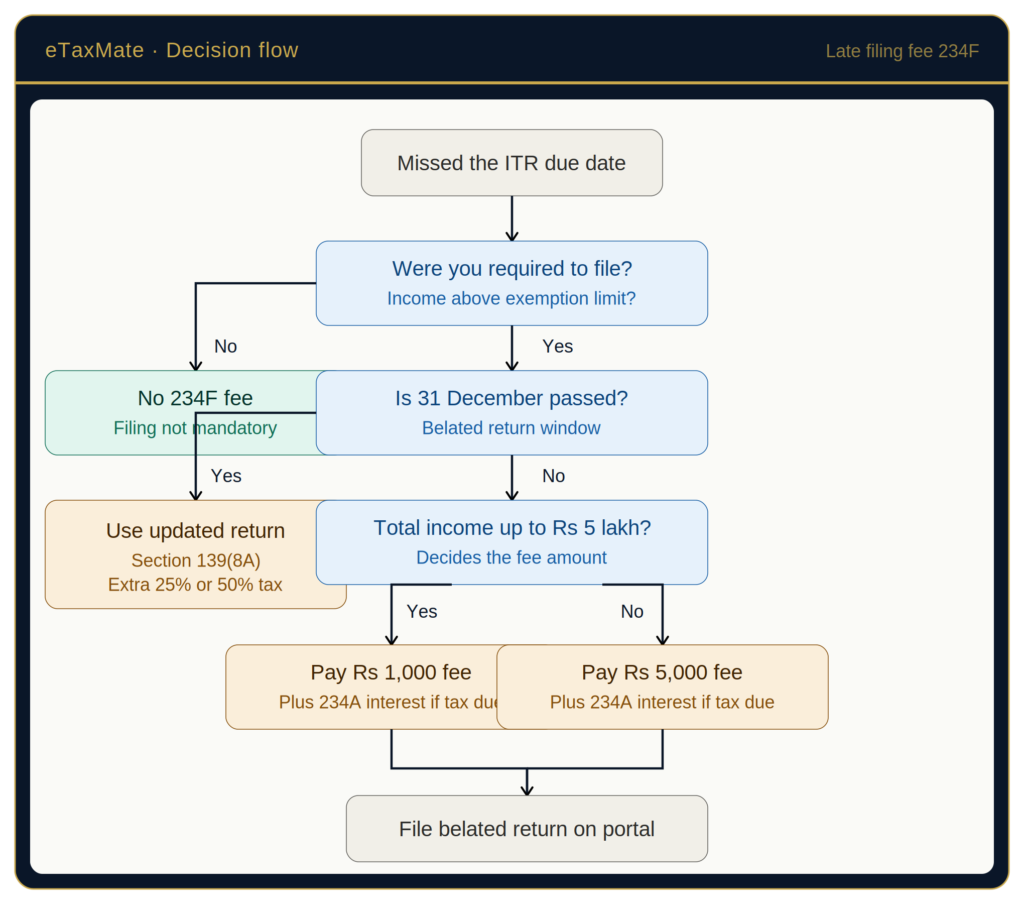

This is a flat fee, not a percentage. It does not scale with how late you are. Filing on 1 August costs the same as filing on 15 December, as long as both are before 31 December of the assessment year. After 31 December, the belated return window under Section 139(4) also closes for most cases, leaving only an updated return under Section 139(8A) — which carries its own additional tax cost and is a separate route.

For salaried individuals whose tax is fully covered by TDS, the 234F fee is often the only direct cost of late filing. But if any shortfall exists, Section 234A interest begins the day after the due date.

Who is exempt from the late filing fee 234F

Section 234F does not apply if you were not required to file a return in the first place. Filing is mandatory under Section 139(1) only when your gross total income exceeds the basic exemption limit before claiming most deductions, or when you meet one of the “seventh proviso” triggers — depositing more than ₹1 crore in current accounts during the year, spending more than ₹2 lakh on foreign travel, paying more than ₹1 lakh in electricity bills, or holding foreign assets. Companies, firms, and LLPs are always required to file.

The basic exemption limit depends on your regime. Under the new tax regime — the default from AY 2024-25 onwards — it is ₹3 lakh. Under the old regime, it is ₹2.5 lakh for individuals below 60, ₹3 lakh for senior citizens, and ₹5 lakh for super senior citizens. Your regime choice directly determines whether you cross the threshold that makes filing mandatory, which in turn determines whether 234F can apply to you at all.

Section 234A interest — worked examples

Section 234A charges 1% per month or part of a month on unpaid tax, from the day after the due date until the date you actually file the return (assuming you pay the shortfall at the same time). “Part of a month” is the trap — one extra day into a new month counts as a full month.

Example 1: Salaried, small shortfall. Priya’s ITR due date was 31 July 2025. Her total tax liability is ₹85,000, TDS deducted is ₹80,000, so her shortfall is ₹5,000. She files on 10 October 2025.

- Months of delay: August, September, October (part month) = 3 months

- 234A interest = ₹5,000 × 1% × 3 = ₹150

- Plus 234F fee: ₹5,000 (her income is above ₹5 lakh)

- Total cost of delay: ₹5,150

Example 2: Consultant, larger shortfall. Rahul, a freelance designer, has a final tax liability of ₹2,40,000 for FY 2024-25. His TDS under Section 194J is ₹48,000. Advance tax paid during the year is ₹1,50,000. Shortfall at the time of filing is ₹42,000. His due date was 31 July 2025 and he files on 2 December 2025.

- Months of delay: August, September, October, November, December (part month) = 5 months

- 234A interest = ₹42,000 × 1% × 5 = ₹2,100

- Plus 234F fee: ₹5,000

- Just the 234F + 234A portion: ₹7,100 (and 234B and 234C still to come, below)

The lesson: even a two-day slip into a new month adds another 1%. Paying the shortfall through a self-assessment challan before month-end stops the 234A clock on that portion, even if the return is filed a few days later.

Section 234B interest — worked examples

Section 234B kicks in when your advance tax paid during the year is less than 90% of your assessed tax liability. It is charged at 1% per month on the shortfall, from 1 April of the assessment year until the date of payment. This usually affects freelancers, consultants, business owners, and anyone with large non-salary income where TDS alone does not cover the liability.

Example: Rahul (continued from above). His assessed tax is ₹2,40,000. TDS is ₹48,000. Advance tax paid is ₹1,50,000. Total tax paid before year-end = ₹1,98,000.

- 90% of ₹2,40,000 = ₹2,16,000

- Since ₹1,98,000 is less than ₹2,16,000, 234B applies

- Shortfall for 234B = ₹2,40,000 − ₹1,98,000 = ₹42,000

- He files and pays on 2 December 2025

- Months from 1 April 2025 to 2 December 2025 (part month counted) = 9 months

- 234B interest = ₹42,000 × 1% × 9 = ₹3,780

Note that 234B runs from 1 April of the assessment year even if your due date is 31 July. The clock does not wait for the filing deadline.

Section 234C interest — worked examples

Section 234C penalises deferment of advance tax within the year. Advance tax is payable in four instalments, and each instalment has its own minimum cumulative percentage of the final liability that should have been paid by that date.

For individuals, the instalment schedule is:

- 15 June: 15% of tax liability

- 15 September: 45% of tax liability

- 15 December: 75% of tax liability

- 15 March: 100% of tax liability

If you fall short at any instalment, 234C charges 1% per month for three months on the shortfall at that instalment (1% for one month on the 15 March shortfall, since the year ends immediately after).

Example: Rahul’s instalment-wise check. His final tax liability is ₹2,40,000. His advance tax payments during the year were: ₹20,000 by 15 June, ₹80,000 cumulative by 15 September, ₹1,20,000 cumulative by 15 December, ₹1,50,000 cumulative by 15 March. His TDS of ₹48,000 is deemed spread across the year, so advance tax required excludes TDS: ₹2,40,000 − ₹48,000 = ₹1,92,000 is the base for advance tax obligations.

- 15 June: Required 15% of ₹1,92,000 = ₹28,800. Paid ₹20,000. Shortfall ₹8,800. Interest = ₹8,800 × 1% × 3 = ₹264.

- 15 September: Required 45% of ₹1,92,000 = ₹86,400. Paid ₹80,000. Shortfall ₹6,400. Interest = ₹6,400 × 1% × 3 = ₹192.

- 15 December: Required 75% of ₹1,92,000 = ₹1,44,000. Paid ₹1,20,000. Shortfall ₹24,000. Interest = ₹24,000 × 1% × 3 = ₹720.

- 15 March: Required 100% of ₹1,92,000 = ₹1,92,000. Paid ₹1,50,000. Shortfall ₹42,000. Interest = ₹42,000 × 1% × 1 = ₹420.

Total 234C interest = ₹264 + ₹192 + ₹720 + ₹420 = ₹1,596.

There is a small relief provision: if the shortfall at the 15 June or 15 September instalment is because of capital gains or lottery/speculative income that arose after that date, 234C does not apply to that portion — provided the tax on such income is paid in the remaining instalments.

How 234F and interest stack together

Taking Rahul’s case end-to-end, his total cost of late filing is:

- Late filing fee 234F: ₹5,000

- 234A interest: ₹2,100

- 234B interest: ₹3,780

- 234C interest: ₹1,596

- Total: ₹12,476 on top of the ₹42,000 tax shortfall itself

Against an original shortfall of ₹42,000, the additional cost is nearly 30%. This is why the advice “just pay the shortfall first, then file” matters so much — every month of delay compounds across multiple sections.

For a pure salaried taxpayer like Priya, only 234F and a small 234A apply, because TDS covered most of her liability and no advance tax was due. That is the best-case late-filing scenario: around ₹5,150. The worst-case scenario is a high-income consultant who deferred advance tax and filed months late — the stacking can easily exceed 40% of the shortfall.

Want an automated tool to calculate the above calculation. We have dedicated Late fees calculator, free to use. Go and check out!

What to do if you have missed the ITR due date

- Check whether the belated return window is still open. For most taxpayers, this runs from the day after the due date to 31 December of the assessment year.

- Compute your total tax liability, including TDS already deducted.

- If tax is still payable, pay it first through a self-assessment challan on the Income Tax e-filing portal, so 234A interest stops accruing from the date of payment.

- Prepare and file the belated return, selecting “return filed under Section 139(4)” in the ITR utility.

- The 234F fee is auto-populated by the utility based on your total income.

- If 31 December has already passed, switch to an updated return under Section 139(8A), which carries additional tax of 25% or 50% over the normal liability depending on how late you file.

When filing a belated return is the wrong call

Filing late is usually better than not filing at all, but there are situations where the calculation changes.

If you have capital losses or business losses that you wanted to carry forward to future years, a belated return disallows the carry-forward of most loss categories. Only loss from house property can still be carried forward in a belated return. Speculative business losses, capital losses, and other business losses are lost permanently if the return is not filed by the original due date under Section 139(1). For a trader who booked ₹3 lakh in short-term capital losses hoping to set them off against future gains, filing late turns that tax shield to zero.

If you are near the basic exemption limit and have no tax payable, no refund to claim, and no mandatory filing trigger, there is no penalty for not filing at all. Filing a belated return voluntarily in this situation invites the 234F fee for no benefit.

If you are choosing between the old and new regimes, a belated return locks you into the default regime — usually the new regime — and you cannot opt out through Form 10-IEA after the due date.

Checklist before you file a belated return

- PAN and Aadhaar, linked and active

- Form 16 from your employer, or income summary if self-employed

- Form 26AS and AIS downloaded from the Income Tax e-filing portal

- Bank statements for interest income and other receipts

- TDS certificates from non-salary deductors (Form 16A)

- Advance tax challans and self-assessment challan if already paid

- Bank account details pre-validated for refund, if any

- A clear note on your regime choice — knowing the belated return may lock you into the default

Final takeaway

The late filing fee 234F looks simple on paper — ₹5,000 or ₹1,000 — but it is rarely the whole cost. If you owe tax, Section 234A interest starts ticking from the day after the due date. If you under-paid advance tax, 234B and 234C pile on, with 234B running from 1 April of the assessment year. On a ₹42,000 shortfall, the extra cost of filing four months late can cross ₹12,000 before you even count the tax itself. The practical priority is always the same: pay the shortfall first through a self-assessment challan, then file — in that order, and before 31 December.

Missed the ITR due date or unsure how much 234F plus 234A, 234B, and 234C will actually cost you? eTaxMate can help you compute what you owe, pay it in the right order, and file the belated return before the window closes.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

What is the late filing fee under Section 234F for AY 2025-26?

The late filing fee 234F is ₹5,000 if you file your ITR after the due date but before 31 December of the assessment year. It is reduced to ₹1,000 if your total income does not exceed ₹5 lakh. The fee is flat — it does not increase with how late you file within that window.

How is Section 234A interest calculated with an example?

Section 234A charges 1% per month or part of a month on unpaid tax, from the day after the due date until you file. If Priya owes ₹5,000 after TDS and files on 10 October when the due date was 31 July, the delay spans August, September, and part of October — three months. Her 234A interest is ₹5,000 × 1% × 3 = ₹150.

What is the difference between Section 234B and Section 234C interest?

Both relate to advance tax, but they measure different things. 234B applies if your total advance tax for the year is less than 90% of the final liability, and runs from 1 April of the assessment year until payment. 234C applies instalment-wise — if you miss the 15 June, 15 September, 15 December, or 15 March thresholds, interest is charged on each shortfall separately.

Can I still carry forward my losses if I file a belated return?

Mostly no. Loss from house property can still be carried forward in a belated return. But capital losses, business losses, and speculative losses are permanently disallowed from carry-forward if you miss the original due date under Section 139(1). For anyone with trading losses or business losses, this is often a much bigger cost than the 234F fee itself.

Do I have to pay 234F if my income is below the basic exemption limit?

No. Section 234F applies only if you were required to file a return under Section 139(1). If your gross total income is below the basic exemption limit and none of the mandatory filing triggers apply — large current account deposits, foreign travel spending above ₹2 lakh, electricity bills above ₹1 lakh, or foreign assets — you are not liable for the late filing fee even if you file voluntarily.

What happens if I miss even the 31 December belated return deadline?

The belated return window under Section 139(4) closes on 31 December of the assessment year. After that, most taxpayers can only file an updated return under Section 139(8A), which carries additional tax of 25% over the normal liability if filed within 12 months, or 50% if filed within 24 months. It is significantly more expensive than a belated return.