When an income tax notice arrives — or when a CA conducts the annual audit — the first question is: where are the records? A startup that has filed every ITR and GST return on time but kept no supporting documents is still exposed. Section 44AA of the Income Tax Act 1961 makes book-keeping a legal obligation for businesses above prescribed thresholds. Missing records attract a ₹25,000 penalty under Section 271A — but the real risk is larger: the assessing officer can then estimate income on assumptions, with no documentation to rebut. So, what are the records to keep for income tax is the key area of discussion.

Quick answer

Under Section 44AA, businesses must maintain prescribed books when income exceeds ₹1.2 lakh or turnover exceeds ₹10 lakh in any of the three preceding years. Records must be kept for 6 years from the end of the relevant assessment year. Failure attracts ₹25,000 penalty under Section 271A.

Before reading:

- Does your business meet the Section 44AA threshold? The obligation is legal, not optional.

- Are records maintained at the principal place of business?

- If turnover crosses ₹1 crore, is a CA engaged for the Section 44AB tax audit, which relies on these same records?

Why record-keeping is a legal obligation, not just good practice

Record-keeping is not about neatness — it is about legal protection. Section 44AA, read with Rule 6F of the Income Tax Rules, specifies the books that must be maintained. The provision exists because the income tax system operates on self-assessment: you declare your income, the department trusts the declaration, and reserves the right to verify it. Records are the verification material.

The income tax department’s AIS already holds transaction data from your bank, GST filings, and TDS returns — our post on high-value transactions and income tax notices explains how mismatches between this data and your ITR trigger scrutiny, and why accurate records are your first line of defence.

Without records: the assessing officer can estimate income using comparable cases or circumstantial evidence — almost always unfavourable. And deductions claimed in the ITR can be disallowed for lack of supporting vouchers. Additions to income plus disallowed deductions combine into a tax demand far larger than the original liability.

Who must maintain books of accounts under Section 44AA

Section 44AA creates two categories.

Specified professionals (Section 44AA(1)): Doctors, lawyers, architects, chartered accountants, engineers, interior decorators, film artists, and other notified professionals must maintain prescribed books if gross receipts exceeded ₹1.5 lakh in any of the three preceding years — or, for a new profession, if gross receipts are expected to exceed that limit.

All other businesses (Section 44AA(2)): Any taxpayer carrying on a business must maintain books if income from business exceeded ₹1.2 lakh, or if turnover exceeded ₹10 lakh, in any of the three preceding years. For a newly set-up business, current-year expected figures determine the obligation.

Important exception: businesses on the Section 44AD presumptive scheme are not required to maintain prescribed books — unless they declare income below the presumptive rate, which triggers the obligation along with a mandatory tax audit under Section 44AB.

Maintaining records is a prerequisite for almost every other compliance obligation — our small business tax compliance checklist covers the full picture of filings, deadlines, and obligations that these records are needed to support.

How long must records be kept?

Records must be kept for 6 years after the end of the relevant assessment year. For FY 2025-26 (AY 2026-27), that means retention until 31 March 2033. If a case is reopened for reassessment under Section 148, records must be retained until the completion of that reassessment — which can extend the period further.

The practical implication: a notice for AY 2026-27 can legitimately arrive as late as 2031 or 2032 under the reopening provisions of Section 147/148. If records for FY 2025-26 are discarded before 31 March 2033, there is no defence. Keep a folder — physical or digital — labelled by financial year and retain it for the full six-year period.

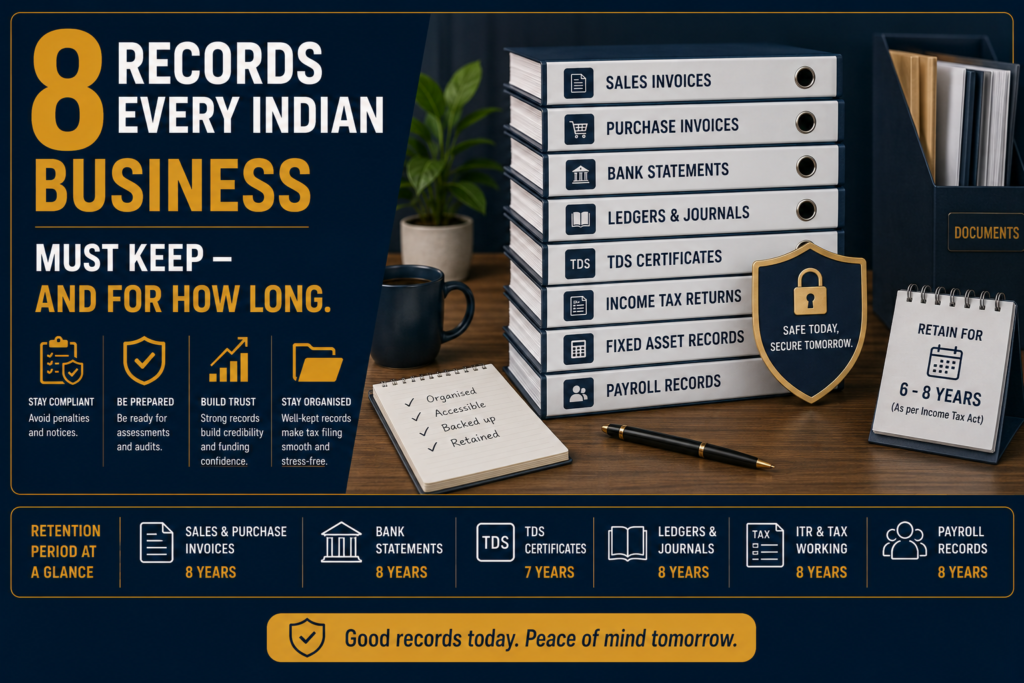

The 8 records every small business must maintain

Record 1: Sales invoices and purchase invoices

Every invoice issued to a customer (sales invoice) and every invoice received from a vendor (purchase invoice) must be maintained. For GST-registered businesses, invoices must carry mandatory fields: GSTIN, invoice number, date, HSN/SAC code, value, tax rate, and tax amount. For income tax, invoices are the primary evidence of both revenue and deductible expenses.

Rule 6F requires that for expenses above ₹25,000 (other than through banking channels), supporting vouchers must be retained.

Consider Vikram, who runs a small IT services firm. He pays ₹80,000 to a freelance developer in cash — not unusual in early-stage startups. Without a signed invoice or acknowledgement, that payment is vulnerable to disallowance at assessment. The deduction exists only as long as the invoice does.

If turnover crosses ₹1 crore, the same books satisfy Section 44AA and form the foundation of the Section 44AB tax audit — our post on tax audit applicability explains when the audit becomes mandatory and what the CA needs to certify.

Record 2: Cash book

The cash book is a daily record of all cash receipts, cash payments, and the closing cash balance. It is one of the prescribed books under Rule 6F and must be updated daily, not reconstructed at year-end.

For most businesses, the cash book and bank statement together tell the complete story of money flow. An assessing officer checking for suppressed income starts here: do the cash receipts in the cash book match the sales invoices? Are there unexplained credits? Unexplained cash receipts invite addition to income.

For fully digital businesses, most transactions flow through bank accounts. But any cash transaction — petty cash, stationery, taxi fares — must still appear in the cash book.

Record 3: Ledger

The ledger is the organised summary of every account: debtors, creditors, income, expenses, assets, and liabilities. Every invoice and cash entry posts to a ledger account. The trial balance — which the CA uses to prepare financial statements — is derived from the ledger.

The ledger is where individual transactions accumulate into the year’s figures. If a customer owes ₹4 lakh at year-end, their debtor account shows every invoice issued and every payment received. That is the evidence when the assessing officer asks how the outstanding balance was calculated.

Most accounting software (Tally, Zoho Books, QuickBooks) maintains the ledger automatically from invoices and journal entries.

Record 4: Bank statements

All business bank account statements for the full financial year must be retained. The bank statement is both an independent record and a reconciliation tool — it verifies that cash book and ledger entries match actual bank movements.

At year-end, the bank statement and cash book closing balance must reconcile. Any difference must be explained in a bank reconciliation statement (BRS). A BRS that cannot be prepared because statements are missing is itself a compliance red flag during audit.

For businesses with multiple accounts — operations, GST refunds, payroll — every account’s statement must be retained separately.

Record 5: TDS certificates and AIS

Two sources cover TDS:

TDS received: Every time a customer deducts TDS on a payment to your business, they must issue Form 16A (non-salary) or Form 16 (salary). These are the documentary evidence for claiming TDS credit in your ITR.

TDS deducted: If your business deducts TDS when paying vendors, keep the deposited challans (Form ITNS 281), quarterly TDS return acknowledgements (Form 24Q or 26Q), and Form 16A issued to each vendor.

The Annual Information Statement (AIS) on the income tax e-filing portal aggregates all TDS and financial data the government holds against your PAN. Cross-check your AIS against your own records before filing ITR. Discrepancies in TDS credit amounts between AIS and Form 16A are common — and must be reconciled before filing.

Record 6: GST returns and supporting documents

For GST-registered businesses, maintain:

- Filed GSTR-1 and GSTR-3B returns: the official record of outward supplies and tax payments

- GSTR-2B statements: the auto-populated ITC record, critical for monthly reconciliation

- E-invoices: for businesses above ₹5 crore turnover, each e-invoice carries an IRN

- ITC reconciliation workings: the monthly comparison of purchase register against GSTR-2B

- GSTR-9 (annual return): reconciles all monthly filings for the year

Under GST law, all records must be kept for 72 months (6 years) from the due date of the annual return. For FY 2025-26, that means until 31 December 2032.

Record 7: Payroll and salary records

If the business employs anyone on salary, maintain:

- Salary register: month-wise gross salary, allowances, deductions (PF, ESI, TDS), and net pay per employee

- TDS on salary (Form 24Q): quarterly returns filed with the income tax department

- Form 16 issued to employees: the annual TDS certificate each employee uses for their ITR

- PF and ESI challans and ECR filings: proof of monthly contributions

- Appointment letters: evidence of agreed salary terms

For startups that pay co-founders through salary, the salary register and Form 24Q are equally important. Founders paying themselves unusually high or low salaries relative to company revenue invite scrutiny — consistent, documented salary records are protective.

Record 8: Fixed assets register and depreciation workings

A fixed assets register (FAR) lists every item of capital expenditure: laptops, servers, furniture, equipment, vehicles. For each asset, the register records the date of purchase, cost, depreciation rate applied (per the Income Tax Act), depreciation charged each year, and written-down value at year-end.

The depreciation charged in the FAR determines what appears as a deduction in the ITR. Without a maintained FAR, the CA cannot verify the depreciation workings and the assessing officer can disallow the deduction.

For startups, the FAR is often neglected in early years. By Year 3, cumulative capital expenditure on computers and cloud infrastructure can be substantial — and an inconsistently maintained FAR creates audit complications. Start the register with the first asset purchased.

What happens if records are missing during assessment

If the department selects your case for scrutiny under Section 143(2), the assessing officer will request books and supporting documents. Missing records produce three outcomes:

- A best-judgement assessment under Section 144, estimating income — almost always resulting in a higher tax demand

- Specific deductions disallowed for lack of supporting vouchers

- A ₹25,000 penalty under Section 271A for failure to maintain books

All three can apply simultaneously. The combined tax demand, interest, and penalties far exceed the cost of proper record-keeping.

At a glance: the 8 records, their legal basis, and retention

Here is a quick-reference infographic covering the 8 records, the provision they satisfy, and how long to keep them.

Final takeaway

The 8 records in this post are not optional extras — they are a legal obligation for most businesses above modest turnover thresholds, and the practical minimum for defending any deduction or income figure at assessment. A business without invoices cannot prove its expenses. Without a bank reconciliation, it cannot explain its cash position. Without TDS certificates, it cannot claim the credit it is owed. Start these records at inception, maintain them consistently, and store them by financial year for the full six years.

Want to confirm whether your record-keeping meets Section 44AA requirements, or need a CA to review books before the audit? eTaxMate can assess your records, close any gaps, and ensure everything needed for ITR filing and audit is in order.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. What records must a small business keep for income tax in India?

Under Section 44AA of the Income Tax Act 1961, small businesses above prescribed thresholds must maintain: a cash book, ledger, sales and purchase invoices, bank statements, TDS certificates, GST returns and documents, payroll records, and a fixed assets register with depreciation workings. These records must be retained for 6 years from the end of the relevant assessment year. Failure to maintain them attracts a penalty of Rs 25,000 under Section 271A.

2. Who is required to maintain books of accounts under Section 44AA?

Businesses must maintain books if income from business exceeded Rs 1.2 lakh or turnover exceeded Rs 10 lakh in any of the three preceding financial years. Specified professionals (doctors, lawyers, architects, chartered accountants, engineers) must maintain books if gross receipts exceeded Rs 1.5 lakh in any of the three preceding years. Businesses on the Section 44AD presumptive scheme are exempt — unless they declare income below the prescribed rate, which then triggers the obligation.

3. How long must a small business keep income tax records in India?

Books of accounts and supporting documents must be retained for 6 years from the end of the relevant assessment year. For FY 2025-26 (AY 2026-27), that means until 31 March 2033. GST records have a slightly longer retention requirement — 72 months (6 years) from the due date of the annual return. If a reassessment is opened under Section 148, records must be kept until the reassessment is completed, which can extend the period further.

4. What happens if a business does not maintain proper books of accounts?

Three consequences can apply simultaneously. First, a penalty of Rs 25,000 under Section 271A for failure to maintain books. Second, the assessing officer can make a best-judgement assessment under Section 144, estimating income — almost always resulting in a higher tax demand. Third, deductions claimed in the ITR can be disallowed if no supporting vouchers exist. Missing records during a scrutiny assessment are one of the most avoidable causes of large tax demands on small businesses.

5. Do startups on the ITR-4 presumptive scheme need to keep books?

Generally, businesses using the Section 44AD presumptive scheme under ITR-4 are not required to maintain prescribed books of accounts. However, if they want to declare income below the prescribed rate (8% or 6%), they must maintain books and get a tax audit done under Section 44AB. Even for those exempt from mandatory book-keeping, it is advisable to maintain invoices, bank statements, and basic records — they are needed for GST compliance, TDS credit claims, and any future assessment or funding due diligence.

6. Are digital records accepted for income tax purposes?

Yes. The Income Tax Department accepts digital records — accounting software, cloud-based systems, spreadsheets, and scanned documents — provided they are complete, auditable, and can be produced on request. The requirement is that records must be accessible and verifiable, not that they be physical. For businesses with high transaction volumes, accounting software like Tally or Zoho Books is strongly recommended as it maintains an audit trail automatically and integrates with GST and TDS filing workflows.