You filed your income tax return, hit submit, and then realised you forgot to declare interest from a fixed deposit. Or you claimed a deduction under the wrong section. Or the bank account you mentioned for the refund was closed last year. This is one of the most common situations Indian taxpayers face after filing season ends, and the panic is almost always unnecessary. The Income Tax Act 1961 gives you a straightforward way to fix it through what is called a revised return under Section 139(5). This post explains when you can file one, what it can fix, and where the trap doors are.

Quick answer

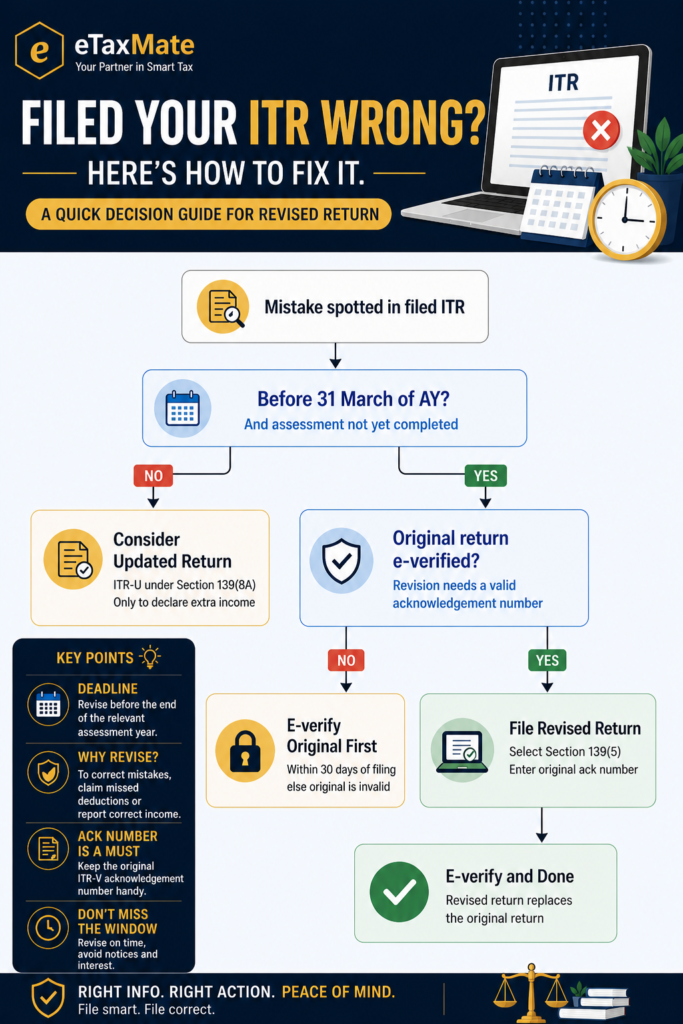

A revised return lets you replace your originally filed ITR with a corrected version, as long as you file it before 31 March of the relevant assessment year or before the assessment is completed, whichever is earlier. It is filed under Section 139(5), uses the same e-filing process as the original return, and there is no limit on how many times you can revise — but each revised return fully replaces the previous one.

Before filing a revised return, check:

- Are you within the deadline (31 March of the relevant assessment year)?

- Has your original return already been processed or assessed?

- Is a revised return the right tool, or do you need an updated return (ITR-U) instead?

What a revised return actually is

A revised return is not a “correction patch” added on top of your original ITR. It is a fresh, complete return that legally replaces the one you filed earlier. Once you file it, the revised version becomes your return of income for that year for all purposes — refunds, scrutiny, carry-forward of losses, everything.

Under Section 139(5) of the Income Tax Act 1961, any taxpayer who has filed a return — whether on time under Section 139(1) or belatedly under Section 139(4) — can revise it if they discover an omission or a wrong statement. The provision is deliberately broad. The law does not ask you to prove the mistake was innocent or to explain why you missed something the first time.

For example, suppose Priya, a salaried professional in Pune, filed her ITR-1 in July 2026 declaring only her salary income. In September, she gets her bank’s interest certificate and realises she forgot to add ₹38,000 of savings account and FD interest. She can simply log in to the e-filing portal, file a revised return adding the interest under “Income from Other Sources,” pay the small additional tax, and the matter is closed.

When you can file a revised return

The deadline is the earlier of these two events:

- 31 March of the assessment year in which the original return was filed. For income earned in financial year 2025-26 (assessment year 2026-27), the last date to revise is 31 March 2027.

- Completion of assessment by the income tax department. Once the assessing officer issues a final assessment order, the return cannot be revised.

This means if you filed your ITR in July 2026 and the department processes it under Section 143(1) and issues an intimation in October 2026, you can still revise — a Section 143(1) intimation is not a completed assessment. But if a regular assessment under Section 143(3) is concluded, the door closes.

There is no minimum waiting period and no maximum number of revisions. You can revise the same return five times if you keep finding new mistakes. However, each filing must be a complete return, not an incremental edit, and each one fully supersedes the last.

What kind of mistakes a revised return can fix

The scope is wide. Common situations where a revised return is the right answer:

- Missed income. Bank interest, dividend income, capital gains from a mutual fund redemption, rental income, freelance receipts that came in late.

- Wrong deduction claimed. You claimed Section 80C for a life insurance premium that was actually paid by your spouse, or claimed HRA without being eligible.

- Wrong tax regime selected. You picked the new regime by mistake when the old regime would have been better, and the deadline to switch has not closed.

- Bank account error. The account number for refund credit was wrong or the account is now closed.

- Wrong ITR form used. You filed ITR-1 but actually had capital gains, which requires ITR-2.

- Personal details errors. Name spelling, address, contact details that affect notices.

- Forgotten exempt income disclosure. Agricultural income, PPF interest — these are exempt but still need to be reported.

For example, Rahul, a Bengaluru-based software engineer, filed ITR-1 declaring only salary. He later remembered he had sold listed shares during the year and had short-term capital gains of ₹1.2 lakh. ITR-1 does not allow capital gains, so his original return is technically defective. The fix is to file a revised return using ITR-2, declaring both salary and capital gains.

Revised return vs updated return: the key difference

This is where most readers get confused. The Income Tax Act now offers two different repair tools, and they are not interchangeable.

A revised return under Section 139(5) is the standard correction tool. It is free to file (no extra tax beyond the regular tax on the corrected income), available until 31 March of the assessment year, and can move the return in any direction — increase income, decrease income, change refund, claim a missed deduction.

An updated return under Section 139(8A), also called ITR-U, is a separate facility introduced in 2022. It is available for up to 48 months from the end of the relevant assessment year (extended from the earlier 24-month window), but it comes with conditions. It can only be used to declare additional income, never to reduce income or claim a larger refund. It also requires payment of additional tax — 25% on top of the tax and interest if filed within 12 months of the assessment year end, 50% if filed in months 13 to 24, 60% in months 25 to 36, and 70% in months 37 to 48.

In short: if you are within the 31 March deadline and want to make any kind of correction, file a revised return. If that deadline has passed and you only need to declare income you missed, an updated return is your option.

How to file a revised return on the income tax portal

The process mirrors the original filing, with one key flag.

The actual steps on the e-filing portal:

- Log in at the Income Tax e-filing portal using your PAN and password.

- Go to e-File → Income Tax Returns → File Income Tax Return.

- Select the relevant assessment year and the appropriate ITR form (the same one you used originally, unless the mistake was the form itself).

- Choose Revised Return under Section 139(5) as the filing type.

- Enter the acknowledgement number and date of filing of your original return — these come from the ITR-V or your e-filing dashboard.

- Fill in the corrected return in full. This is a complete return, not an edit, so re-enter all data with the corrections applied.

- Compute tax. If the revision increases your liability, pay the additional tax along with applicable interest under Sections 234B and 234C — these are the advance tax shortfall and deferment interest provisions — before submission.

- Submit and e-verify within 30 days, otherwise the revised return is treated as never filed and the original stands.

When you should not rush to file a revised return

A revised return is a useful tool, but it is not always the right first move. Step back if:

- The “mistake” is actually a difference in interpretation flagged by the AIS or 26AS. Check the figures first. If your return is correct and the mismatch is a reporting error in the AIS, file feedback in the AIS portal rather than revising your return.

- You received a Section 143(1) intimation with a small adjustment. Sometimes the department’s own calculation correctly reconciles your return. Read the intimation carefully before assuming you need to revise.

- The error is purely clerical and does not affect tax. A mistyped pin code or a non-critical disclosure error may not be worth a full revised return — though most taxpayers prefer to revise for completeness.

- You are revising only to lower your declared income without solid documentation. Revisions that reduce income invite scrutiny. If you do not have proof for the change, the original figure is safer than a revised one you cannot defend.

- The original return itself was never e-verified. An unverified return is treated as invalid. There is nothing to revise — file a fresh original return instead, if the deadline allows.

Documents and details to keep ready

Before filing a revised return, gather:

- Acknowledgement number and date of filing of the original return

- Form 16, Form 16A, and any TDS certificates

- Updated bank interest certificates and dividend statements

- Latest AIS and Form 26AS download from the e-filing portal

- Capital gains statements from brokers and mutual funds

- Proofs for any deductions being added or modified

- Challan details for any additional tax already paid

- A clear note of exactly what is being corrected and why

Final takeaway

Filing the wrong ITR, missing a piece of income, or claiming a deduction incorrectly is not the disaster it feels like in the moment. As long as you act before 31 March of the assessment year and your return has not been formally assessed, a revised return under Section 139(5) lets you replace the original cleanly and at no extra cost. The real mistake is leaving the error untouched and waiting for a notice. Fix it early, fix it completely, and keep proof of what changed and why.

Spotted a mistake in your filed ITR or unsure whether to file a revised return or an updated return? eTaxMate can help you review your original filing, identify what needs correction, and file the right type of return on the portal.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. How many times can I file a revised return for the same year?

There is no limit under Section 139(5). You can revise the same return multiple times as long as each filing is before 31 March of the assessment year and the assessment has not been completed. Each revised return fully replaces the previous version, so the most recent valid filing is the one the department considers final.

2. Will filing a revised return trigger a tax notice?

A revised return by itself does not automatically invite scrutiny. The department recognises that taxpayers genuinely discover omissions or errors after filing. However, revisions that significantly reduce declared income or increase refunds without supporting documents do attract closer review. Filing a revised return that is well-documented and accurate is far safer than leaving an error in place.

3. Can I change my tax regime in a revised return?

For salaried taxpayers without business income, the regime can usually be re-selected in a revised return filed within the deadline. For taxpayers with business or professional income, the regime choice is more restricted because of the rules around Form 10-IEA. If you have business income and want to switch regimes through a revision, take professional advice before filing.

4. What if my original ITR was filed late under Section 139(4)?

A belated return filed under Section 139(4) can also be revised under Section 139(5), as long as the revision is filed before 31 March of the assessment year and before assessment is completed. The same deadline and process apply. The revised return then replaces the belated one for all purposes.

5. Is there any extra tax or penalty for filing a revised return?

No specific penalty applies for revising a return. If the revision increases your tax liability, you pay the differential tax along with interest under Sections 234B and 234C for any shortfall. There is no separate fee for the revision itself, which is what distinguishes it from an updated return under Section 139(8A) where additional tax of 25% to 70% is payable.

6. Can I file a revised return after receiving a Section 143(1) intimation?

Yes. A Section 143(1) intimation is a preliminary processing notice, not a completed assessment. As long as you are within the 31 March deadline of the assessment year, you can still file a revised return. However, if a regular assessment under Section 143(3) has been completed, the option to revise is closed and other remedies must be considered.