If you are an NRI, you have probably been asked to choose between an NRE, an NRO, and an FCNR account, and the bank likely explained the difference in two rushed sentences. The confusion around NRE NRO and FCNR account is one of the most common things NRIs get wrong, and it costs them — either in tax they did not need to pay, or in money they cannot freely move out of India. The three accounts look similar but are taxed and repatriated very differently. This post sorts them out in one clear view, so you know which account holds what, and what India can tax.

Quick answer

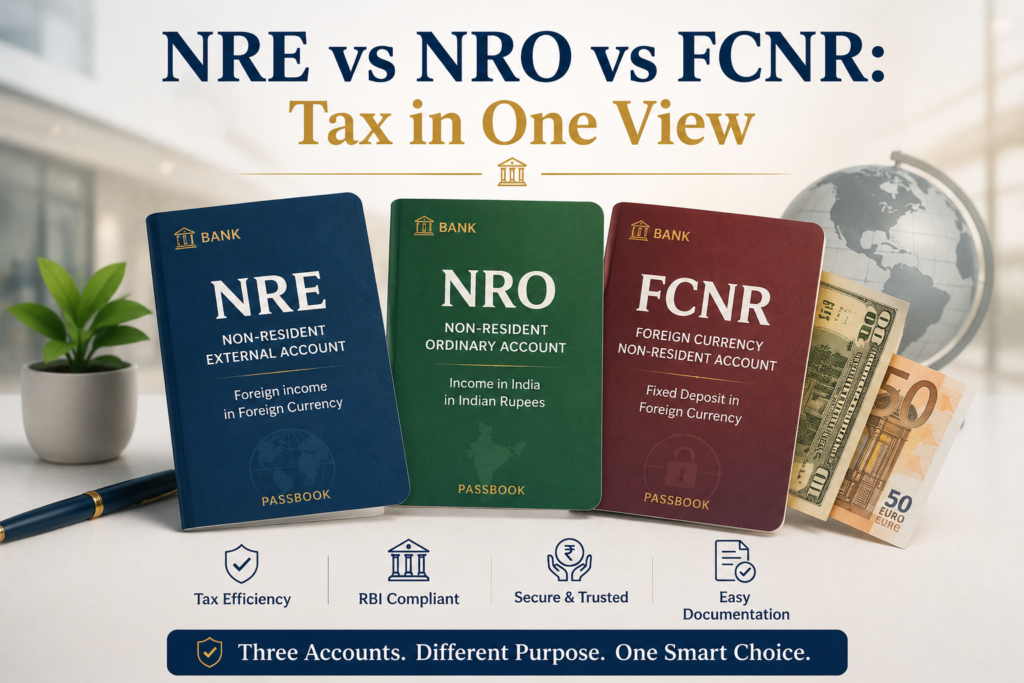

NRE and FCNR interest is generally tax-free in India; NRO interest is fully taxable and subject to TDS. All three serve different purposes: NRE for foreign earnings parked in rupees, FCNR for foreign earnings held in foreign currency, and NRO for income arising in India.

Before acting, check:

- Whether the money you are depositing is earned abroad or arises in India.

- Whether you still qualify as a person resident outside India under FEMA.

- How much you need to move out of India, and from which account.

What each account is for

The three accounts exist because an NRI has two kinds of money: income earned abroad, and income arising in India. The account type follows the source of the money.

An NRE (Non-Resident External) account holds foreign earnings converted into Indian rupees. You send money from abroad, it sits in rupees, and both the principal and the interest can be moved back out freely.

An FCNR (Foreign Currency Non-Resident) account also holds foreign earnings, but keeps them in the original foreign currency — dollars, pounds, dirhams — as a fixed deposit. This protects you from rupee exchange-rate movement.

An NRO (Non-Resident Ordinary) account holds income that arises in India: rent from an Indian flat, dividends from Indian shares, a pension, or money from selling Indian assets.

Consider Sanjay, an NRI in Dubai. His salary savings sent home go into his NRE account. The rent from his Mumbai apartment goes into his NRO account. If he wants to lock in dollars rather than rupees, he opens an FCNR deposit. Same person, three accounts, three different jobs.

NRE NRO FCNR tax treatment, account by account

This is where the accounts diverge sharply, and where most of the confusion lives.

NRE account

Interest earned on an NRE account is exempt from income tax in India, as long as you qualify as a person resident outside India under FEMA, the Foreign Exchange Management Act. There is no TDS on NRE interest while that condition holds. This is the main reason NRIs favour NRE accounts for parking foreign savings.

FCNR account

FCNR interest is treated the same way — exempt from Indian income tax while you remain a non-resident under FEMA. The added benefit is that the deposit stays in foreign currency, so you carry no rupee depreciation risk on the principal.

NRO account

NRO interest is fully taxable in India and subject to TDS (tax deducted at source). For NRIs, TDS on NRO interest is generally deducted at a higher rate than for residents. This is where a tax treaty can help: if India has a DTAA with your country of residence, you may be able to claim a lower rate — but only if you furnish the right documents. You can read more about claiming DTAA relief with a TRC and Form 10F, because without that paperwork the higher domestic deduction stands.

Take Priya, an NRI in the UK with a rented flat in Pune. The rent lands in her NRO account, and the bank deducts TDS on the interest that account earns. Her NRE savings, meanwhile, earn interest tax-free. Same person — but the money’s source decides the tax.

Repatriation: moving the money out

Tax is only half the picture. The other half is repatriation — your ability to send the money out of India.

NRE and FCNR funds are freely repatriable. Both principal and interest can be moved abroad without limit and without special permission, because the money originated abroad.

NRO funds are different. Repatriation from an NRO account is capped — currently up to USD 1 million per financial year — and requires documentation, typically including a chartered accountant’s certificate in Form 15CA/15CB confirming taxes are paid. The money arose in India, so moving it out is more controlled. For the full mechanics, see how repatriation and FEMA rules work.

Old Act, new Act, and the regime question

The exemption for NRE and FCNR interest, and the taxability of NRO interest, are rules of source and residential status, not deductions. So the choice between the old and new tax regime does not change whether NRE or FCNR interest is exempt or whether NRO interest is taxed. The regime affects only the rate applied to your taxable Indian income, which would include NRO interest.

On the law: the exemption for NRE and FCNR interest and the taxability of NRO interest exist under the Income Tax Act 1961 and continue in substance under the Income Tax Act 2025. The FEMA-linked condition for the NRE/FCNR exemption is unchanged in principle. The exact section numbering under the 2025 Act should be confirmed against the current bare Act rather than assumed.

A crucial point for anyone moving back to India: the NRE and FCNR exemption depends on your FEMA residential status, not your income tax status. When you return for good, your FEMA status can change, and the exemption can stop even before your income tax position fully shifts. This trips up returning NRIs constantly — see how RNOR status affects returning NRIs for how the transition actually works.

How to choose and use the right account

The rule of thumb is simple: match the account to the source of the money. Foreign earnings go to NRE (in rupees) or FCNR (in foreign currency); Indian income goes to NRO.

In practice: open an NRE account for routine foreign savings you may want to bring back, use FCNR when you want to avoid rupee risk on a fixed deposit, and route all India-source income through an NRO account, accepting that it will be taxed and that moving it out needs paperwork.

When these accounts will not work the way you expect

These accounts are well-designed, but a few assumptions catch NRIs out.

The NRE and FCNR tax exemption is not permanent. It rests on your being a non-resident under FEMA. Once you return to India for good and your FEMA status changes, the exemption can end, and continuing to treat that interest as tax-free is a mistake.

You cannot deposit Indian-source income into an NRE account. Rent, Indian dividends, or sale proceeds of Indian assets belong in an NRO account. Pushing them into an NRE account to chase the exemption is not permitted and can create FEMA problems.

Do not assume a treaty automatically lowers your NRO TDS. The lower rate applies only when you furnish a valid tax residency certificate and supporting documents; without them, the higher domestic rate is deducted.

Finally, the NRO repatriation cap and its documentation are real constraints. Plan large outward transfers in advance rather than assuming the money will move on demand.

Quick checklist for NRI account holders

📋 Keep these ready:

- Clarity on the source of each rupee — foreign earnings (NRE/FCNR) versus Indian income (NRO).

- Proof of your non-resident status under FEMA, supporting the NRE/FCNR exemption.

- A valid tax residency certificate and Form 10F if you want lower treaty TDS on NRO interest.

- Form 15CA/15CB and a CA certificate for repatriating funds from an NRO account.

- A record of your FCNR deposit currency and maturity, if avoiding rupee risk matters to you.

Final takeaway

The one idea to keep is that the source of the money decides everything. Foreign earnings sit in NRE or FCNR accounts, where interest is generally tax-free and the funds move out freely. India-source income sits in an NRO account, where interest is taxed, TDS applies, and repatriation is capped and paperwork-heavy. Match each rupee to the right account by where it came from, and remember that the NRE and FCNR exemption depends on your staying a non-resident under FEMA — a status that changes the day you move back for good.

NRE, NRO and FCNR tax confusion, or need expert help structuring your accounts and claiming the right treaty rate on NRO interest? eTaxMate can help you review your situation, identify what applies to you, and handle filing or compliance correctly.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. Is interest on an NRE account taxable in India?

No, NRE account interest is generally exempt from income tax in India, and no TDS is deducted, as long as you qualify as a person resident outside India under FEMA. This exemption is a key reason NRIs use NRE accounts for foreign savings. It ends if your FEMA residential status changes, such as when you return to India permanently.

2. Why is TDS deducted on my NRO account interest?

NRO account interest is fully taxable in India because the account holds India-source income, so the bank deducts tax at source. For NRIs, this is generally at a higher rate than for residents. If India has a tax treaty with your country, you may claim a lower rate, but only by furnishing a valid tax residency certificate and Form 10F.

3. Can I freely move money out of an NRE versus an NRO account?

NRE and FCNR funds, both principal and interest, are freely repatriable abroad without limit, because the money originated overseas. NRO funds are different: repatriation is capped, currently up to USD 1 million per financial year, and requires documentation including a chartered accountant’s certificate in Form 15CA/15CB confirming taxes are paid.

4. What is the difference between an NRE and an FCNR account?

Both hold foreign earnings and both offer tax-free interest while you are a non-resident under FEMA. The difference is currency: an NRE account converts your money into Indian rupees, exposing you to rupee exchange-rate movement, while an FCNR account keeps the deposit in the original foreign currency, protecting the principal from rupee depreciation.

5. What happens to my NRE account tax exemption when I return to India?

The NRE and FCNR interest exemption depends on your residential status under FEMA, not your income tax status. When you return to India for good, your FEMA status can change and the exemption can stop, even before your income tax position fully shifts. Continuing to treat that interest as tax-free after returning is a common and costly mistake.

6. Can I deposit rent from my Indian property into my NRE account?

No. Indian-source income such as rent, dividends from Indian shares, or sale proceeds of Indian assets must go into an NRO account. An NRE account is only for foreign earnings. Routing India-source income into an NRE account to seek the tax exemption is not permitted and can create problems under FEMA.