If you sold shares or redeemed mutual fund units in FY 2025-26, the tax rules you remember from a few years ago are not the rules that now apply to you. Capital gains tax on shares was reset on 23 July 2024 — rates went up, holding periods were standardised, and indexation was withdrawn for almost everything. On top of that, the Section 87A rebate, which many small investors counted on, no longer covers gains from equity. This post walks through the rules now in force, the points where most retail investors slip, and what to keep ready before filing your return.

Quick answer

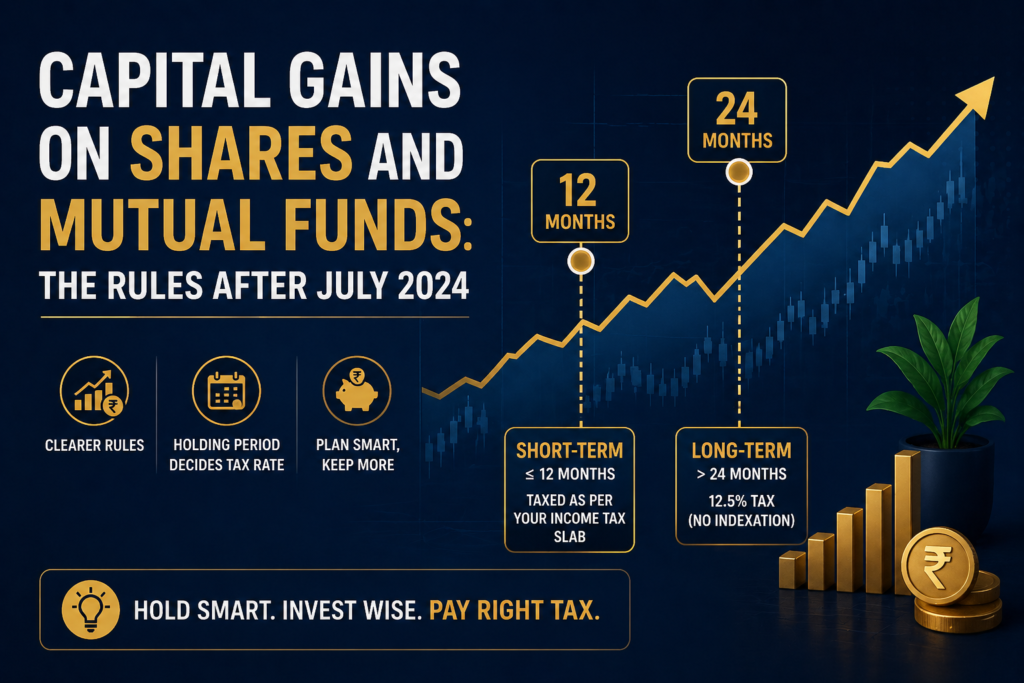

Listed shares and equity mutual funds held for more than 12 months are long-term and taxed at 12.5% on gains above ₹1.25 lakh per year. Held for 12 months or less, they are short-term and taxed at 20%. Debt mutual funds bought on or after 1 April 2023 are always taxed at your slab rate, no matter how long you hold them.

Before acting on any of this, check:

- The exact date of purchase — it decides which rule applies.

- Whether the asset is equity-oriented, debt, or “other” (unlisted shares, gold, property).

- Whether your gains push you above the ₹1.25 lakh annual exemption for equity LTCG.

What capital gains tax on shares actually means

A capital gain is the profit you make when you sell a capital asset for more than you paid for it. For shares and mutual funds, the gain is calculated as the sale price minus the cost of acquisition and minus expenses directly connected with the transfer (brokerage, STT in some cases, demat charges).

There are two big variables that decide how that gain is taxed:

- Holding period — how long you owned the asset before selling. This puts the gain in either the short-term or long-term bucket.

- Type of asset — listed equity shares and equity-oriented mutual funds get a special concessional rate. Debt mutual funds, unlisted shares, and other capital assets follow different rules.

The combination of the two decides the rate. Get either wrong and your tax estimate is wrong.

A quick note on the Acts: the Income Tax Act 1961 still governs income earned up to 31 March 2026, which means it applies to the AY 2026-27 return you are filing now. The Income Tax Act 2025 takes effect from 1 April 2026 onwards. The substantive rules for capital gains have been carried forward, but section numbers and some wording change. In this post, references to Sections 111A, 112, and 112A are to the 1961 Act, since that is what the current return draws from.

Holding period: the line that decides everything

After the changes effective 23 July 2024, the holding period rules were simplified into two broad buckets:

- Listed securities (listed equity shares, equity mutual fund units, listed bonds, units of business trusts): long-term if held for more than 12 months.

- All other capital assets (unlisted shares, immovable property, gold, debt mutual funds bought before 1 April 2023): long-term if held for more than 24 months.

The earlier 36-month rule that applied to debt funds and several other assets is gone. This affects anything sold on or after 23 July 2024.

For SIP investments, each instalment has its own holding period. A redemption is checked unit by unit on a first-in-first-out basis. So a single redemption from an SIP can throw up both short-term and long-term components — the older units may be long-term while the recent ones are still short-term. Investors who redeem the whole corpus in one go are often surprised by the split.

Rates after the 23 July 2024 reset

This is where most of the confusion sits. The numbers below apply to transfers made on or after 23 July 2024, which covers all of FY 2025-26.

Listed equity shares and equity-oriented mutual funds

- Short-term capital gains (Section 111A): 20% flat, plus surcharge and 4% cess. Securities Transaction Tax (STT) must have been paid for this rate to apply.

- Long-term capital gains (Section 112A): 12.5% on gains exceeding ₹1.25 lakh per financial year. The first ₹1.25 lakh of long-term gains across all such equity assets in a year is exempt. No indexation benefit.

The ₹1.25 lakh exemption is a per-investor, per-year limit covering all your listed-equity LTCG combined. Splitting redemptions across funds does not create separate exemptions.

Unlisted shares and other long-term capital assets (gold, jewellery, debt funds bought before April 2023, foreign shares)

- Long-term capital gains (Section 112): 12.5% without indexation.

- Short-term capital gains: added to your total income and taxed at slab rates.

For resident individuals and HUFs who acquired land or buildings before 23 July 2024, an option to compute LTCG at 20% with indexation is available — they choose whichever is lower. This option does not extend to shares or mutual funds.

Surcharge cap

The surcharge on capital gains taxable under Sections 111A, 112, and 112A is capped at 15%, even for high-income taxpayers. This protects investors from the higher 25% and 37% surcharge rates that otherwise apply to non-capital-gains income above ₹2 crore and ₹5 crore.

Debt mutual funds: a separate, harsher rule

Section 50AA, brought in by the Finance Act 2023, removed long-term capital gain status entirely for “specified mutual funds” — broadly, mutual funds with 35% or less invested in domestic equity. The rule is purchase-date sensitive:

- Units bought on or after 1 April 2023: all gains are short-term, regardless of holding period. Taxed at slab rates. No indexation, no LTCG benefit, no concessional rate. A debt fund held for 5 years still produces slab-rate tax.

- Units bought before 1 April 2023: the older rules apply. If sold on or after 23 July 2024 and held more than 24 months, LTCG at 12.5% without indexation. Held 24 months or less, slab rate.

The same logic catches gold ETFs, international fund-of-funds, and most non-equity hybrid funds. A modest portfolio of debt funds bought after April 2023 now generates roughly the same tax bill as a fixed deposit. The tax-efficiency edge debt funds once had has been removed.

What to do at the time of sale

Selling a holding is the easy part. Reporting it correctly is where mistakes happen. Use this checklist before you click “redeem” or place a sell order:

- Confirm the holding period for each lot — separately if it is an SIP or staggered purchase.

- Pull the Capital Gains Statement from your broker or AMC. CAMS and KFintech issue consolidated statements covering most fund houses.

- Match the figures against your AIS (Annual Information Statement) on the Income Tax e-filing portal. Mismatches are now the single biggest reason for ITR notices on capital gains.

- Check whether short-term losses elsewhere can offset the gain — short-term capital losses can be set off against both short-term and long-term gains.

- Long-term losses can only be set off against long-term gains; carry forward up to 8 assessment years if not fully absorbed.

- Pay advance tax on the gain in the quarter the sale falls in. Capital gains are not subject to TDS for resident individuals on equity, but interest under Sections 234B and 234C will apply if advance tax is not paid.

- Report gains in Schedule CG of ITR-2 (or ITR-3 if you also have business income).

Here is how the decision flows for a typical retail investor selling listed shares or equity mutual funds. Variations for debt funds and unlisted assets are covered just below the chart.

Variations on this main path

- Debt mutual funds bought on or after 1 April 2023: skip the holding-period question entirely. All gains are short-term and taxed at slab rate under Section 50AA.

- Unlisted shares, gold, property: the long-term threshold is 24 months, not 12. LTCG is at 12.5% under Section 112; STCG is taxed at slab rates.

- Mixed redemptions from an SIP: treat each instalment as a separate purchase. Some units may qualify as long-term while others are still short-term in the same redemption.

When the Section 87A rebate will not save you

Many small investors assume that if their total income is under the Section 87A threshold, no tax is payable on capital gains either. That assumption no longer works.

The Finance Act 2025 amended Section 87A so that, from FY 2025-26 onwards, the rebate is not available against tax on income chargeable at special rates — including LTCG under Section 112A, LTCG under Section 112, and STCG under Section 111A. The Income Tax Department has confirmed this position. So even if your total income is within ₹12 lakh under the new regime (or ₹5 lakh under the old regime), you must still pay tax on capital gains from listed shares and equity mutual funds. The rebate now only reduces tax on income taxed at normal slab rates.

Other common situations where you should pause before acting:

- Your gains are entirely within the ₹1.25 lakh equity LTCG exemption. No tax is payable, but you must still report the transactions in Schedule CG. Skipping disclosure attracts notices because broker-level data is reported in your AIS.

- You are tempted to “harvest” losses by selling and rebuying within a short window. This is legal, but be sure you understand timing risks and that the loss you book actually carries forward only if you file your ITR by the due date.

- You hold shares received as ESOPs or under a buyback. The cost of acquisition rules differ from a regular market purchase, and applying the wrong base will overstate or understate the gain.

- You are an NRI. Different TDS rates apply at source on equity gains, and treaty relief under a DTAA may need to be invoked. The position cannot be applied straight from a resident’s calculation.

Want to check which regime saves you more. Do check our old vs new regime calculator.

Documents and records to keep ready

A capital gains return needs more documentation than a salary-only return because every transaction has to be traceable to its purchase price, sale price, and date. The list below is organised by source, not as one flat list, so you can collect the documents in batches as they arrive.

From your broker or trading platform

- Capital Gains Statement / Tax P&L Report for FY 2025-26 — most brokers (Zerodha, Groww, Upstox, ICICI Direct, HDFC Securities, Kotak) generate a consolidated P&L that covers shares, equity F&O, and intraday separately

- Contract notes for major buy and sell transactions, especially for any disputed or unusual trade

- Demat holding statement as on 1 April 2025 and 31 March 2026 — your opening and closing positions

- STT certificate, if your broker provides one separately

From mutual fund houses (via CAMS, KFintech, or AMC)

- Consolidated Capital Gains Statement from CAMS (covering most fund houses) and KFintech (covering the rest) for FY 2025-26

- Statement of Account (SoA) for each AMC, especially if you have switched between schemes — switches are treated as redemption-plus-fresh-purchase and must be reported

- For SIPs, a statement that breaks down each instalment with its own purchase date and NAV

From the Income Tax e-filing portal

- Annual Information Statement (AIS) — pulls broker, AMC, and RTA data, and is the single most important document to reconcile against

- Taxpayer Information Summary (TIS) — the summarised version of AIS

- Form 26AS — for any TDS deducted on buybacks, NRI redemptions, or dividends

For specific situations

- Inherited or gifted holdings: original purchase records of the previous owner, plus the gift deed or succession document. The cost of acquisition is taken from the previous owner’s records, not the date you received them.

- ESOPs sold during the year: the perquisite value taxed at exercise (this becomes your cost of acquisition) and the FMV certificate from the company.

- Unlisted shares: share certificates, share transfer forms (SH-4), valuation report if applicable, and the sale agreement.

- Shares sold under a buyback after 1 October 2024: the buyback letter and acceptance — these are now reported as capital gains in Schedule CG, and ITR-2 for AY 2026-27 has a dedicated field for buyback-related capital losses.

- Foreign shares or US stocks (RSUs, ESPP): broker statements (Schwab, Etrade, etc.), Form 1042-S equivalents for any US tax withheld, and FX conversion records.

For loss set-off and carry-forward

- Copies of previous years’ ITR acknowledgements showing capital losses carried forward, with the assessment year of origin clearly identified

- Schedule CFL from prior returns, showing the breakup between short-term and long-term carry-forward losses

For advance tax records

- Challans for any advance tax paid in Q1 (15 June 2025), Q2 (15 September 2025), Q3 (15 December 2025), and Q4 (15 March 2026)

- Self-assessment tax challans, if paid

A practical tip before you start filing: build a single FY 2025-26 folder — physical or on cloud storage — and drop these documents in as they arrive, rather than scrambling at the last minute. CAMS and KFintech statements take 24 to 48 hours to arrive by email and are password-protected (PAN in lowercase plus date of birth in DDMMYYYY format is the most common pattern).

Final takeaway

Capital gains tax on shares and mutual funds is no longer a topic where rough rules of thumb work. The 23 July 2024 reset moved rates upward, killed indexation for equity, and the Finance Act 2025 has removed the Section 87A safety net for special-rate income. The four numbers that matter now are 12 months, 24 months, 12.5%, and 20%. Get those right, match your transactions to your AIS before filing, and report every sale in Schedule CG even when the tax works out to zero. Underreporting is the single biggest trigger for capital gains notices today.

Sold shares or redeemed mutual fund units this year and unsure how the new rates apply to your specific case? eTaxMate can help you reconcile your transactions, compute gains correctly, and file your return with the right schedules in place.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. What is the capital gains tax on shares in India for AY 2026-27?

For listed equity shares and equity mutual funds sold on or after 23 July 2024, short-term capital gains (held 12 months or less) are taxed at 20% under Section 111A. Long-term capital gains (held more than 12 months) are taxed at 12.5% on the amount exceeding ₹1.25 lakh per financial year, under Section 112A. No indexation benefit applies.

2. Is the ₹1.25 lakh LTCG exemption available per fund or in total?

It is a single, combined annual limit. The ₹1.25 lakh exemption applies to the total long-term capital gains from all listed equity shares and equity-oriented mutual funds put together in a financial year, not per scheme or per broker. Splitting redemptions across multiple funds or accounts does not create separate exemptions.

3. How are debt mutual funds taxed if I bought them after April 2023?

All gains are treated as short-term capital gains under Section 50AA, regardless of how long you hold them. They are added to your total income and taxed at your applicable slab rate. There is no long-term capital gains rate, no indexation, and no concessional treatment, which makes their tax behaviour close to that of a fixed deposit.

4. Can I claim the Section 87A rebate against tax on capital gains?

No, not from FY 2025-26 onwards. The Finance Act 2025 amended Section 87A to exclude income taxed at special rates — including LTCG under Sections 112 and 112A and STCG under Section 111A. So even if your total income is below the rebate threshold, you must still pay tax on equity capital gains. The rebate now applies only to tax on slab-rate income.

5. Can I set off a long-term capital loss against my salary or other income?

No. A long-term capital loss can only be set off against long-term capital gains in the same year, not against salary, business income, or other heads. Short-term capital losses are slightly more flexible — they can be set off against both short-term and long-term gains. Unused capital losses can be carried forward for up to 8 assessment years if the return is filed by the due date.

6. Do I need to report equity gains in my ITR if they are below the ₹1.25 lakh exemption?

Yes. Even if no tax is payable because your long-term gains are within the ₹1.25 lakh exemption, the transactions must still be reported in Schedule CG of your ITR. Broker and AMC data is already reflected in your Annual Information Statement, so skipping the disclosure is the most common trigger for capital gains mismatch notices.