Many founders and small traders register under GST and tick the default “regular scheme” without realising there is a second option that could halve their compliance load. Others rush into the composition scheme because a friend said it has lower tax, then lose corporate clients who needed an input tax credit. The composition vs regular GST decision is not about which scheme is “better” — it is about which scheme fits your business model, your customers, and your supply chain. This post breaks down both schemes, where each makes sense, and the traps that catch first-time choosers.

Quick answer

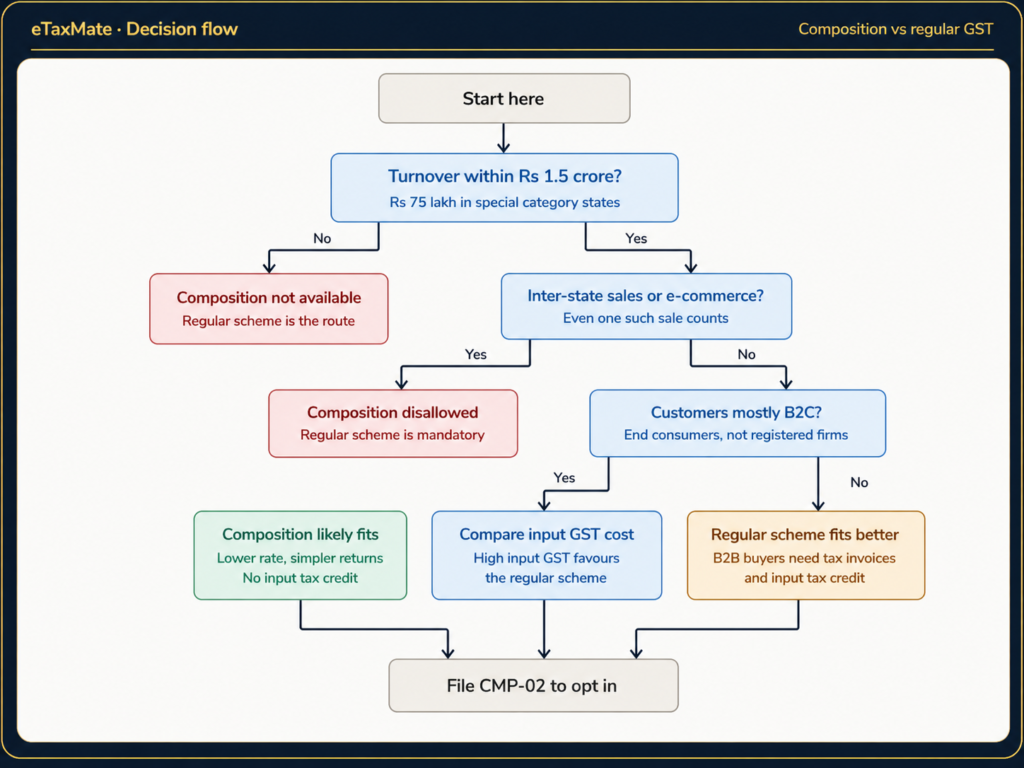

The composition scheme suits small B2C businesses with turnover below ₹1.5 crore (₹75 lakh in special category states) that sell mostly to end consumers and want simpler compliance. The regular scheme suits businesses that sell to other GST-registered buyers, deal in inter-state supplies, or want to claim input tax credit.

Before opting in, check:

- Is your aggregate turnover within the composition limit?

- Are your customers mostly end consumers or GST-registered businesses?

- Do you make any inter-state outward supplies of goods?

What the two schemes actually are

The regular scheme is the default GST framework. You charge GST at the prescribed rate on every taxable supply (5%, 12% now withdrawn, 18%, or 28% now withdrawn, 40%) depending on the item), issue tax invoices, claim input tax credit (the GST you paid on purchases can be set off against the GST you collect on sales), and file monthly or quarterly returns.

The composition scheme is a simplified alternative under Section 10 of the CGST Act 2017. Eligible small businesses pay a fixed low rate of tax on their turnover instead of charging GST on each transaction. They cannot collect GST from customers, cannot claim input tax credit, and cannot issue tax invoices. In exchange, they file fewer returns and keep simpler records.

The choice between composition vs regular GST is essentially a trade-off: lower compliance versus the ability to participate in the input tax credit chain.

Eligibility: who can opt for composition vs regular GST

Not every business can choose the composition scheme. The eligibility filters are strict.

Turnover limit. Aggregate turnover in the preceding financial year must not exceed ₹1.5 crore for most states. For special category states (Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, and Uttarakhand), the limit is ₹75 lakh. Service providers have a separate composition route under Section 10(2A) with a turnover ceiling of ₹50 lakh.

GST registration threshold explainer post in etaxmate previous post’s. Do visit for detailed explanation.

Type of supply. The scheme is primarily for traders, manufacturers, and restaurants. Manufacturers of ice cream, pan masala, tobacco, and aerated waters are explicitly barred.

No inter-state outward supplies. A composition dealer cannot make inter-state outward supplies of goods. Even one such sale disqualifies the business and forces a switch to the regular scheme.

No e-commerce sales. A business selling through e-commerce operators that collect TCS (such as Amazon, Flipkart, Meesho) cannot opt for composition.

No GST-exempt supplies that take the business outside the scheme. A composition dealer can make exempt supplies, but the broader rule is that the dealer must be otherwise eligible to register normally.

The regular scheme has no upper turnover cap and no restrictions on the type of customer or geography.

Tax rates and compliance differences

The composition scheme uses fixed rates on turnover, paid out of the dealer’s own pocket — not collected from the customer.

- Manufacturers and traders: 1% of turnover (0.5% CGST + 0.5% SGST)

- Restaurants (not serving alcohol): 5% of turnover (2.5% CGST + 2.5% SGST)

- Other service providers under Section 10(2A): 6% of turnover (3% CGST + 3% SGST)

Under the regular scheme, the rate depends on what you sell — anywhere from 0% (exempt) to 40%.

For more clarification, visit CBIC portal.

On compliance, the gap is large. A regular dealer files GSTR-1 (outward supplies) and GSTR-3B (summary return) every month or quarter under the QRMP scheme, plus an annual GSTR-9. A composition dealer files only a quarterly statement in CMP-08 and an annual return in GSTR-4. No invoice-level reporting. No monthly reconciliation. No e-invoicing requirement.

For a small kirana store or a neighbourhood restaurant, this difference can mean five to ten hours of monthly compliance saved.

The input tax credit trade-off

This is where the composition vs regular GST decision turns sharp for many businesses.

A regular dealer can claim input tax credit on the GST paid for purchases — raw materials, packaging, rent, professional fees, capital goods. This credit reduces the net GST liability when the dealer collects GST on outward supplies. For a business with significant input GST, the regular scheme is almost always cheaper despite the higher compliance load.

A composition dealer cannot claim any input tax credit. The 1% or 5% paid is a pure cost. If a trader buys goods worth ₹10 lakh with ₹1.8 lakh of GST embedded, that ₹1.8 lakh is gone — it cannot be set off against anything.

There is a second, less obvious cost. A composition dealer cannot pass on input tax credit to buyers either, because the dealer issues a “bill of supply” rather than a tax invoice. This makes the composition dealer unattractive to GST-registered B2B customers, who lose the ability to claim credit on what they buy. A composition dealer who tries to sell to corporate buyers will often find the buyers walking away.

How to choose between composition vs regular GST

The decision rests on three practical questions: who buys from you, where they are located, and how much input GST you pay.

A composition dealer suits a high-volume B2C business with thin input costs and customers who do not need a tax invoice — local kirana shops, small restaurants, neighbourhood salons, modest manufacturing units selling to retail consumers within one state. The simplicity and lower effective tax rate make it the rational choice.

The regular scheme suits any business that sells to other businesses, exports, operates across states, or has significant input GST to recover. Most startups, software service providers, B2B traders, and growing manufacturers fall here. The compliance load is real but manageable, and the input tax credit recovery typically more than offsets it.

Here is how the decision flows for a typical small business owner weighing the two schemes.

Variations on this main path

- Service providers: Use the Section 10(2A) composition route at 6% with a ₹50 lakh turnover ceiling. The decision logic is the same, but the rates and limits differ.

- Restaurants (not serving alcohol): Pay 5% under composition; this is often the most attractive scheme for small restaurants with low input credit.

- Mixed suppliers: A composition trader can supply services up to 10% of turnover or ₹5 lakh, whichever is higher, without losing eligibility.

When you should not opt for the composition scheme

The composition scheme looks attractive on paper, but it is wrong for several common situations.

You sell to GST-registered businesses. Your buyers cannot claim input tax credit on what they buy from you, because you cannot issue a tax invoice. They will quietly switch to a regular-scheme supplier.

You make inter-state outward supplies of goods. Even a single sale to a buyer in another state disqualifies you and forces immediate migration to the regular scheme, often with retrospective tax demands.

You sell on e-commerce platforms. Marketplaces that collect TCS (Amazon, Flipkart, Meesho, and similar) are barred for composition dealers.

Your input GST is high. A trader with thin margins and heavy input GST may end up paying more under composition (1% on full turnover, with no credit) than under the regular scheme (margin × applicable GST rate, with full credit).

You are growing fast. Crossing the ₹1.5 crore threshold mid-year forces a mid-year migration with extensive transitional adjustments. If your turnover trajectory looks likely to breach the limit, starting under the regular scheme avoids the disruption.

Documents and steps before opting in

Keep these ready before filing for the composition scheme on the GST portal:

- GSTIN and login credentials for the portal

- Form CMP-02 (intimation to opt for the composition scheme), filed at the start of the financial year

- Form ITC-03 (reversal of input tax credit on closing stock), filed within 60 days of opting in

- Closing stock statement as on the date of switch, with input GST embedded

- Bank account and business address details, already linked to the GSTIN

- A copy of the previous year’s turnover working, to confirm eligibility

- Customer-mix analysis (B2B vs B2C share) to confirm the scheme suits the business

Final takeaway

The composition vs regular GST decision is not about saving tax. It is about matching the scheme to your business model. If you sell mostly to end consumers within one state, deal in low input GST, and want a simpler compliance routine, composition fits. If you sell to other businesses, work across states, sell online, or have meaningful input GST to recover, the regular scheme is almost always the right call. Choose wrong, and you either lose customers or pay more tax than you needed to.

Confused about whether the composition or regular GST scheme suits your business, or thinking about switching mid-year? eTaxMate can help you review your turnover, customer mix, and input GST profile, and handle the opt-in or migration paperwork correctly.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. What is the turnover limit for the GST composition scheme?

For traders and manufacturers, aggregate turnover in the preceding financial year must not exceed ₹1.5 crore (₹75 lakh in special category states). Service providers under Section 10(2A) have a separate limit of ₹50 lakh. Crossing the threshold mid-year disqualifies the business and forces a switch to the regular scheme from that point.

2. Can a composition dealer claim input tax credit?

No. A composition dealer cannot claim any input tax credit on purchases. The 1% (for traders and manufacturers) or 5% (for restaurants) paid on turnover is a pure cost, not offset against input GST. This is the central trade-off of the scheme — lower compliance and a lower headline rate, but no credit chain participation.

3. Can I sell on Amazon or Flipkart under the composition scheme?

No. A business selling through e-commerce operators that collect TCS — including Amazon, Flipkart, Meesho, and similar marketplaces — cannot opt for the composition scheme. This applies to goods sellers specifically. If online sales are part of your model, the regular scheme is the only option, regardless of turnover size.

4. How do I switch from composition to regular GST scheme?

File Form CMP-04 on the GST portal to withdraw from the composition scheme, either voluntarily or because of disqualification. After withdrawal, claim input tax credit on closing stock by filing Form ITC-01 within 30 days. From that date onwards, charge GST at the regular applicable rates and file GSTR-1 and GSTR-3B returns.

5. Is the composition scheme good for B2B businesses?

Usually no. A composition dealer issues a bill of supply, not a tax invoice, so GST-registered B2B customers cannot claim input tax credit on what they buy. Most corporate buyers will switch to a regular-scheme supplier for this reason. The composition scheme is designed for B2C businesses selling to end consumers who do not need a tax invoice.

6. What returns does a composition dealer file?

A composition dealer files Form CMP-08 quarterly (a simple statement of self-assessed tax) by the 18th of the month following each quarter, and Form GSTR-4 annually by 30 June following the financial year. There is no monthly GSTR-1 or GSTR-3B and no invoice-level reporting, which is the main compliance advantage over the regular scheme.