A common belief among retirees is that once you stop working, you no longer need to file an income tax return — or that having tax deducted at source settles everything. Both ideas are usually wrong. The senior citizen ITR rules give older taxpayers some genuine relief, including higher exemption limits and a few special deductions, but they do not generally remove the duty to file. This post answers the basic questions a senior citizen or their family actually has: do you need to file, what are the limits, what can you claim, and where is the one real exemption from filing.

Quick answer

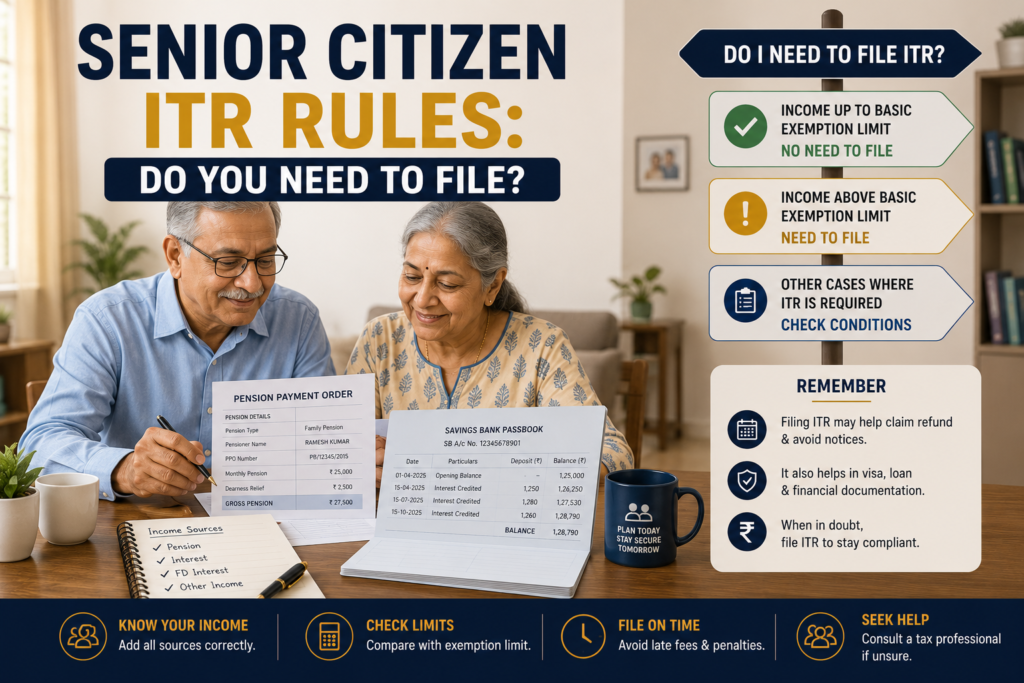

Most senior citizens still need to file an ITR. There is only one full exemption from filing — for certain resident pensioners aged 75 and above with very simple income — under Section 194P. Higher exemption limits and deductions lower the tax, but they rarely remove the filing requirement.

Before acting, check:

- Is the person a senior citizen (60–80) or a super senior citizen (80+)?

- Is their total income above the basic exemption limit that applies to them?

- Do they meet every Section 194P condition, or do they still need to file?

Who counts as a senior citizen for tax

For income tax, age is measured by whether you reached the relevant age at any time during the financial year. A resident individual aged 60 or above but below 80 during FY 2025-26 is a senior citizen. A resident aged 80 or above is a super senior citizen.

The timing rule is generous at the edge. If someone turns 60 on 1 April 2026, they are treated as 60 on 31 March 2026 and so qualify as a senior citizen for FY 2025-26. The return you file in 2026 is for FY 2025-26 (AY 2026-27) under the Income Tax Act 1961, even though the new Income Tax Act 2025 took effect on 1 April 2026.

Do senior citizens always need to file?

The honest answer: almost always, yes — with one narrow exception covered below.

A senior citizen must file a return if their total income before deductions exceeds the basic exemption limit that applies to them. The fact that a bank already deducted TDS does not change this. Many seniors assume TDS is the end of the matter; in reality, if TDS was deducted but the actual tax due is lower, the only way to get that money back is to file and claim a refund. Filing is also how you reconcile your income against your AIS, which now captures pension, interest, and other receipts.

So the trigger is not employment — it is income crossing the exemption limit. A retired person living on a pension and FD interest that together exceed the limit must file, even though they have no job.

The exemption limits that decide whether you file

This is where age and regime both matter, so read carefully.

Under the old regime, senior citizens get a higher basic exemption limit of ₹3 lakh, and super senior citizens get ₹5 lakh — more generous than the ₹2.5 lakh for those under 60. These higher limits are a real, age-based benefit of the old regime.

Under the new regime, which is the default for AY 2026-27, the basic exemption limit is a flat ₹4 lakh for everyone, with no extra allowance for age. However, the new regime offers a much larger Section 87A rebate, so a resident with taxable income up to ₹12 lakh effectively pays no tax. Salaried and pension income also gets a ₹75,000 standard deduction under the new regime, against ₹50,000 under the old.

The practical effect: a super senior citizen with modest income may find the old regime’s ₹5 lakh exemption simpler, while a senior with higher income and few deductions may do better under the new regime’s rebate. It is worth taking the time to compare the old and new regime properly rather than assuming the old one is always kinder to seniors.

Section 194P: the one case where filing is waived

There is exactly one situation where a senior citizen is fully relieved from filing a return, and it is narrow. Under Section 194P, a resident senior citizen aged 75 or above does not need to file an ITR if all of these are true:

- They are a resident individual aged 75 or above during the year.

- Their income consists only of pension and interest.

- Both the pension and the interest come from the same specified bank.

- They submit a declaration in Form 12BBA to that specified bank.

When these are met, the specified bank computes the tax after allowing the applicable deductions and rebate, deducts it, and the senior citizen need not file separately. The moment any condition fails — interest from a second bank, any capital gain, rental income — the exemption does not apply and a normal return is required.

Take a retired couple: the husband, aged 78, draws his pension and keeps all his deposits in the same bank, and submits Form 12BBA — he qualifies under 194P and need not file. His wife, aged 76, also has rental income from a shop, so she falls outside 194P and must file a normal return.

Deductions and reliefs built for senior citizens

Even where filing is required, seniors get specific reliefs:

- Section 80TTB allows a resident senior citizen a deduction of up to ₹50,000 on interest from savings accounts, fixed deposits, and post office deposits — far more generous than the ₹10,000 savings-only limit for younger taxpayers. You can claim the Section 80TTB deduction on interest only under the old regime.

- Higher medical insurance deduction under Section 80D applies to senior citizens.

- No advance tax is required from a senior citizen who has no business or professional income; they simply pay any balance as self-assessment tax when filing, and avoid the related interest.

Note that 80TTB and most other deductions sit only in the old regime. Under the new regime, the trade-off is a higher rebate and standard deduction instead.

How a senior citizen should approach filing

Work through it in order.

First, fix the age category — senior or super senior — based on age during FY 2025-26.

Second, total all income: pension, interest from every bank, any rent, dividends, and capital gains.

Third, check whether that total crosses the exemption limit for the chosen regime.

Fourth, test the four Section 194P conditions — if every one is met, filing may be waived; if not, plan to file.

Fifth, choose the regime after comparing the old regime’s higher exemption and 80TTB against the new regime’s larger rebate.

Sixth, reconcile everything against the AIS and Form 26AS, and claim credit for any TDS.

When a senior citizen should still file even if not required

Even where income is below the limit, filing is often the wiser move:

- TDS was deducted and you are owed a refund. Banks can deduct TDS on interest. If your income is below the taxable limit, that TDS only comes back if you file. Not filing means leaving your own money with the department.

- You want a clean record for visas, loans, or property. A filed return is widely accepted proof of income for many purposes, and seniors increasingly need it for travel and large transactions.

- You have capital gains or sold property. These fall outside the Section 194P exemption and outside simple slab logic, so a return is needed even if your routine income is small.

- Your AIS shows transactions you have not explained. Filing lets you reconcile high-value entries before they turn into a query.

For seniors, the question is rarely “must I file” alone — it is often “will filing get me a refund or save trouble.”

Quick checklist before you file

📋 Keep these ready for a senior citizen’s return:

- Pension statements and Form 16 (if pension is paid through a bank or former employer)

- Interest certificates from every bank, FD, RD, and post office account

- Form 26AS and AIS, to reconcile income and claim TDS credit

- Details for Section 80TTB (interest) and Section 80D (medical insurance), if using the old regime

- Form 12BBA acknowledgement, if claiming the Section 194P waiver

- Records of any capital gains, rent, or dividends — these can change the form and the regime; follow a full pre-filing checklist to avoid missing anything

Final takeaway

The senior citizen ITR rules give older taxpayers higher exemption limits, a larger 80TTB deduction, and freedom from advance tax — but they do not generally excuse you from filing. The only full waiver is Section 194P, for resident pensioners aged 75 and above with pension and interest from a single bank who submit Form 12BBA. For everyone else, filing crosses the exemption limit, and TDS is not a substitute for a return. When in doubt, filing usually protects your refund and your record.

Confused about whether a senior citizen in your family needs to file, or which regime and deductions apply to a pensioner’s income? eTaxMate can help you check the exemption limits, test the Section 194P conditions, and file the return correctly for AY 2026-27.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. Do senior citizens have to file an ITR?

In most cases, yes. A senior citizen must file if their total income before deductions crosses the basic exemption limit that applies to them. Having TDS deducted does not remove this duty. The only full exemption is under Section 194P, for resident pensioners aged 75 and above whose income is only pension and interest from the same specified bank.

2. What is the basic exemption limit for senior citizens in AY 2026-27?

Under the old regime, it is ₹3 lakh for senior citizens (60–80) and ₹5 lakh for super senior citizens (80+). Under the new regime, which is the default, it is a flat ₹4 lakh for all ages, but the larger Section 87A rebate makes income up to ₹12 lakh effectively tax-free.

3. Who is exempt from filing ITR under Section 194P?

A resident senior citizen aged 75 or above is exempt from filing if their income consists only of pension and interest, both received from the same specified bank, and they submit a declaration in Form 12BBA to that bank. The bank then deducts the correct tax. If any condition fails, a normal return is required.

4. Can senior citizens claim Section 80TTB on interest income?

Yes, but only under the old regime. Section 80TTB lets a resident senior citizen deduct up to ₹50,000 of interest from savings accounts, fixed deposits, and post office deposits — much more than the ₹10,000 savings-only limit for younger taxpayers. Under the new regime, this deduction is not available, though the higher rebate may compensate.

5. Are senior citizens required to pay advance tax?

A senior citizen with no income from business or profession is not required to pay advance tax. They can pay any tax due as self-assessment tax when filing the return, and they avoid the interest that otherwise applies for not paying advance tax. Seniors who do run a business or profession are not covered by this relief.

6. Should a senior citizen file even if income is below the limit?

Often, yes. If a bank deducted TDS on interest and the actual tax due is lower, filing is the only way to claim that refund. A filed return also serves as accepted income proof for visas, loans, and property, and lets a senior reconcile any high-value entries in their AIS before they prompt a query from the department.