If you are a freelancer, consultant, or anyone earning income from business or profession, choosing the old tax regime requires more than ticking a box. You must file a separate form — Form 10-IEA — before your income tax return and before the deadline. Miss it, and your return is processed under the new regime regardless of intent, with no correction in a revised return. This post explains exactly who needs it, what it does, and where the costly mistakes happen.

Quick answer

Form 10-IEA is a statutory declaration under Section 115BAC(6) of the Income Tax Act 1961. Mandatory for individuals and HUFs with business or professional income who want the old tax regime. It must be submitted online before the ITR due date under Section 139(1). For AY 2026-27, the statutory deadline is 31 July 2026 — though CBDT has extended this in prior years, watch for any official notification before assuming the date holds.

Before acting, check:

- Do you have income from business or profession? Only then is Form 10-IEA required.

- Have you previously filed Form 10-IEA and switched back to the new regime? If yes, you may have exhausted your option.

- Have you compared your tax under both regimes before committing? Form 10-IEA cannot be withdrawn once e-verified.

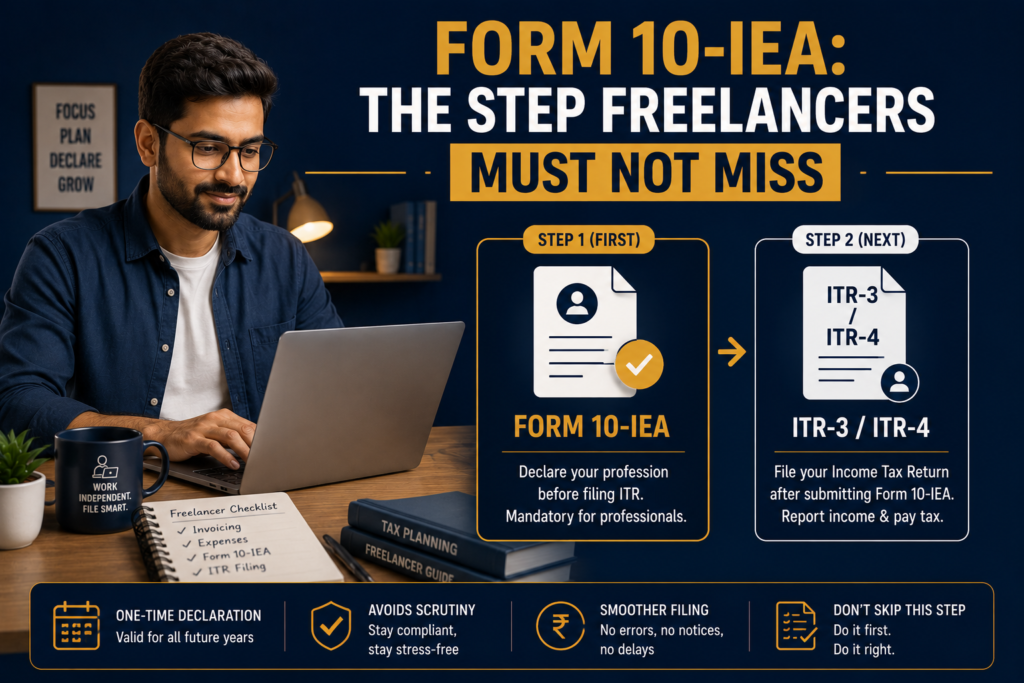

What Form 10-IEA is and why it exists

The new tax regime under Section 115BAC is the default for all individual and HUF taxpayers from AY 2024-25 onwards. Without any action, every taxpayer is assumed to be in the new regime.

For salaried individuals filing ITR-1 or ITR-2, opting out is simple — the ITR form asks whether they want to switch, and selecting Yes is sufficient. No separate form needed.

For taxpayers with business or professional income — freelancers, consultants, proprietors, F&O traders, and anyone filing ITR-3 or ITR-4 — the law imposes a stricter requirement. Their regime choice must be recorded in a separate statutory form filed before the ITR. That form is Form 10-IEA, introduced by CBDT Notification No. 43/2023 dated 21 June 2023.

Salaried employees who have no freelance or business income face a completely different set of rules — their regime choice at ITR time is far more flexible, as our post on what to do when your employer chose the new regime explains.

Who must file Form 10-IEA — and who does not

The requirement is determined by whether you have income from business or profession — not by your job title.

Form 10-IEA is required for: freelancers and independent professionals, consultants and advisors earning professional fees, sole proprietors and small business owners, individuals with intraday or F&O trading income (classified as business income), and HUFs with business or professional income.

Form 10-IEA is not required for: salaried individuals with no business income filing ITR-1 or ITR-2, or anyone whose only income is salary, interest, pension, or rent.

The test is simple: ITR-3 or ITR-4 → Form 10-IEA required. ITR-1 or ITR-2 → not required.

One edge case worth flagging: a salaried employee who also does occasional freelance work shifts into ITR-3 or ITR-4 territory. From that point, Form 10-IEA is mandatory — the salaried flexibility to switch regimes freely no longer applies.

The lifetime switch rule: what it actually means

This is the most misunderstood aspect of Form 10-IEA.

Once you file Form 10-IEA and switch to the old regime, you stay there automatically in subsequent years — no need to refile each year. When you later want to return to the new regime, you file Form 10-IEA again. That return is permitted — but only once. After switching back to new, the old regime is permanently unavailable.

The sequence in practice:

- Year 1 (default): New regime. No form filed.

- Year 2: Form 10-IEA filed → old regime.

- Year 3, 4, 5: Old regime continues automatically. No form needed.

- Year 6: Form 10-IEA filed again → back to new regime. This exhausts the lifetime option.

- Year 7 onwards: Locked in new regime permanently.

The form can be filed at most twice in a lifetime — once to leave the new regime, once to return.

Before filing Form 10-IEA, the decision should be grounded in an actual comparison of your tax under both regimes — our post on old tax regime vs new tax regime walks through the key deductions that make the old regime worth choosing.

What Arjun’s case shows you

Arjun is a freelance UX designer in Bengaluru earning ₹18 lakh per year in professional fees. He files ITR-4 under Section 44ADA. Under that scheme, 50% of gross receipts is declared as taxable income — so his starting figure is ₹9 lakh.

For AY 2026-27 he runs both scenarios:

- New regime: ₹9 lakh minus ₹75,000 standard deduction = tax on ₹8.25 lakh

- Old regime: ₹9 lakh minus standard deduction (₹50,000), 80C (₹1.2 lakh), 80D (₹20,000) = tax on roughly ₹7.1 lakh

The old regime saves him around ₹8,000–₹10,000. To access it, he must file Form 10-IEA first, then file ITR-4. If he files ITR-4 first, the return locks into the new regime with no fix.

Since Arjun has never filed Form 10-IEA before, his lifetime option is intact. He files, saves the acknowledgement number, enters it in Part A of his ITR-4, and files within the due date.

Most freelancers and consultants filing ITR-4 under Section 44ADA will be directly affected by this requirement — our post on Section 44ADA presumptive taxation covers how that scheme works before you decide which regime makes sense.

How to file Form 10-IEA: the steps

Form 10-IEA is filed entirely online through the income tax e-filing portal. No offline or physical submission exists.

- Log in to the e-filing portal using PAN and password.

- Go to: e-File → Income Tax Forms → File Income Tax Forms, then search for Form 10-IEA.

- Select the assessment year (AY 2026-27 for FY 2025-26).

- Part 1 (name, PAN, AY, taxpayer status) is pre-filled. Select whether you are opting out of the new regime (first switch to old) or re-entering the new regime (return from old).

- Fill Part 2 if applicable (IFSC unit details).

- Submit and e-verify using Aadhaar OTP or Digital Signature Certificate.

- Save the acknowledgement number — you will enter it in Part A of ITR-3 or ITR-4 when filing.

The form must be submitted before the ITR. Submitting Form 10-IEA after filing the ITR does not change the regime for that return.

Who needs Form 10-IEA vs who does not: a quick comparison

Here is a side-by-side of how the two groups differ — the most common source of confusion in this topic.

One important note on the horizon: the draft Income Tax Rules 2026 have proposed removing the mandatory Form 10-IEA requirement, proposing that business-income taxpayers could also select their regime directly within the ITR. As of AY 2026-27, those draft rules are not in force and Form 10-IEA remains mandatory. If the finalised rules change this, Madhvendra should update this post accordingly.

When you should not delay or assume

Do not assume you are salaried-only if you have any business income. Even occasional freelance invoicing creates business income placing you in ITR-3 or ITR-4 territory, triggering the Form 10-IEA requirement.

Do not refile Form 10-IEA unnecessarily if already in the old regime. Once switched, you stay automatically. Filing again when already in the old regime records a return to the new regime — using your once-in-a-lifetime exit.

Do not wait until the ITR deadline to file Form 10-IEA. The form must go in before the ITR. Both deadlines fall on the same date — submit Form 10-IEA at least a week ahead to avoid portal issues.

Do not file without running the numbers first. Once e-verified, the form cannot be withdrawn. The only correction is a new filing the following year, at the cost of your return option.

Do not confuse Form 10-IEA with the discontinued Form 10-IE. Form 10-IE was used to opt for the new regime when the old regime was the default (up to AY 2022-23). Form 10-IEA is the current form.

Documents and details to keep ready

- PAN and password for the income tax e-filing portal

- Confirmed assessment year (AY 2026-27 for FY 2025-26)

- Tax computation under both regimes showing that old regime results in lower liability — prepared before submitting Form 10-IEA

- Deduction proofs if switching to old regime: 80C receipts (PPF, ELSS, LIC), health insurance premium certificates for 80D, home loan interest certificate for Section 24(b)

- Acknowledgement number from Form 10-IEA submission — required in Part A of ITR-3 or ITR-4

- Digital Signature Certificate (DSC) if e-verifying via DSC rather than Aadhaar OTP

- Note of whether you have previously filed Form 10-IEA in any earlier year — this determines whether your lifetime option is intact

Final takeaway

Form 10-IEA is the mandatory pre-step for any freelancer, consultant, or business-income taxpayer who wants the old tax regime. File it before the ITR, not after. Do not refile if already in the old regime. Do not commit without comparing liability under both regimes — because once e-verified, the form stands and the lifetime switch count moves. Miss it, and you spend a year in the new regime with no fix.

Unsure whether Form 10-IEA applies to your income, or want a regime comparison before committing? eTaxMate can review your income profile, confirm the right form to file, and handle your ITR-3 or ITR-4 correctly.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. What is Form 10-IEA and who needs to file it?

Form 10-IEA is a statutory declaration under Section 115BAC(6) of the Income Tax Act 1961. It must be filed by individuals and HUFs who have income from business or profession — freelancers, consultants, proprietors, F&O traders — and want to opt for the old tax regime. Salaried individuals with no business income do not need it; they can switch regimes directly within the ITR form.

2. Do I need to file Form 10-IEA every year to stay in the old tax regime?

No. Once you file Form 10-IEA and switch to the old regime, you remain there automatically in subsequent years. You do not need to refile each year. The form is required again only if you decide to switch back to the new regime — and that return switch is permitted only once in a lifetime.

3. What happens if I miss the Form 10-IEA deadline?

If you miss the deadline — which is the same as the ITR due date under Section 139(1) — your return is processed under the new tax regime by default, regardless of your intent. A revised return cannot fix this. You lose the old regime for that year entirely. There is no direct monetary penalty for missing the form itself, but the indirect cost is the loss of all old-regime deductions for that assessment year.

4. Can I switch back to the new regime after filing Form 10-IEA?

Yes, but only once in a lifetime. After switching to the old regime via Form 10-IEA, you can return to the new regime by filing Form 10-IEA again. However, once you have re-entered the new regime this way, you cannot go back to the old regime again — the option is permanently exhausted.

5. A salaried employee told me Form 10-IEA is not needed. Is that correct for me as a freelancer?

It is correct for that salaried employee — but not for you. Salaried individuals with no business income switch regimes by answering a question in ITR-1 or ITR-2. Freelancers and consultants with business or professional income must file Form 10-IEA separately before filing ITR-3 or ITR-4. The two groups follow different rules under Section 115BAC, and confusing them is one of the most common filing errors among self-employed taxpayers.

6. I do occasional freelance work alongside my salary. Do I need Form 10-IEA?

Yes, if your freelance income is classified as business or professional income and you are filing ITR-3 or ITR-4. Any business or professional income — even occasional or part-time — places you in the category that requires Form 10-IEA to opt for the old regime. The salaried-employee flexibility of switching freely every year does not apply once you have business income.