Many freelancers in India treat GST and income tax as the same thing. They are not. Income tax is on your earnings — computed annually, filed as an ITR. GST is on the services you supply — collected from clients on each invoice, remitted monthly or quarterly. The two systems run on separate portals under separate laws, and satisfying one does not satisfy the other. This post covers GST for freelancers in India only: when it kicks in for freelancers and what changes when you bill foreign clients.

Quick answer

Freelancers must register for GST once aggregate turnover from services crosses ₹20 lakh in a financial year (₹10 lakh in special category states). Below that threshold, GST registration is generally not mandatory — including for interstate service work — under Notification No. 10/2017-IGST. Standard rate on most freelance services: 18%. Foreign client invoices are zero-rated if payment arrives in convertible foreign exchange.

Before acting, check:

- Has your total service income crossed ₹20 lakh this financial year?

- Do you pay for foreign tools (Upwork fees, Adobe, Zoom) where no Indian GST is charged? Reverse charge may force registration regardless of turnover.

- Are you billing foreign clients and GST-registered? Those invoices need specific treatment to be zero-rated.

GST and income tax are two separate obligations

This is where most freelancer confusion begins. The two systems are governed by different laws, filed on different portals, and computed on different bases.

Income tax applies to your net income — receipts minus eligible expenses — filed annually on the income tax e-filing portal under the Income Tax Act 1961.

GST applies to the full value of services you supply — not net of expenses — filed monthly or quarterly on the GST portal under the CGST Act 2017. GST collected from clients is not your income; it is a liability you hold and remit.

Both obligations are triggered independently. A freelancer earning ₹25 lakh files income tax on their net earnings and also registers for GST and files GSTR-1 and GSTR-3B. Satisfying one does not satisfy the other.

GST and income tax are separate obligations — our post on ITR filing for freelancers covers how Section 44ADA and ITR-4 work on the income tax side.

When GST registration becomes mandatory for freelancers

Under Section 22 of the CGST Act 2017, registration is mandatory once aggregate turnover crosses ₹20 lakh in a financial year. In special category states (Arunachal Pradesh, Assam, J&K, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh, Uttarakhand), the threshold is ₹10 lakh.

Two errors are very common here. First: the ₹40 lakh threshold applies to goods suppliers only — not service providers. Freelancers remain at ₹20 lakh. Second: billing clients in other states does not force registration for service providers below the threshold. Notification No. 10/2017-IGST exempts service providers below ₹20 lakh from mandatory registration even for interstate supplies. This is different from goods suppliers, where interstate supply triggers registration regardless of turnover.

Voluntary registration is available below the threshold for those who want to claim ITC on business expenses or issue GST invoices to corporate clients. Once registered, all return filing obligations apply regardless of turnover.

The full picture of compulsory registration categories — which can apply regardless of turnover — is covered in our post on the GST registration threshold.

What counts as aggregate turnover — and what does not

Aggregate turnover under Section 2(6) of the CGST Act 2017 includes all taxable supplies, all exempt supplies, all exports of goods and services, and all interstate supplies — computed PAN-wide across all states and all GSTINs.

In practice: freelance income from every client in every state is counted together. Export earnings from foreign clients are included even though they are zero-rated. If you also earn rental income or royalties, those count too.

What is excluded: GST itself, and inward supplies on which you pay tax under reverse charge.

A practical example: a content writer earns ₹12 lakh from domestic clients and ₹9 lakh from a UK-based publication. Aggregate turnover is ₹21 lakh — registration is mandatory, even though the export portion is zero-rated.

GST rate on freelance services: the number that surprises people

Most freelance services attract GST at 18%. IT development, software services, content writing, graphic design, marketing consulting, financial advisory, and most other professional or creative services fall here. Some services — healthcare, certain educational services — may be exempt, but 18% is the working number for almost every freelancer.

Once registered, you charge 18% GST on top of your fee for every domestic client invoice. A ₹1 lakh project invoice becomes ₹1.18 lakh — ₹18,000 of which you collect and deposit with the government. That ₹18,000 is not your income.

Every GST invoice must include your GSTIN, the client’s name and GSTIN (for B2B clients), invoice number, date, service description, SAC (Services Accounting Code), tax rate, tax amount, and place of supply. From 1 April 2021, SAC codes are mandatory on all invoices issued to GST-registered clients.

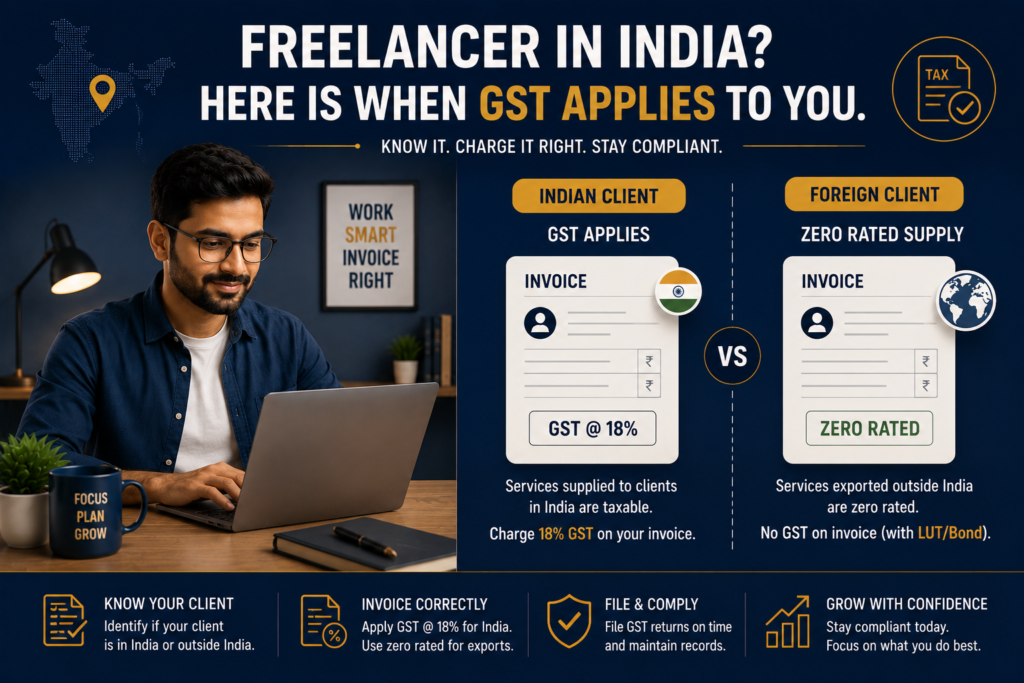

Billing Indian clients vs foreign clients: two different paths

Indian clients: You charge 18% GST on the invoice, collect it, report in GSTR-1, and remit via GSTR-3B. For B2B clients, the GST you charge is claimable by them as ITC — often neutral to the client.

Foreign clients: If the service qualifies as an export under Section 2(6) of the IGST Act 2017, it is zero-rated — 0% GST. The key conditions: supplier in India, recipient outside India, payment in convertible foreign exchange (or RBI-permitted INR), and supplier and recipient not mere establishments of the same person.

Registered freelancers billing foreign clients zero-rated have two routes: pay IGST and claim refund later, or file an LUT before invoicing and export with no IGST. The LUT route is almost always better for cash flow.

If you bill foreign clients and your turnover crosses the threshold, filing an LUT before your first export invoice keeps IGST out of your cash flow — our post on LUT under GST covers exactly how.

Key GST facts for freelancers at a glance

Here is a quick-reference infographic covering the essential GST parameters every freelancer in India needs to know.

The RCM trap: when using foreign tools forces registration

If you pay for services from a foreign provider who does not charge Indian GST — Upwork service fees, Adobe Creative Cloud, Zoom paid plans, Figma, Canva Pro — those payments are treated as imports of services under GST, typically as OIDAR (Online Information and Database Access or Retrieval) services.

Under the reverse charge mechanism, when you import services from outside India, you — the Indian recipient — become liable to pay 18% GST on those fees, even though the foreign provider charged you nothing under Indian GST.

The critical consequence: RCM on import of services is a compulsory registration trigger under Section 24 of the CGST Act 2017. No turnover threshold applies. If foreign SaaS tools are invoicing you without Indian GST, you must register — even if your own freelance income is well below ₹20 lakh.

Once registered, you pay the 18% GST on platform fees via GSTR-3B each period and claim the same back as ITC — net cash impact nil for most freelancers. But the filing obligation runs every return period.

What Priya’s case shows you

Priya is a freelance UI/UX designer in Hyderabad earning ₹18 lakh per year — ₹12 lakh from Indian clients and ₹6 lakh from a UK-based startup paid in GBP. She uses Adobe Creative Cloud (no Indian GST on invoice), Figma Professional (no Indian GST), and Upwork which charges a service fee.

Three questions settle her GST position.

Is her aggregate turnover above ₹20 lakh? No — ₹18 lakh total. Registration is not mandatory on turnover grounds.

Does she use foreign tools without Indian GST? Yes. Adobe, Figma, and Upwork service fees are OIDAR imports — RCM applies. She must register regardless of her ₹18 lakh total.

What happens after registering? She pays 18% GST on platform fees via GSTR-3B and reclaims the same as ITC — net nil. Her Indian client invoices remain non-GST (below threshold, domestic billing). Her UK invoices are zero-rated exports; she files an LUT and reports them in Table 6B of GSTR-1.

When you should not wait to register

Turnover approaching ₹20 lakh. Registration takes a few days to a week. If you cross the limit mid-month without being registered, you face a liability gap. Apply before crossing, not after.

Losing B2B clients because you cannot issue GST invoices. Corporate clients often require a GST invoice to claim ITC. An unregistered freelancer cannot provide one. Voluntary registration solves this.

Using paid foreign tools without Indian GST. RCM on OIDAR services is a compulsory registration trigger independent of your own turnover. If Adobe, Zoom, or Figma invoices arrive without Indian GST, check whether RCM applies.

Formalising for funding or government contracts. A GSTIN is increasingly required for startup grants, institutional clients, and government tenders. Voluntary registration provides it immediately.

Documents and details to keep ready

- PAN card (mandatory for GST registration)

- Aadhaar card of the proprietor or authorised signatory

- Photograph of the applicant

- Bank account details with a cancelled cheque or bank statement

- Proof of principal place of business: rent agreement or electricity bill or property tax receipt

- Mobile number and email for OTP-based verification on the GST portal

- A record of total service income for the current financial year — to confirm whether the threshold has been crossed or is close

Final takeaway

GST for freelancers in India applies when aggregate turnover crosses ₹20 lakh — not because of interstate billing, not because of foreign exchange income. The ₹40 lakh threshold is for goods only. Below ₹20 lakh, interstate service work does not force registration. What does force registration regardless of turnover is an RCM liability on OIDAR imports. And once registered, foreign invoices are zero-rated — reported at 0% in GSTR-1, not ignored.

Earning above ₹20 lakh, using paid foreign tools, or unsure whether GST applies? eTaxMate can confirm your position, handle registration, and manage your GSTR-1 and GSTR-3B filings.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. Do freelancers in India need to register for GST?

GST registration is mandatory once a freelancer’s aggregate turnover from all services exceeds Rs 20 lakh in a financial year (Rs 10 lakh in special category states like Arunachal Pradesh, Manipur, or Uttarakhand). Below this threshold, registration is generally not required — even for interstate client work — under Notification No. 10/2017-IGST. However, registration becomes mandatory regardless of turnover if you have a reverse charge liability on imported services.

2. What is the GST rate for freelancers in India?

Most freelance services — IT development, content writing, graphic design, consulting, digital marketing — attract GST at 18% under SAC code group 9983. This applies when billing Indian clients. Services to foreign clients qualify as exports and are zero-rated (0% GST), provided payment is received in convertible foreign exchange and other export conditions are met.

3. Does billing clients in other states require GST registration if I am below Rs 20 lakh?

No, not for service providers. Notification No. 10/2017-IGST (amended by 10/2019-IGST) specifically exempts service providers below the registration threshold from mandatory registration even for interstate supplies. This is different from goods suppliers, for whom interstate supply triggers mandatory registration regardless of turnover. As a freelancer providing services, the threshold test governs — not the interstate rule.

4. I use Adobe, Zoom, and Upwork. Does that affect my GST obligations?

Yes. When foreign platforms charge service fees without levying Indian GST, those fees are treated as imports of services (often OIDAR services). Under the reverse charge mechanism, you — as the Indian recipient — become liable to pay 18% GST on those fees. This triggers mandatory GST registration regardless of your overall freelance turnover. Once registered, you pay the GST on those fees via GSTR-3B and claim it back as Input Tax Credit, so the net cash impact is often nil — but the filing obligation is real.

5. Do I charge GST on invoices to foreign clients?

If the supply qualifies as an export of services — the client is outside India, payment comes in foreign currency, and other conditions under Section 2(6) of the IGST Act 2017 are met — the invoice is zero-rated. You do not charge 18% GST. Instead, if you are registered for GST, you file a Letter of Undertaking (LUT) before raising the invoice and report the export in Table 6B of GSTR-1. This is different from being exempt — you still report the transaction, just at 0% GST.

6. What GST returns does a registered freelancer need to file?

A registered freelancer files GSTR-1 (details of outward supplies — your invoices) and GSTR-3B (monthly summary of supplies and tax payment). Freelancers with annual turnover up to Rs 5 crore can opt for quarterly filing under the QRMP (Quarterly Return Monthly Payment) scheme, where GSTR-1 and GSTR-3B are filed quarterly rather than monthly. Nil returns must be filed even in months with no invoices.