If your startup exports software to a client in the US, supplies SaaS to a company in Singapore, or sells goods to an SEZ unit in India, you are making zero-rated supplies under GST. Zero-rated does not mean ignored. It means you have two choices: pay IGST on every invoice and wait months for a refund, or file a Letter of Undertaking first and export with no IGST outflow at all. Most growing businesses should be on the second route.

Quick answer

An LUT (Letter of Undertaking) under GST is filed in Form GST RFD-11 on the GST portal. It allows a GST-registered exporter or SEZ supplier to issue zero-rated invoices without paying IGST upfront. Valid for one financial year. Must be filed before the first export of each year. Renewed annually. Legal basis: Section 16 of the IGST Act 2017, Rule 96A of the CGST Rules 2017.

Before acting, check:

- Are you making exports of goods or services, or supplying to an SEZ?

- Has your business been prosecuted for tax evasion exceeding ₹2.5 crore? If yes, a bond is required instead of an LUT.

- Is your LUT filed before your first export invoice of this financial year?

What LUT under GST is and why it exists

Under Section 16 of the IGST Act 2017, exports and supplies to Special Economic Zones are zero-rated — effective GST is nil. The law gives exporters two ways to achieve that zero-rating.

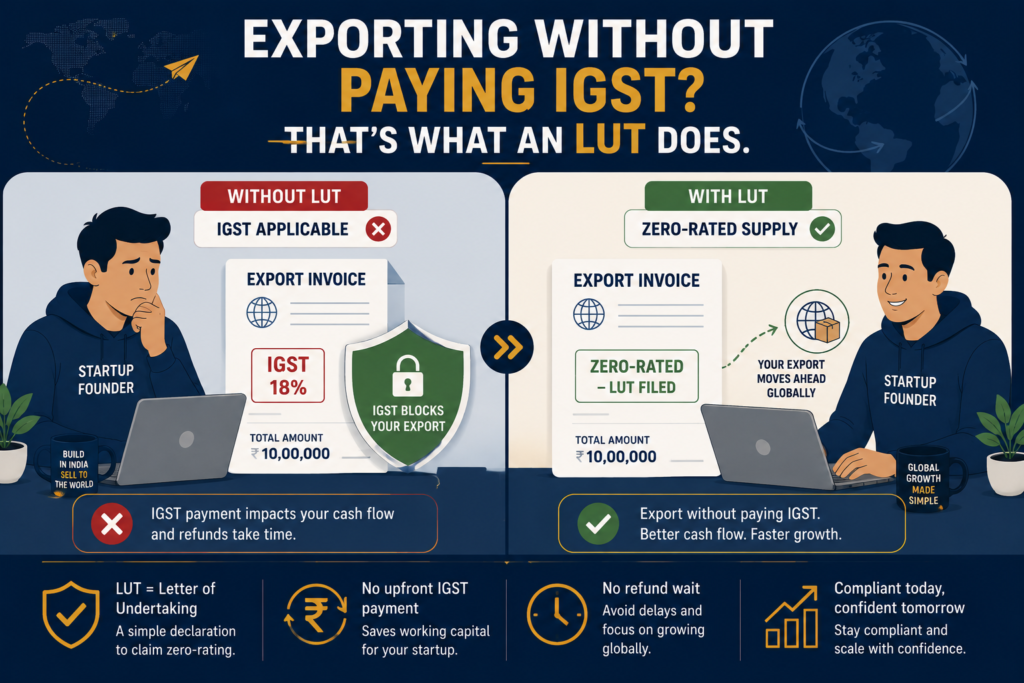

First: pay IGST on the export invoice and claim a refund later. Second: file an LUT before exporting, allowing invoices to go out with no IGST charged. If the exporter complies with export timelines, no IGST is ever due. If they do not, IGST plus 18% interest becomes payable within 15 days of the default.

The LUT is filed in Form GST RFD-11 on the GST portal. Once the ARN is generated, the LUT is valid. No physical submission, no bank guarantee for most businesses, no fee.

Before an LUT becomes relevant, the business must be GST-registered — our post on the GST registration threshold explains when registration is mandatory and how aggregate turnover is calculated.

Who needs an LUT — and who does not

The requirement is determined by whether you are making zero-rated supplies and want to do so without upfront IGST payment.

LUT is needed if you are: exporting goods or services directly (software, IT services, consulting, digital products), supplying goods or services to an SEZ unit or SEZ developer in India, or a startup billing foreign clients in convertible foreign exchange.

LUT is not needed if you are: making only domestic taxable supplies, exporting but choosing to pay IGST and claim a refund later, or below the GST registration threshold entirely.

One ineligibility: A registered person prosecuted for tax evasion exceeding ₹2.5 crore must furnish an export bond with a bank guarantee instead of an LUT. For most startups with a clean compliance record, the bond route is irrelevant — LUT is available.

One operational point: if your startup has multiple GST registrations across states, a separate LUT must be filed for each GSTIN. The LUT is GSTIN-specific.

LUT vs the alternative: why cash flow is at stake

Without a valid LUT, an exporter seeking zero-rated treatment must pay IGST on every export invoice and then file a refund claim in Form GST RFD-01. That refund involves waiting for GSTR-1 and GSTR-3B to be processed, a tax officer to approve the claim, and potentially responding to queries. Routine refund processing takes 30 to 60 days; complex cases take longer.

On ₹1 crore of monthly exports at 18% GST, that is ₹18 lakh of IGST paid and awaiting refund every month. The LUT route eliminates this entirely — zero IGST flows out on export invoices.

The exporter still accumulates ITC on input purchases (cloud services, office rent, software tools) and can claim that as a separate refund via Form RFD-01. But the export invoices themselves carry no IGST.

Once you are exporting under LUT, the ITC accumulated on inputs used for those exports can be claimed as a refund — our post on input tax credit basics explains how ITC accumulates and how the refund mechanism works.

What Meera’s case shows you

Meera runs a Bengaluru-based SaaS startup billing UK and UAE companies ₹40 lakh per month. The applicable GST rate on her software subscription service is 18%.

Without LUT: each month she pays ₹7.2 lakh in IGST and files for a refund. Over a quarter, ₹21.6 lakh is locked with the government at any given time — capital she needs to hire and grow.

With LUT: she files Form RFD-11 before her first export invoice of the financial year, receives an ARN, and raises all export invoices with zero IGST. She reports each invoice in Table 6B of GSTR-1 as zero-rated supply under LUT and files GSTR-3B normally.

Her ongoing obligation: ensure the foreign exchange for each invoice is received within one year. Most SaaS businesses with monthly payment terms are comfortably within this window.

The two compliance obligations that come with an LUT

Filing the LUT is the start, not the end. Two ongoing conditions apply after filing.

Condition 1 — for goods exporters: Goods must be exported within three months of the invoice date. If shipment is delayed beyond that window, IGST plus 18% interest per annum is payable within 15 days of the deadline’s expiry, calculated from the invoice date.

Condition 2 — for service exporters: Payment must be received in convertible foreign exchange within one year of the invoice date. The same 15-day window and 18% interest consequence apply if payment is not received.

Both conditions are tracked against the invoice date. A missed deadline withdraws the LUT privilege for that supply — restored once the tax and interest are paid.

For GSTR-1 purposes, export invoices under LUT go in Table 6B (zero-rated supply without payment of tax). Table 6A is for exports with IGST payment. Reporting in the wrong table creates mismatches and system queries.

Filing an LUT does not replace your monthly or quarterly return obligations — our post on GST returns covers GSTR-1 and GSTR-3B deadlines and what happens when they are missed.

Key parameters of LUT under GST at a glance

Here is a quick-reference infographic covering the critical compliance facts for any startup or exporter considering the LUT route.

When the LUT route breaks down

Goods not shipped within three months. Rule 96A of the CGST Rules 2017 requires goods to be exported within three months of the invoice date. If delayed, IGST plus 18% interest must be paid within 15 days of the cutoff. Once paid, the LUT privilege is restored.

Foreign exchange not received within one year (services). Most monthly-subscription businesses are well within this window. But renegotiated contracts or payment disputes can push past it. If payment is not received, IGST and interest become payable on that invoice.

LUT not renewed at year-end. The LUT expires 31 March. A zero-rated invoice raised on 2 April without a renewed LUT is taxable — IGST is due. This is the single most common LUT failure. Set a calendar reminder for late March every year.

Multiple GSTINs, only one LUT filed. Each GSTIN needs its own LUT. A valid Karnataka LUT does not cover exports from a Tamil Nadu GSTIN.

Common mistakes startups make

Not filing LUT before the first invoice. The LUT must be in place before the export invoice is raised. A startup that raises an invoice first and files LUT the next day has a compliance gap — the first invoice technically lacked cover.

Reporting in the wrong GSTR-1 table. Table 6B is for zero-rated supply without IGST payment (LUT route). Table 6A is for exports with IGST payment. Reporting LUT-route invoices in 6A creates an automatic system mismatch.

Forgetting the annual renewal. A startup with a valid LUT all year forgets renewal. The first April invoice goes out zero-rated — now IGST is owed on that supply.

Assuming SEZ supplies don’t need LUT. Domestic SEZ supplies are also zero-rated and need LUT coverage, exactly like foreign exports.

Not tracking forex realisation for services. Each invoice has its own one-year payment window. Losing track of an unpaid invoice is avoidable with a simple accounts-receivable dashboard — but it is regularly missed.

Documents and details to keep ready

- GST login credentials (username and password) and valid DSC or EVC for portal submission

- GSTIN for which LUT is being filed (file separately for each GSTIN if multiple)

- Details of any prior prosecution history (relevant only if it exceeds ₹2.5 crore, which disqualifies you for LUT)

- Bank account details of the business (needed for certain portal verifications)

- ARN of the previous year’s LUT (for reference during renewal — the portal pre-fills some details)

- Export invoices and shipping bills (for goods) or foreign exchange inward remittance certificates (for services) — needed to demonstrate timely compliance if queried

Final takeaway

An LUT under GST is one of the most impactful compliance steps an export-oriented startup can take — and one of the simplest. A single filing of Form RFD-11 before the first export invoice of each financial year unlocks zero-IGST export invoicing for the whole year. The alternative, paying 18% IGST and chasing refunds, locks working capital that early-stage companies cannot afford to idle. File LUT before the first invoice, report exports in Table 6B of GSTR-1, and track your shipment and forex realisation timelines per invoice.

Starting to export services or goods and unsure whether LUT applies to your structure, or want to ensure your GSTR-1 reports zero-rated supplies correctly? eTaxMate can review your export setup, file your LUT, and handle your GST return compliance.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. What is an LUT under GST and who needs to file it?

An LUT (Letter of Undertaking) under GST is a declaration filed in Form GST RFD-11 by a GST-registered exporter or SEZ supplier. It allows them to supply goods or services without paying IGST at the time of invoicing. Any registered person making zero-rated supplies — exports to foreign buyers or supplies to SEZ units or developers — should file an LUT to avoid blocking working capital in upfront IGST payments and refund cycles.

2. How long is an LUT valid under GST?

An LUT is valid for one financial year, from 1 April to 31 March. It must be renewed every year before the first export or SEZ supply of the new financial year — ideally before 31 March to avoid a gap on Day 1. If you start exporting mid-year, file the LUT before your first export invoice and it will remain valid until 31 March of that financial year.

3. What happens if I export without a valid LUT?

If you raise an export invoice without a valid LUT, the supply is treated as a taxable domestic supply by default. IGST at the applicable rate becomes payable, along with interest under Section 50 of the CGST Act. If goods are not exported within 3 months of the invoice date under LUT, or foreign exchange for services is not received within 1 year, IGST plus 18% interest must be paid within 15 days of the deadline.

4. Do startups exporting software services need an LUT?

Yes. Software services and other IT-enabled services billed to foreign clients qualify as exports of services under Section 2(6) of the IGST Act 2017, provided payment is received in convertible foreign exchange. These are zero-rated supplies. To avoid paying 18% IGST on each invoice and waiting for a refund, the startup should file Form RFD-11 before raising their first export invoice. The LUT covers all foreign service invoices for that financial year.

5. Can I claim ITC refund if I export under LUT?

Yes. Under the LUT route, no IGST is paid on the export invoice — but the exporter continues to accumulate Input Tax Credit on input purchases (cloud services, software tools, office costs, etc.). This accumulated ITC on inputs used for zero-rated supplies can be claimed as a cash refund by filing Form RFD-01 on the GST portal. This is separate from — and in addition to — the IGST savings from the LUT route itself.

6. Does an LUT cover supplies to SEZ units inside India?

Yes. Supplies to Special Economic Zone (SEZ) units and SEZ developers within India are classified as zero-rated supplies under Section 16 of the IGST Act 2017, just like foreign exports. A valid LUT covers both foreign exports and SEZ supplies under the same filing. If the business has multiple GSTINs registered in different states, a separate LUT must be filed for each GSTIN.