If you have never looked past the “net pay” figure on your payslip, you are leaving tax decisions to your payroll team by default. Two people earning the same cost-to-company can pay very different amounts of tax, purely because of how their salary is split. This is the heart of salary breakup and tax planning: the same rupees, arranged differently, are taxed differently. The catch is that the rules changed sharply once the new tax regime became the default, and a structure that saved tax three years ago may do nothing today. This post walks you through what actually matters now.

Quick answer

Your salary breakup affects your tax bill, but how much it helps depends entirely on which regime you are in. Under the new tax regime (the default for AY 2026-27), most allowance-based exemptions are gone, so structure matters far less. Under the old regime, the split between basic pay, HRA, and allowances still drives real savings.

Before changing anything, check:

- Which regime you are actually taxed under this year.

- Whether you live in rented accommodation (this decides if HRA is worth anything).

- Whether your employer offers an NPS contribution, since this survives in both regimes.

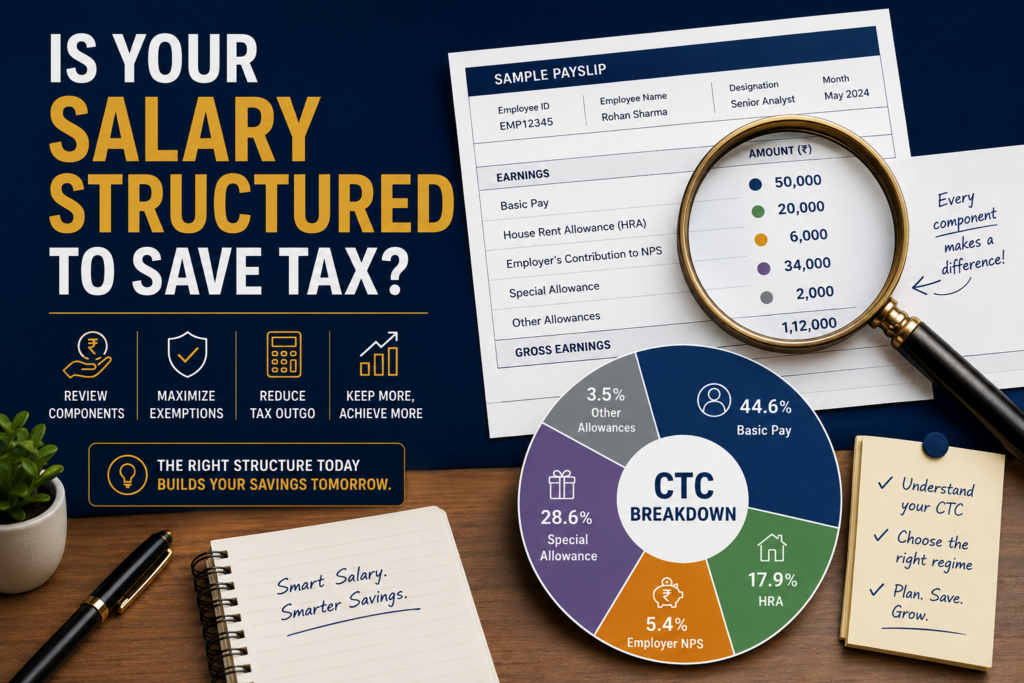

What your salary breakup actually contains

Your cost-to-company is rarely a single number paid out. It is split into building blocks, and each block is taxed under its own rule.

The common components are basic salary, dearness allowance (DA) where applicable, House Rent Allowance (HRA — an allowance meant to offset rent you pay), Leave Travel Allowance (LTA — reimbursement for travel during leave), special allowance (a residual taxable bucket), employer contributions to Provident Fund and the National Pension System (NPS — a government-backed retirement scheme), and retirement benefits like gratuity.

Basic salary is fully taxable, but it is also the anchor. Several exemptions — HRA, employer PF, and employer NPS — are calculated as a percentage of basic pay. So a salary that is heavily loaded into “special allowance” instead of basic can quietly shrink the exemptions you are entitled to under the old regime.

How the regime you choose changes everything

This is where most outdated advice goes wrong. The value of your salary structure depends almost entirely on your regime, so address that first.

Under the new tax regime, which is the default under Section 115BAC of the Income Tax Act 1961, most salary-linked exemptions have been removed. HRA exemption, LTA, and the deductions under Section 80C are not available. What you do keep is the standard deduction of ₹75,000 and, importantly, the deduction for your employer’s NPS contribution under Section 80CCD(2). For a deeper comparison of where each regime wins, see our explainer on the [old versus new tax regime].

Under the old tax regime, the full toolkit survives: HRA exemption, LTA, Section 80C investments up to ₹1.5 lakh, and more. Here, how your salary is split genuinely changes your tax.

One nuance worth getting right: the employer NPS deduction under Section 80CCD(2) is capped at 14% of basic plus DA in the new regime for all employees, but at 10% of basic plus DA for private-sector employees in the old regime. The Income Tax Act 2025 takes effect from 1 April 2026, so for AY 2026-27 the provisions of the 1961 Act still apply to income earned up to 31 March 2026.

The components worth reviewing

Take Priya, a Bengaluru-based marketing manager renting a flat, on the old regime. Her CTC is ₹18 lakh. If her employer loads ₹9 lakh into basic salary and gives her HRA of ₹4.5 lakh, her HRA exemption (the least of actual HRA, rent paid minus 10% of basic, or 50% of basic in a metro) can be substantial. If instead the same CTC is structured with only ₹4 lakh basic and a large “special allowance,” her HRA exemption shrinks, because it is pegged to basic pay. Same CTC, different tax. Reviewing whether her [HRA exemption] is being maximised is the single most valuable check for a renter on the old regime.

Now take Rahul, a software engineer on the new regime who does not rent and has no major investments. For him, HRA and Section 80C are irrelevant. The one lever that still works is asking his employer to route a portion of CTC as an NPS contribution under Section 80CCD(2) — up to 14% of basic plus DA, fully deducted from taxable salary. This is the rare structuring move that helps in the new regime.

Gratuity and leave encashment exemptions, within prescribed limits, continue under both regimes. So does the employer PF contribution, within limits. These are not things you “claim” so much as confirm your payroll is treating correctly.

How to review your salary breakup

A salary review is not about asking for a bigger number. It is about arranging the existing number well. Here is the practical sequence.

- Pull your latest payslip and Form 16. Identify every component and how much each one is.

- Confirm your regime. If you are on the old regime, structure matters; if you are on the new regime, focus narrowly on employer NPS.

- Run both regimes side by side using the tax calculator on the [Income Tax e-filing portal] before deciding which one to declare to your employer.

- If on the old regime, check your basic-pay ratio. A basic that is too low caps your HRA and PF benefits.

- Ask about an employer NPS option if one exists — it is one of the few moves that helps under the new regime.

- Submit your declarations on time so your employer deducts the right TDS through the year, rather than you scrambling for a refund later. If your taxable income lands near the threshold, confirm whether the [Section 87A rebate] applies before assuming you owe nothing.

The infographic below summarises which components survive under each regime.

When salary restructuring is not worth it

Restructuring is not free, and chasing it blindly can backfire. Step back in these situations.

If you are on the new regime and do not have an employer NPS option, there is very little structuring left to do — the slab rates and standard deduction already do the work, and time spent rearranging allowances is wasted.

If you do not pay rent, do not chase a high HRA component. HRA only gives an exemption when you actually pay rent and can prove it; an inflated HRA with no genuine rent invites scrutiny and is not a saving.

Do not cut your basic pay too low purely to dodge tax. Basic salary drives your PF, gratuity, and HRA limits, so a thin basic can reduce your retirement corpus and long-term benefits for a small annual tax gain. Finally, never claim rent paid to a family member without an actual rental arrangement, genuine payments, and the recipient declaring that rent as income — fabricated arrangements are a common trigger for notices.

Documents and declarations to keep ready

📋 Keep these handy before you review or restructure:

- Latest monthly payslip and your annual CTC letter

- Form 16 from your employer for the relevant year

- Rent receipts and your rental agreement, if claiming HRA

- Landlord’s PAN, if annual rent exceeds ₹1 lakh

- Proof of Section 80C and 80D investments, if on the old regime

- Your employer’s investment declaration form and its deadline

- NPS account details, if your employer offers a contribution

Final takeaway

Salary breakup tax planning is no longer a one-size-fits-all exercise. The honest answer is that your regime decides how much your structure matters: under the new regime, the slabs and standard deduction do most of the work and only employer NPS moves the needle; under the old regime, a well-set basic pay and HRA can save real money if you rent. Decide your regime first by running both calculations, then shape your salary to fit that choice — not the other way around.

Confused about how your salary breakup is taxed, or unsure which regime leaves you better off? eTaxMate can help you review your CTC structure, identify what applies to you, and handle your filing or declarations correctly.

This blog post is for general information only and does not constitute professional advice. Tax laws are subject to change and their application depends on individual facts and circumstances. Readers should consult a qualified professional before taking any action based on this content. eTaxMate accepts no liability for any action taken based on the information in this post.

Frequently Asked Questions

1. Does my salary structure still help me save tax under the new regime?

Much less than before. Under the new tax regime, exemptions like HRA, LTA, and Section 80C are no longer available, so rearranging allowances does little. The one structuring move that still works is asking your employer to contribute to your NPS account under Section 80CCD(2), which is deductible up to 14% of basic plus DA.

2. Why does my basic salary amount matter so much?

Basic salary is the anchor for several benefits. Your HRA exemption, provident fund, and gratuity are all calculated as a percentage of basic pay. If your salary is loaded into “special allowance” instead of basic, these benefits shrink. Under the old regime especially, a healthy basic-pay ratio protects your exemptions and your long-term retirement corpus.

3. Can I claim HRA if I do not pay rent?

No. HRA exemption is only available when you actually pay rent for accommodation you live in and can prove it with receipts and an agreement. Receiving an HRA component on your payslip does not by itself give an exemption. Claiming HRA without genuine rent, or against fabricated arrangements, is a common trigger for tax notices.

4. Is the employer’s NPS contribution taxable?

The employer’s contribution to your NPS account is deductible from taxable salary under Section 80CCD(2), within limits — up to 14% of basic plus DA in the new regime, and 10% for private-sector employees in the old regime. Your own contribution to NPS, however, is not deductible under the new regime.

5. Should I switch to the new regime just to avoid salary planning?

Not automatically. The right regime depends on your numbers. If you rent and have strong Section 80C investments, the old regime may still leave you better off despite the extra paperwork. The reliable method is to compute your tax under both regimes side by side using the same income figures, then choose.

6. Which salary components stay tax-free under both regimes?

A few survive in both. Gratuity and leave encashment remain exempt within prescribed limits, the employer’s PF contribution stays tax-free within limits, and the employer’s NPS contribution under Section 80CCD(2) is deductible under both regimes. The standard deduction also applies in both, though it is higher in the new regime at ₹75,000 versus ₹50,000.